Question

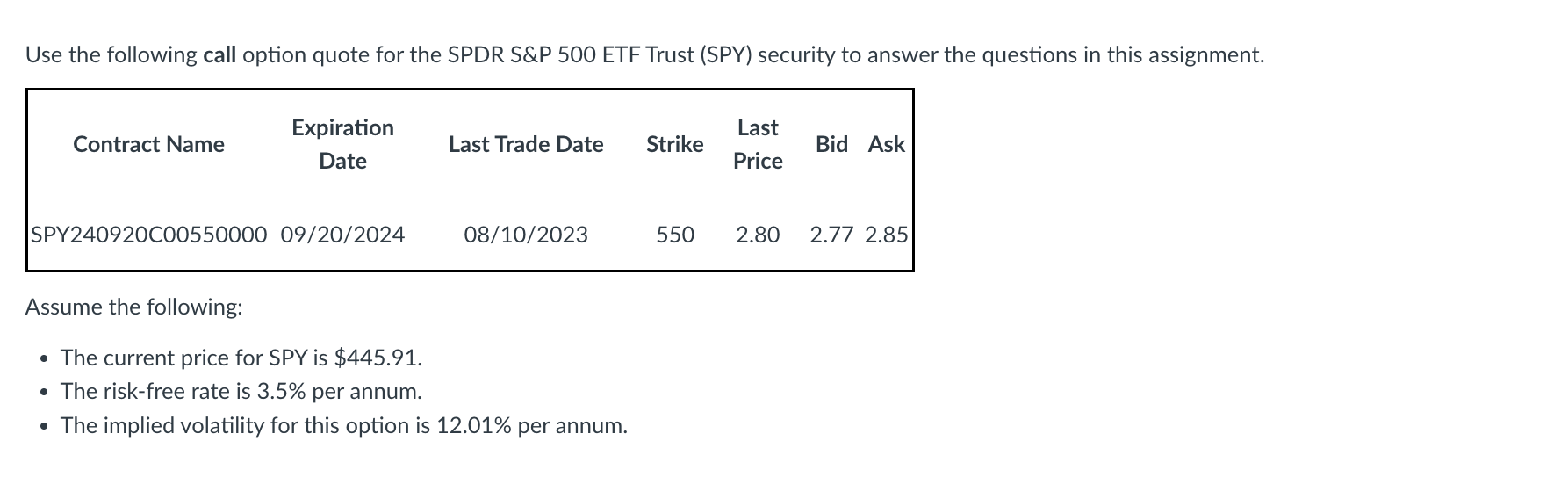

What would be your percent return had you purchased a single contract at the call premium when the SPY price was $445.91 and sold at

- What would be your percent return had you purchased a single contract at the call premium when the SPY price was $445.91 and sold at the expected call premium if the underlying SPY price increased to $500 (do not round the forecasted premium)?

[Enter the final answer in as a percent (e.g., 5.55%=5.55) - not a decimal and put a negative sign if appropriate]

2. What would be the expected premium of the call option if the underlying stock price for SPY decreased to $400 per share (Hint: adjust the input S in your B-S model)?

3. What would be your dollar return had you purchased a single contract at the call premium when the SPY price was $445.91 and sold at the expected call premium if the underlying SPY price decreased to $400 (do not round the forecasted premium)?

[Round the answer to the nearest cent and put a negative sign if appropriate]

4. What would be your percent return had you purchased a single contract at the call premium when the SPY price was $445.91 and sold at the expected call premium if the underlying SPY price decreased to $400 (do not round the forecasted premium)?

[Enter the final answer in as a percent (e.g., 5.55%=5.55) - not a decimal and put a negative sign if appropriate]

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Real Estate Finance and Investments

Authors: William Brueggeman, Jeffrey Fisher

14th edition

73377333, 73377339, 978-0073377339