Question

Which cost flow assumption(s) does the company use to value its inventory? What is the amount of inventory purchases in fiscal year 2020? Estimate cash

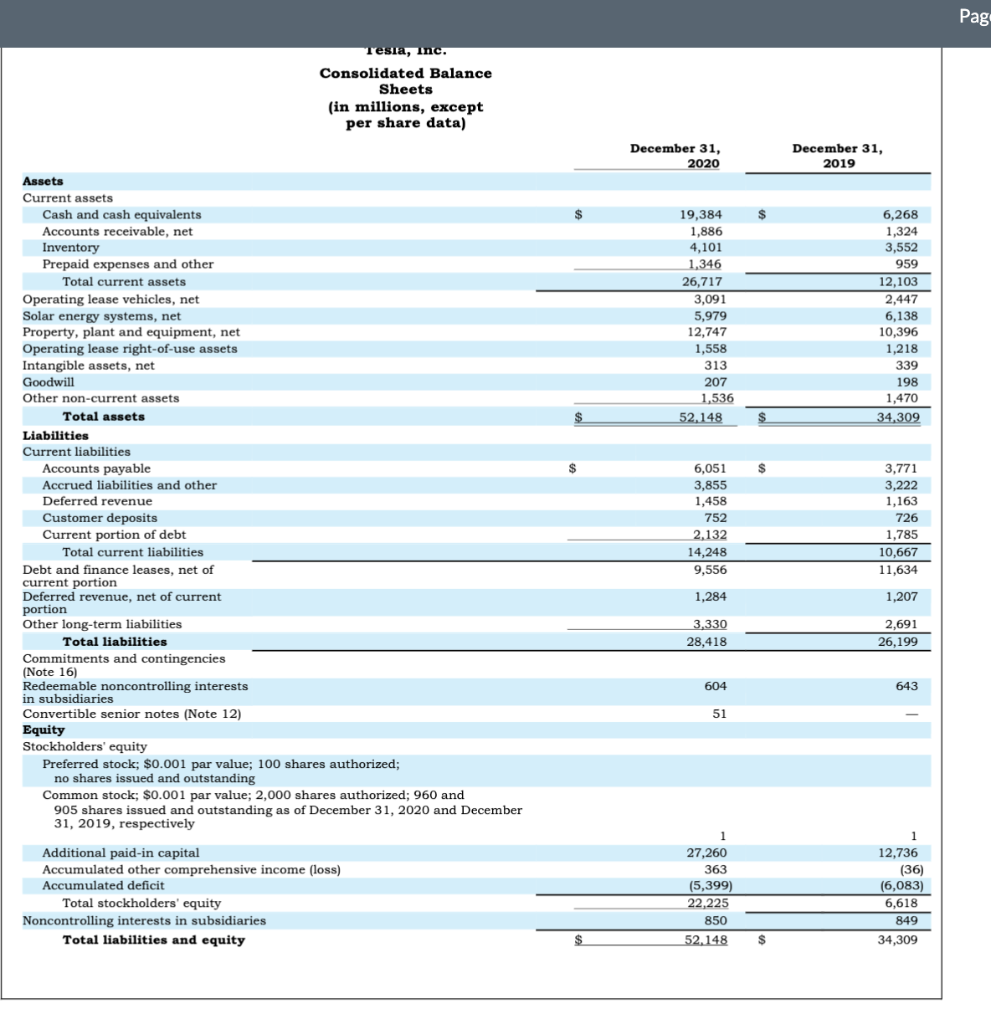

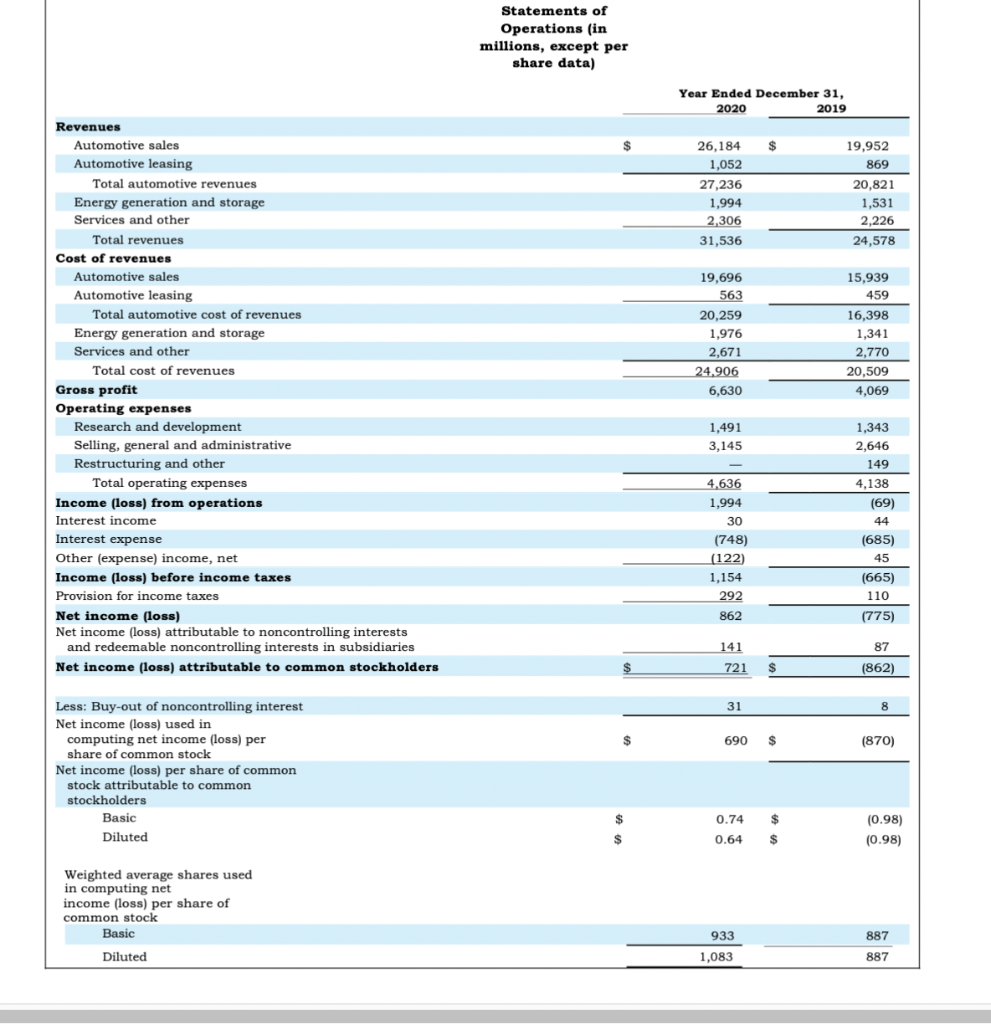

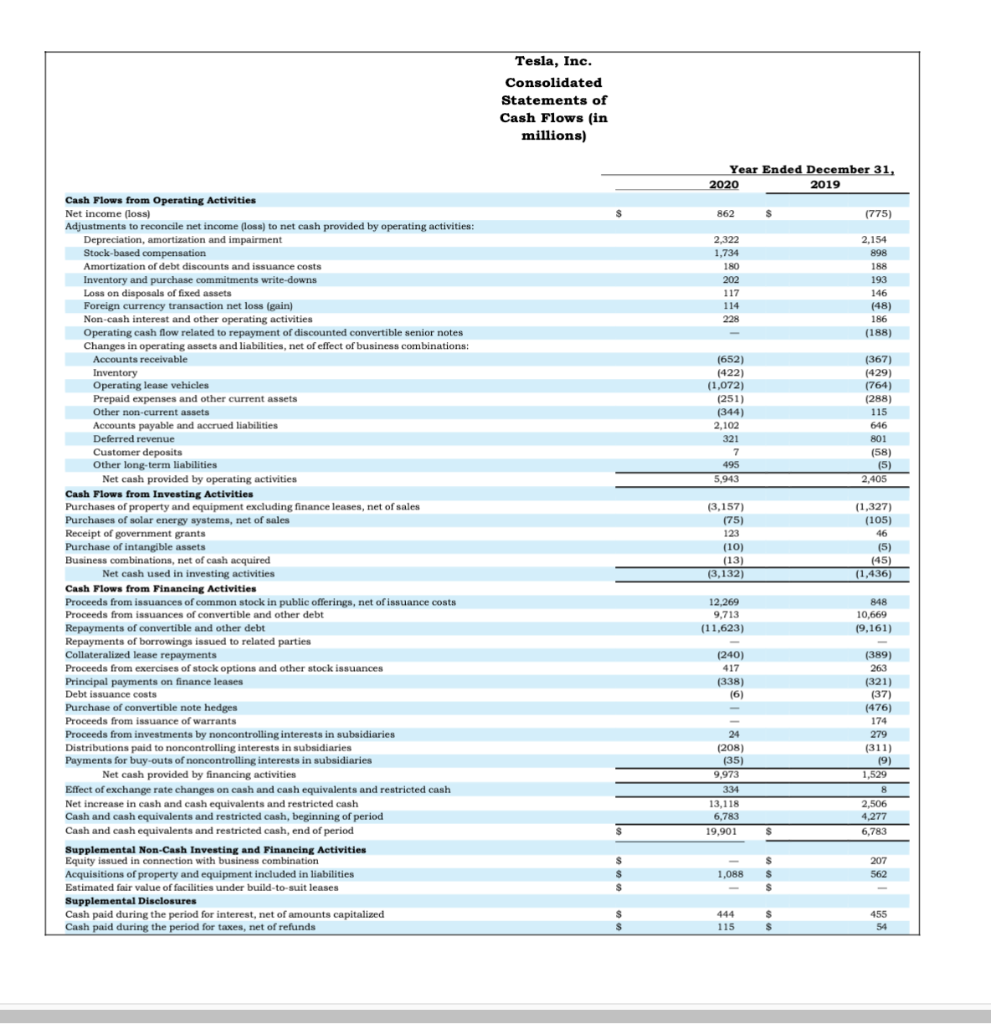

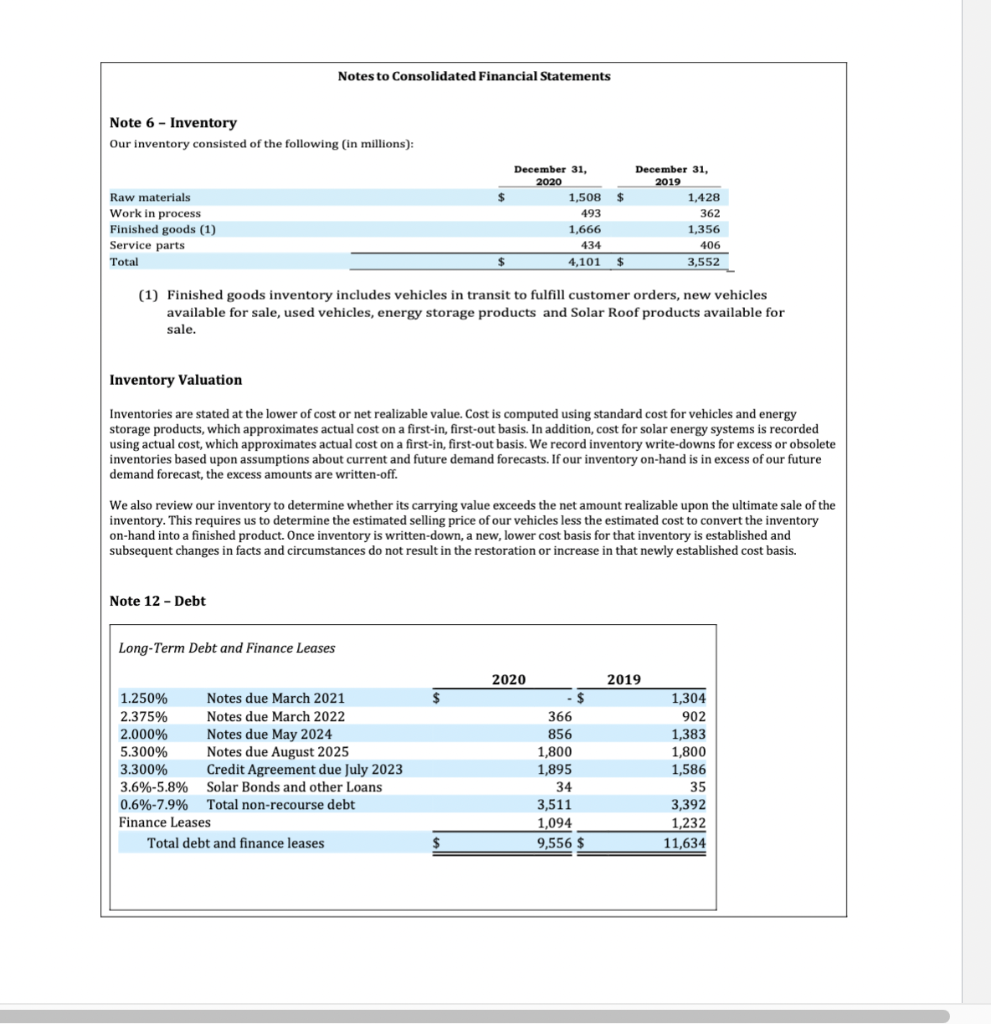

Which cost flow assumption(s) does the company use to value its inventory? What is the amount of inventory purchases in fiscal year 2020? Estimate cash collected from customers in fiscal year 2020 (Assume that sales are net of bad debt expense). Estimate cash paid to suppliers in fiscal year 2020 (Inventory purchases from question 2 above may be used in your calculation). How much cash was generated by the sale of common stock in public offerings during fiscal year 2020? What is the par value of each common share? What is the number of issued and outstanding common shares at the end of fiscal year 2020? Does the company own any treasury stock at the end of fiscal year 2020? Refer to the 5.30% Notes due August 2025 (fourth item listed in the Long-Term Debt table). Calculate the interest expense on this note for fiscal year 2023. Refer to the same notes as in the previous question (i.e., the 5.30% notes due 2025). Calculate the total cash that would be paid at maturity (Use semi-annual calculations). What is the present value of future minimum finance lease payments in 2020?

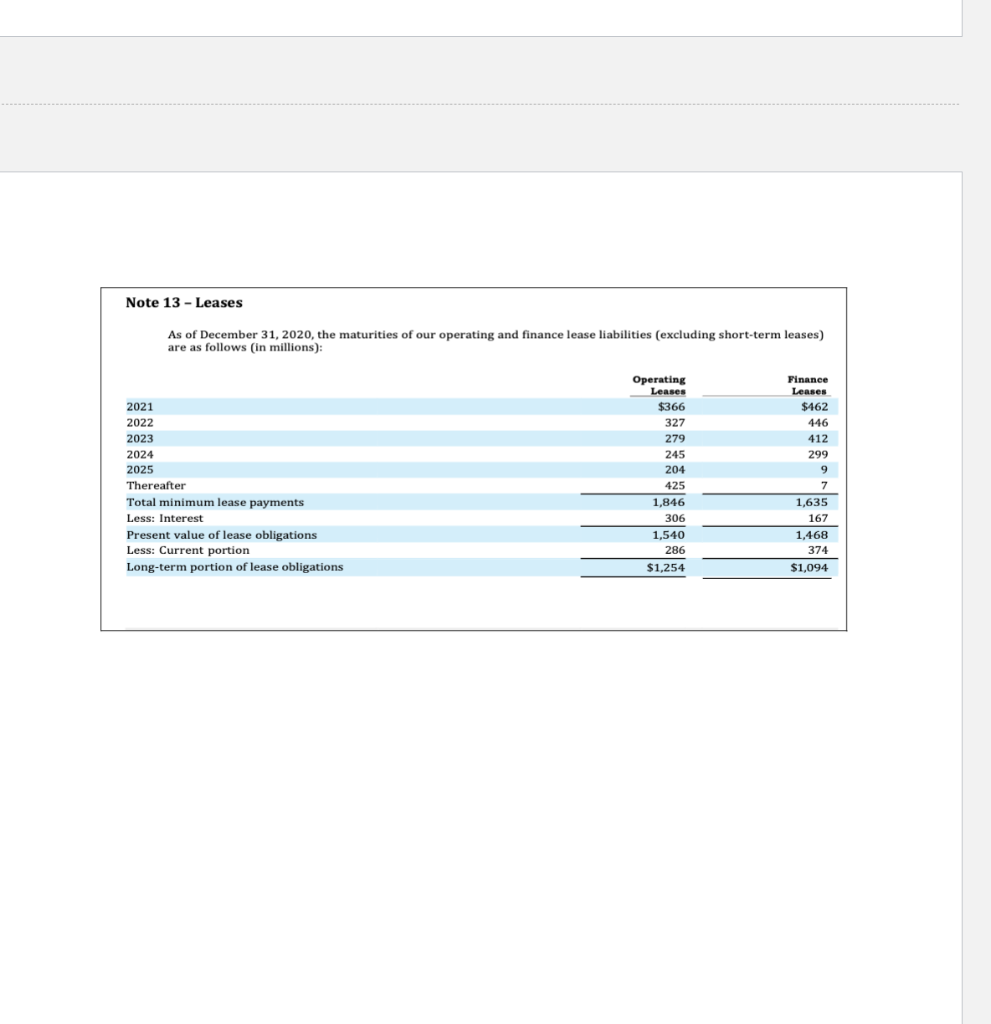

Consolidated Balance Sheets (in millions, except ner share datal Statements of Operations (in millions, except per share data) Notes to Consolidated Financial Statements Note 6 - Inventory Our inventory consisted of the following (in millions): (1) Finished goods inventory includes vehicles in transit to fulfill customer orders, new vehicles available for sale, used vehicles, energy storage products and Solar Roof products available for sale. Inventory Valuation Inventories are stated at the lower of cost or net realizable value. Cost is computed using standard cost for vehicles and energy storage products, which approximates actual cost on a first-in, first-out basis. In addition, cost for solar energy systems is recorded using actual cost, which approximates actual cost on a first-in, first-out basis. We record inventory write-downs for excess or obsolete inventories based upon assumptions about current and future demand forecasts. If our inventory on-hand is in excess of our future demand forecast, the excess amounts are written-off. We also review our inventory to determine whether its carrying value exceeds the net amount realizable upon the ultimate sale of the inventory. This requires us to determine the estimated selling price of our vehicles less the estimated cost to convert the inventory on-hand into a finished product. Once inventory is written-down, a new, lower cost basis for that inventory is established and subsequent changes in facts and circumstances do not result in the restoration or increase in that newly established cost basis. Note 12 - Debt As of December 31, 2020, the maturities of our operating and finance lease liabilities (excluding short-term leases) are as follows (in millions)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing

Authors: Alan Millichamp, John Taylor

11th Edition

1473749301, 978-1473749306