Question

Where it says select, the options are increase or decrease. Consider the following questions on the pricing of options on the stock of ARB Inc.:

Where it says select, the options are increase or decrease.

Where it says select, the options are increase or decrease.

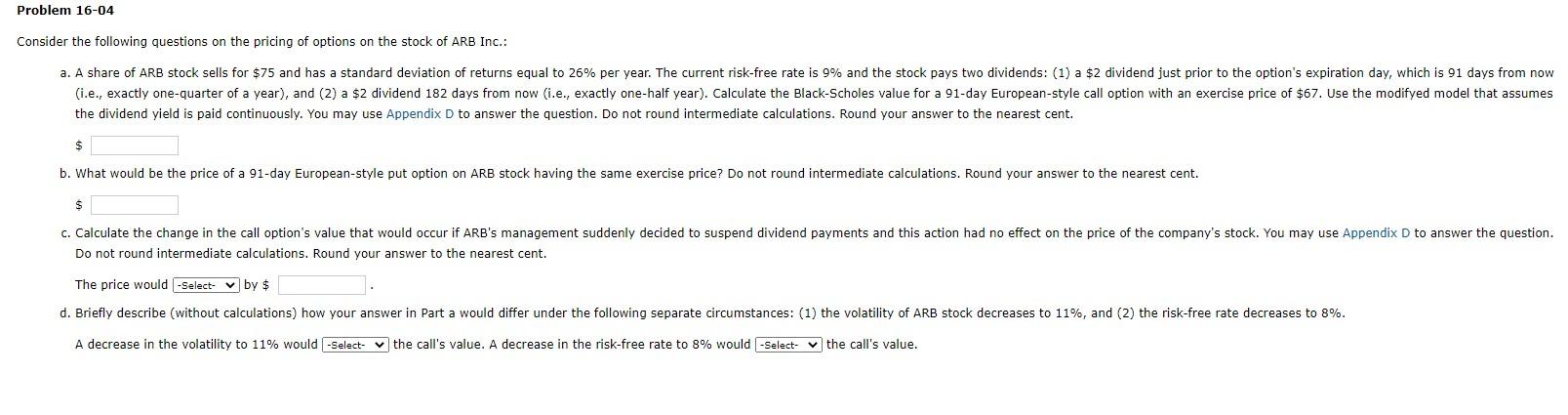

Consider the following questions on the pricing of options on the stock of ARB Inc.:

A share of ARB stock sells for $75 and has a standard deviation of returns equal to 26% per year. The current risk-free rate is 9% and the stock pays two dividends: (1) a $2 dividend just prior to the option's expiration day, which is 91 days from now (i.e., exactly one-quarter of a year), and (2) a $2 dividend 182 days from now (i.e., exactly one-half year). Calculate the Black-Scholes value for a 91-day European-style call option with an exercise price of $67. Use the modifyed model that assumes the dividend yield is paid continuously. You may use Appendix D to answer the question. Do not round intermediate calculations. Round your answer to the nearest cent.

$

What would be the price of a 91-day European-style put option on ARB stock having the same exercise price? Do not round intermediate calculations. Round your answer to the nearest cent.

$

Calculate the change in the call option's value that would occur if ARB's management suddenly decided to suspend dividend payments and this action had no effect on the price of the company's stock. You may use Appendix D to answer the question. Do not round intermediate calculations. Round your answer to the nearest cent.

The price would -Select-decreaseincreaseItem 3 by $ .

Briefly describe (without calculations) how your answer in Part a would differ under the following separate circumstances: (1) the volatility of ARB stock decreases to 11%, and (2) the risk-free rate decreases to 8%.

A decrease in the volatility to 11% would -Select-decreaseincreaseItem 5 the call's value. A decrease in the risk-free rate to 8% would -Select-decreaseincreaseItem 6 the call's value.

Problem 16-04 Consider the following questions on the pricing of options on the stock of ARB Inc.: a. A share of ARB stock sells for $75 and has a standard deviation of returns equal to 26% per year. The current risk-free rate is 9% and the stock pays two dividends: (1) a $2 dividend just prior to the option's expiration day, which is 91 days from now (i.e., exactly one-quarter of a year), and (2) a $2 dividend 182 days from now (i.e., exactly one-half year). Calculate the Black-Scholes value for a 91-day European-style call option with an exercise price of $67. Use the modifyed model that assumes the dividend yield is paid continuously. You may use Appendix D to answer the question. Do not round intermediate calculations. Round your answer to the nearest cent. $ b. What would be the price of a 91-day European-style put option on ARB stock having the same exercise price? Do not round intermediate calculations. Round your answer to the nearest cent. $ c. Calculate the change in the call option's value that would occur if ARB's management suddenly decided to suspend dividend payments and this action had no effect on the price of the company's stock. You may use Appendix D to answer the question. Do not round intermediate calculations. Round your answer to the nearest cent. The price would -Select- by $ d. Briefly describe (without calculations) how your answer in Part a would differ under the following separate circumstances: (1) the volatility of ARB stock decreases to 11%, and (2) the risk-free rate decreases to 8%. A decrease in the volatility to 11% would -Select-the call's value. A decrease in the risk-free rate to 8% would -Select-the call's value. Problem 16-04 Consider the following questions on the pricing of options on the stock of ARB Inc.: a. A share of ARB stock sells for $75 and has a standard deviation of returns equal to 26% per year. The current risk-free rate is 9% and the stock pays two dividends: (1) a $2 dividend just prior to the option's expiration day, which is 91 days from now (i.e., exactly one-quarter of a year), and (2) a $2 dividend 182 days from now (i.e., exactly one-half year). Calculate the Black-Scholes value for a 91-day European-style call option with an exercise price of $67. Use the modifyed model that assumes the dividend yield is paid continuously. You may use Appendix D to answer the question. Do not round intermediate calculations. Round your answer to the nearest cent. $ b. What would be the price of a 91-day European-style put option on ARB stock having the same exercise price? Do not round intermediate calculations. Round your answer to the nearest cent. $ c. Calculate the change in the call option's value that would occur if ARB's management suddenly decided to suspend dividend payments and this action had no effect on the price of the company's stock. You may use Appendix D to answer the question. Do not round intermediate calculations. Round your answer to the nearest cent. The price would -Select- by $ d. Briefly describe (without calculations) how your answer in Part a would differ under the following separate circumstances: (1) the volatility of ARB stock decreases to 11%, and (2) the risk-free rate decreases to 8%. A decrease in the volatility to 11% would -Select-the call's value. A decrease in the risk-free rate to 8% would -Select-the call's valueStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started