Answered step by step

Verified Expert Solution

Question

1 Approved Answer

whats the difference between yield and curve sensitivity. please explain in details Q. For a long-term, zero-coupon bond, which of the following factors contributes to

whats the difference between yield and curve sensitivity.

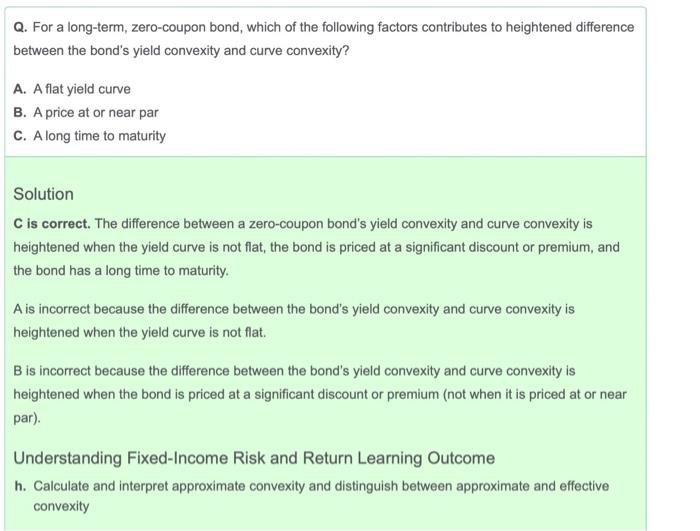

Q. For a long-term, zero-coupon bond, which of the following factors contributes to heightened difference between the bond's yield convexity and curve convexity? A. A flat yield curve B. A price at or near par C. A long time to maturity Solution C is correct. The difference between a zero-coupon bond's yield convexity and curve convexity is heightened when the yield curve is not flat, the bond is priced at a significant discount or premium, and the bond has a long time to maturity. A is incorrect because the difference between the bond's yield convexity and curve convexity is heightened when the yield curve is not flat. B is incorrect because the difference between the bond's yield convexity and curve convexity is heightened when the bond is priced at a significant discount or premium (not when it is priced at or near par). Understanding Fixed-Income Risk and Return Learning Outcome h. Calculate and interpret approximate convexity and distinguish between approximate and effective convexity please explain in details

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Old Money New Woman How To Manage Your Money And Your Life

Authors: Byron Tully

1st Edition

1950118010, 978-1950118014