Question

(b) Suppose the bond above is putable at par from Year 1. Compute the value of the bond at time 0. (c) Suppose the interest

(b) Suppose the bond above is putable at par from Year 1. Compute the value of the bond at time 0.

(c) Suppose the interest rate volatility increases. Appraise how it affects the value of the putable bond in Part (b).

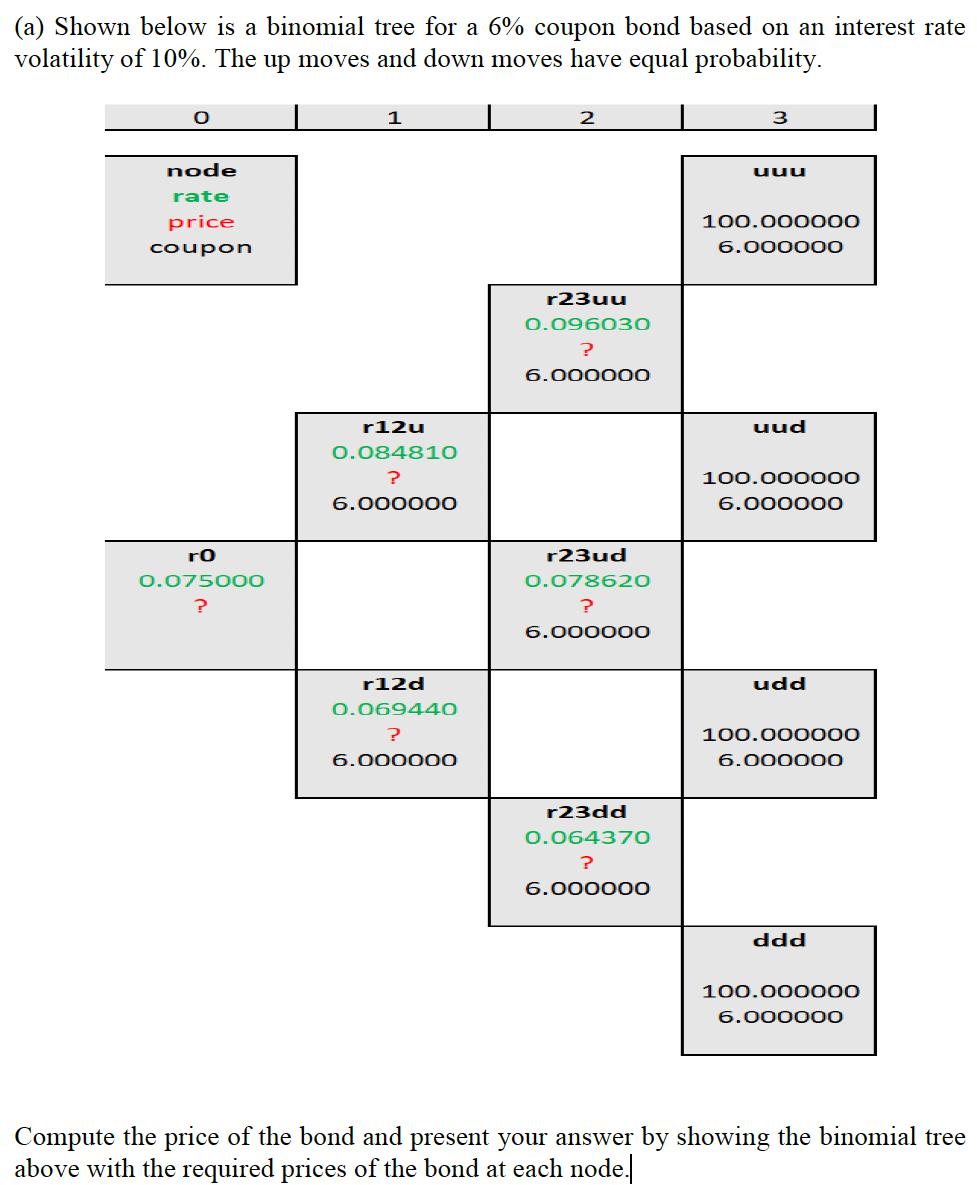

(a) Shown below is a binomial tree for a 6% coupon bond based on an interest rate volatility of 10%. The up moves and down moves have equal probability. O node rate price coupon ro 0.075000 ? 1 r12u 0.084810 ? 6.000000 r12d 0.069440 ? 6.000000 2 r23uu 0.096030 ? 6.000000 r23ud 0.078620 ? 6.000000 r23dd 0.064370 ? 6.000000 3 uuu 100.000000 6.000000 uud 100.000000 6.000000 udd 100.000000 6.000000 ddd 100.000000 6.000000 Compute the price of the bond and present your answer by showing the binomial tree above with the required prices of the bond at each node.

Step by Step Solution

3.36 Rating (171 Votes )

There are 3 Steps involved in it

Step: 1

Solution a Shown below is the binomial tree with the bond prices at each node 0 1 2 3 ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Payroll Accounting 2017

Authors: Bernard J. Bieg, Judith Toland

27th edition

1305675126, 1305675124, 9781305888586, 1305888588, 978-1337734776