Which income statement presentation provides a better basis for managerial performance assessment: Lean or Traditional? Justify in terms of profitability and operational efficiency (Waste reduction).

Which income statement presentation provides a better basis for managerial performance assessment: Lean or Traditional? Justify in terms of profitability and operational efficiency (Waste reduction).

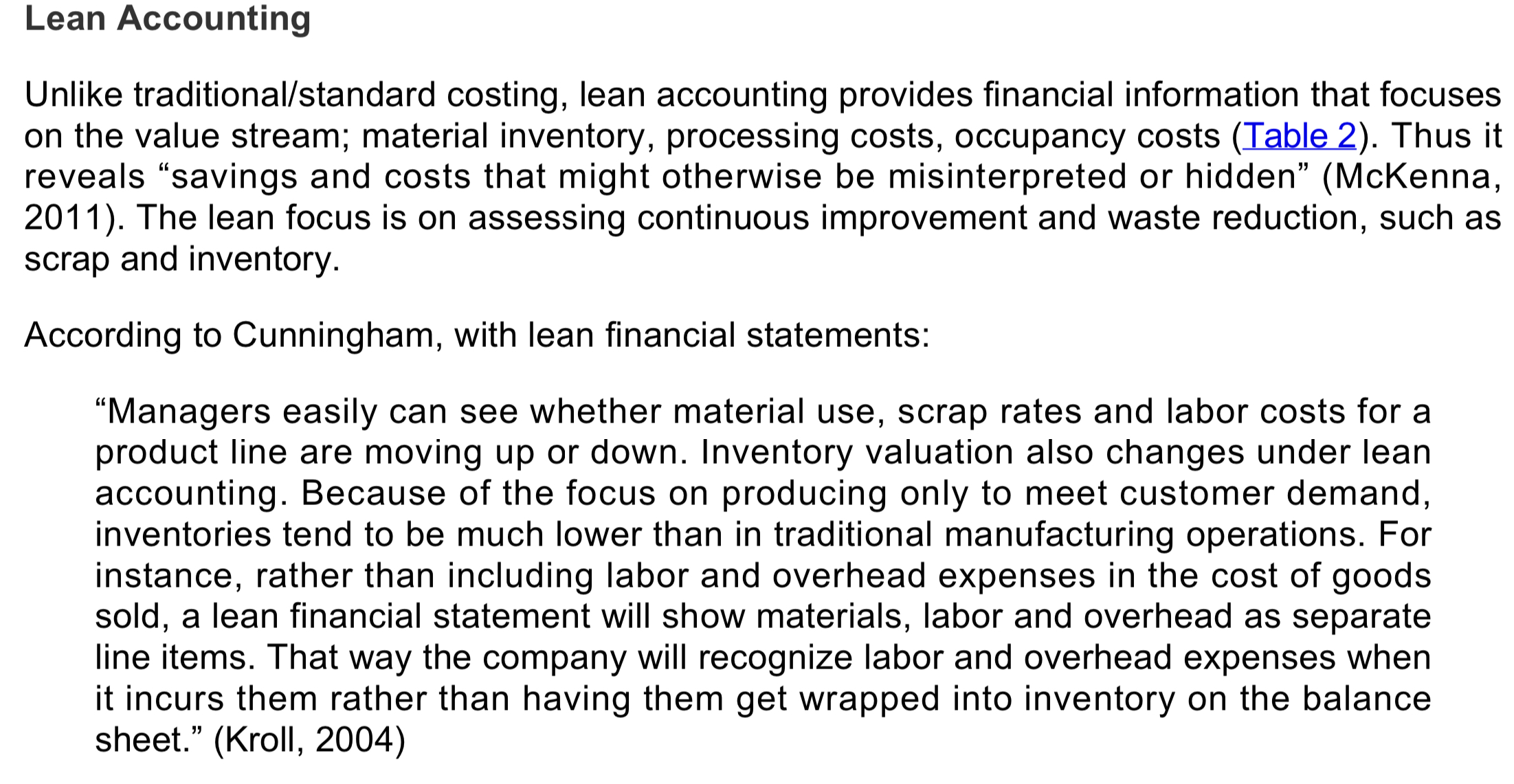

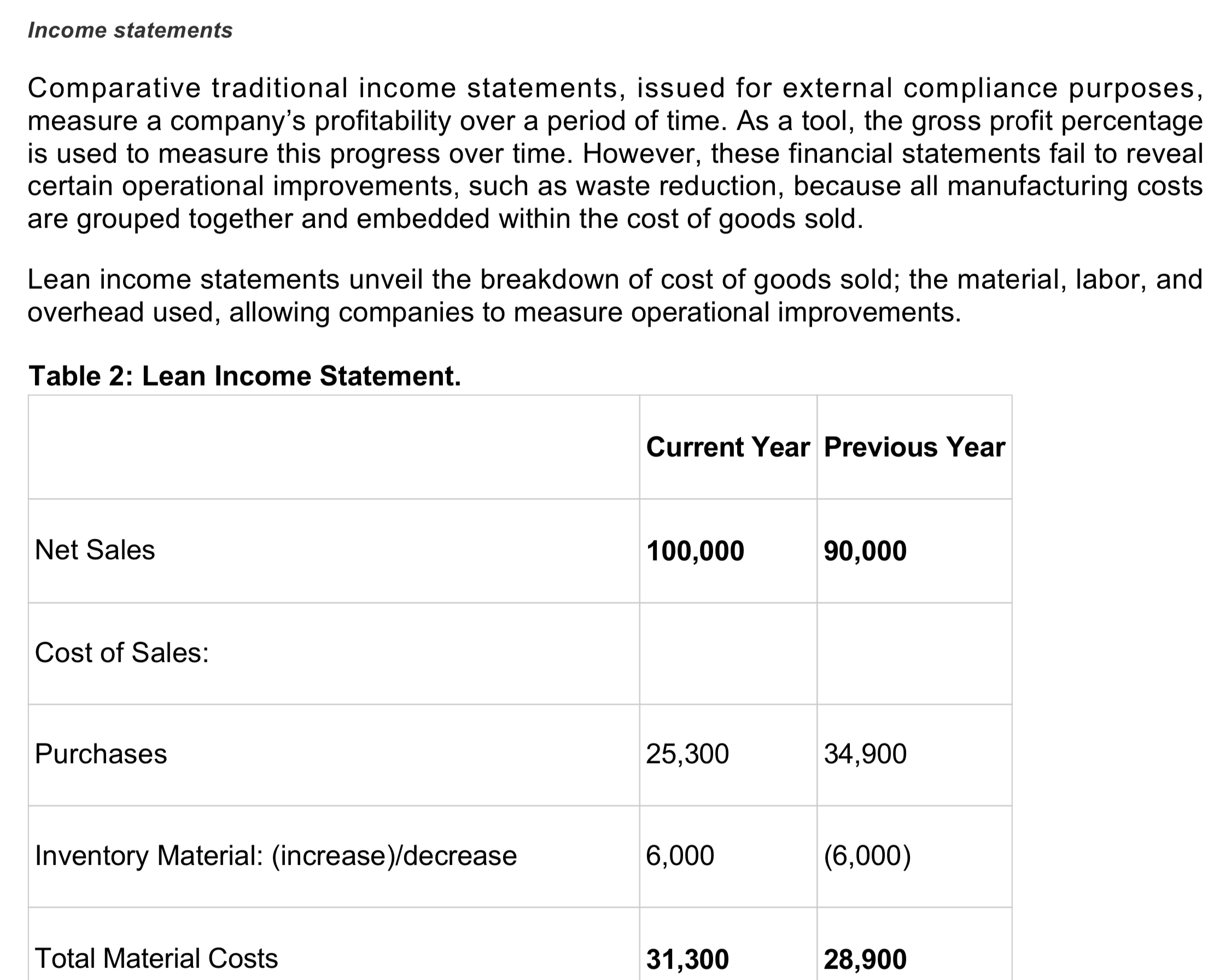

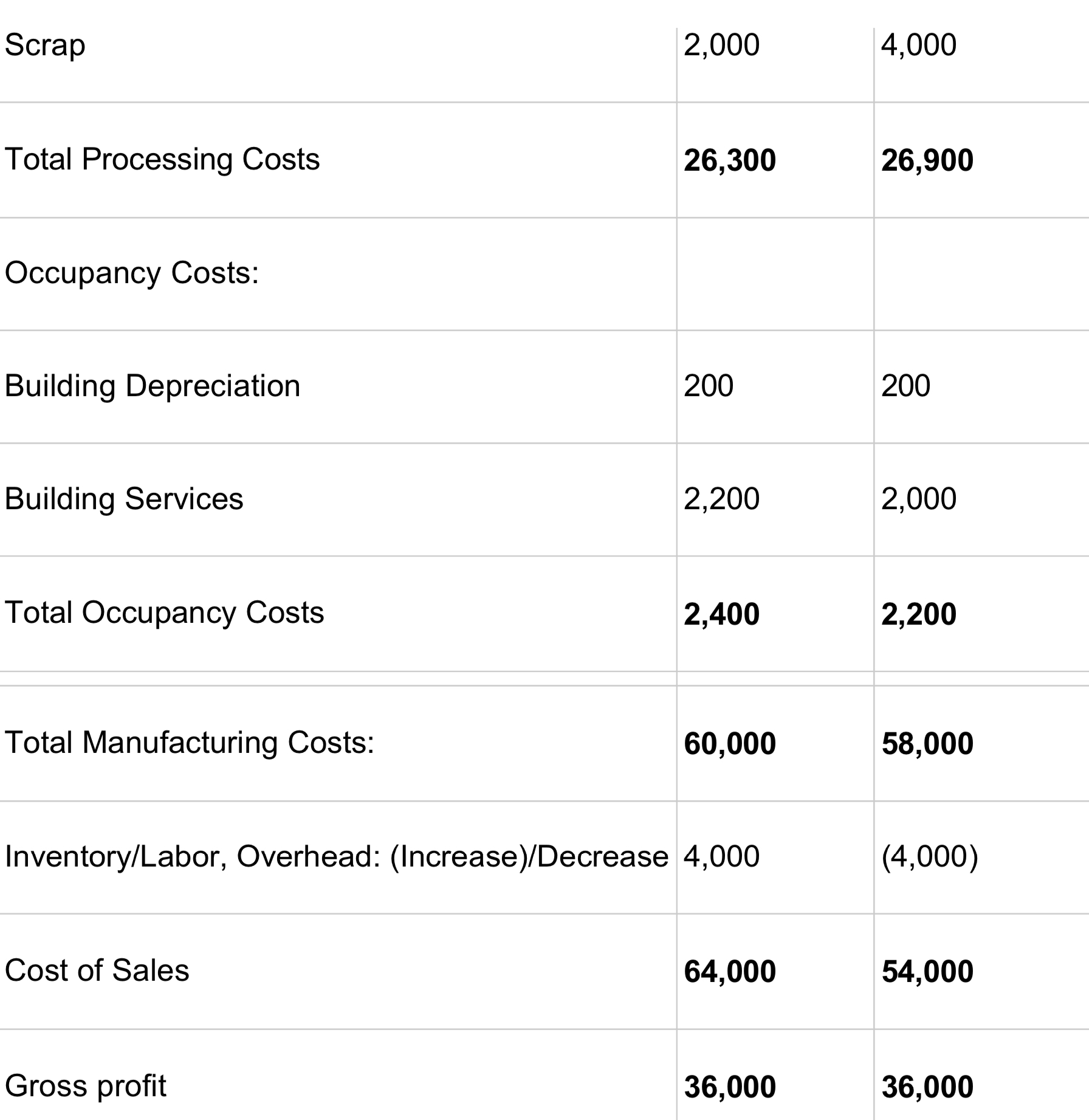

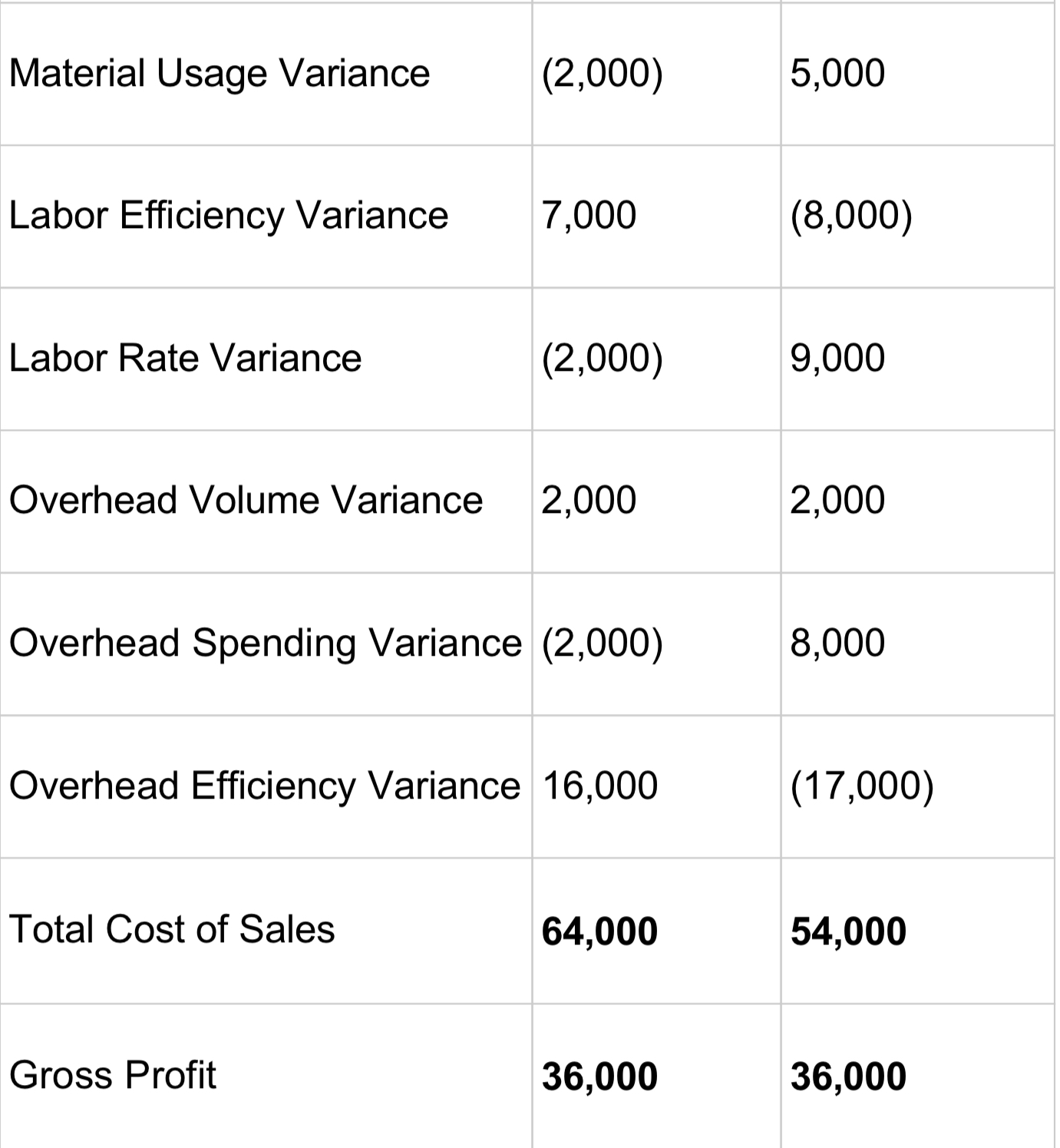

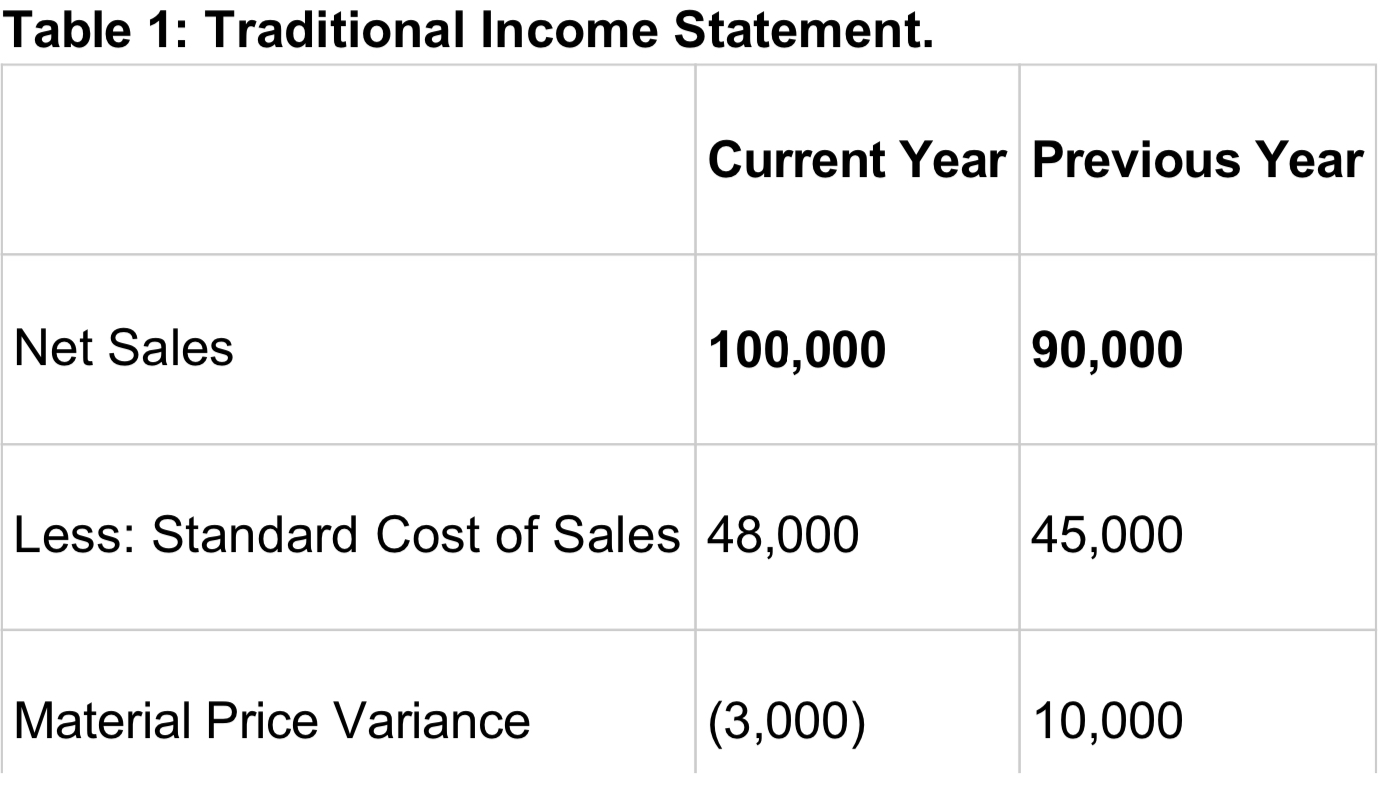

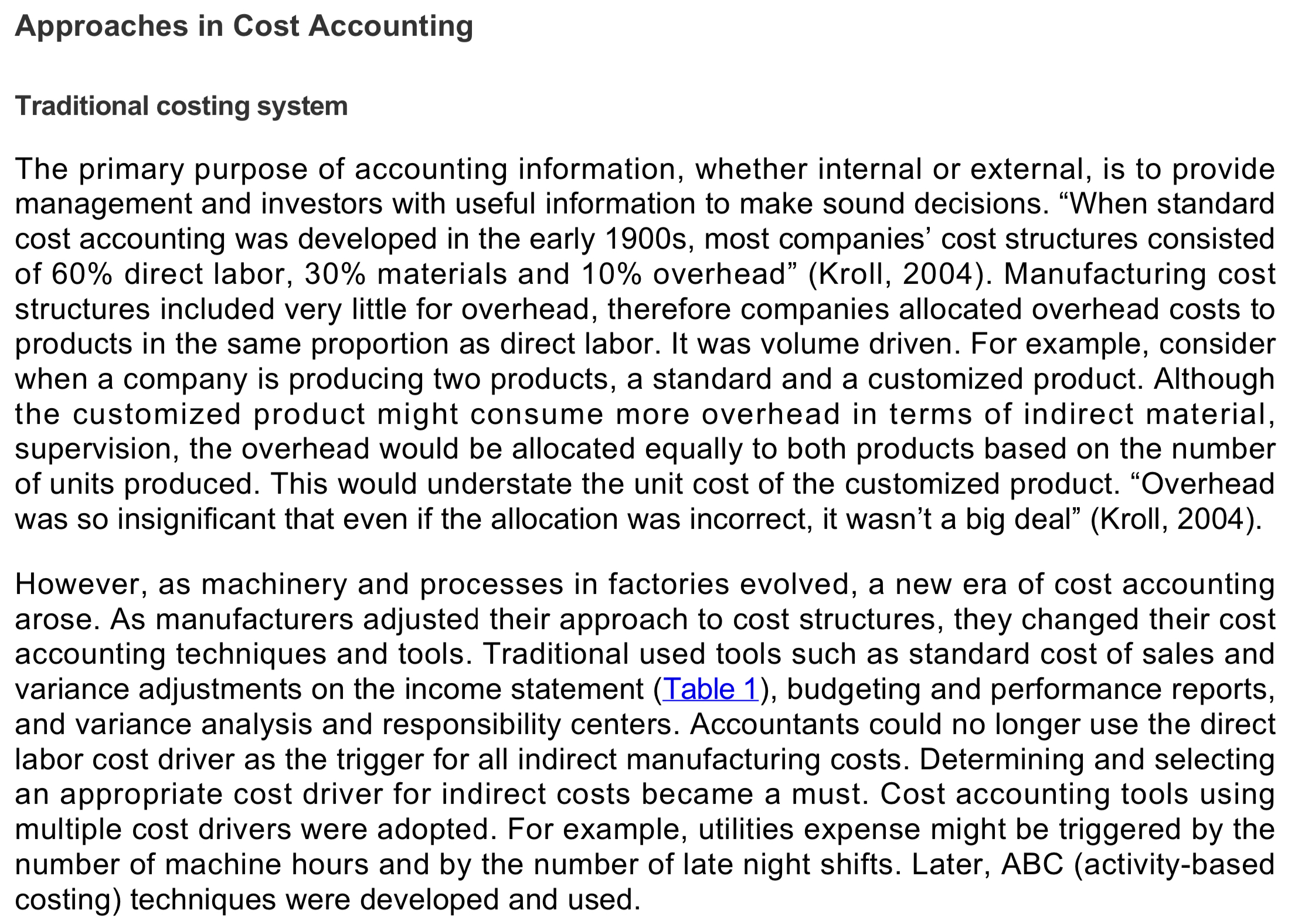

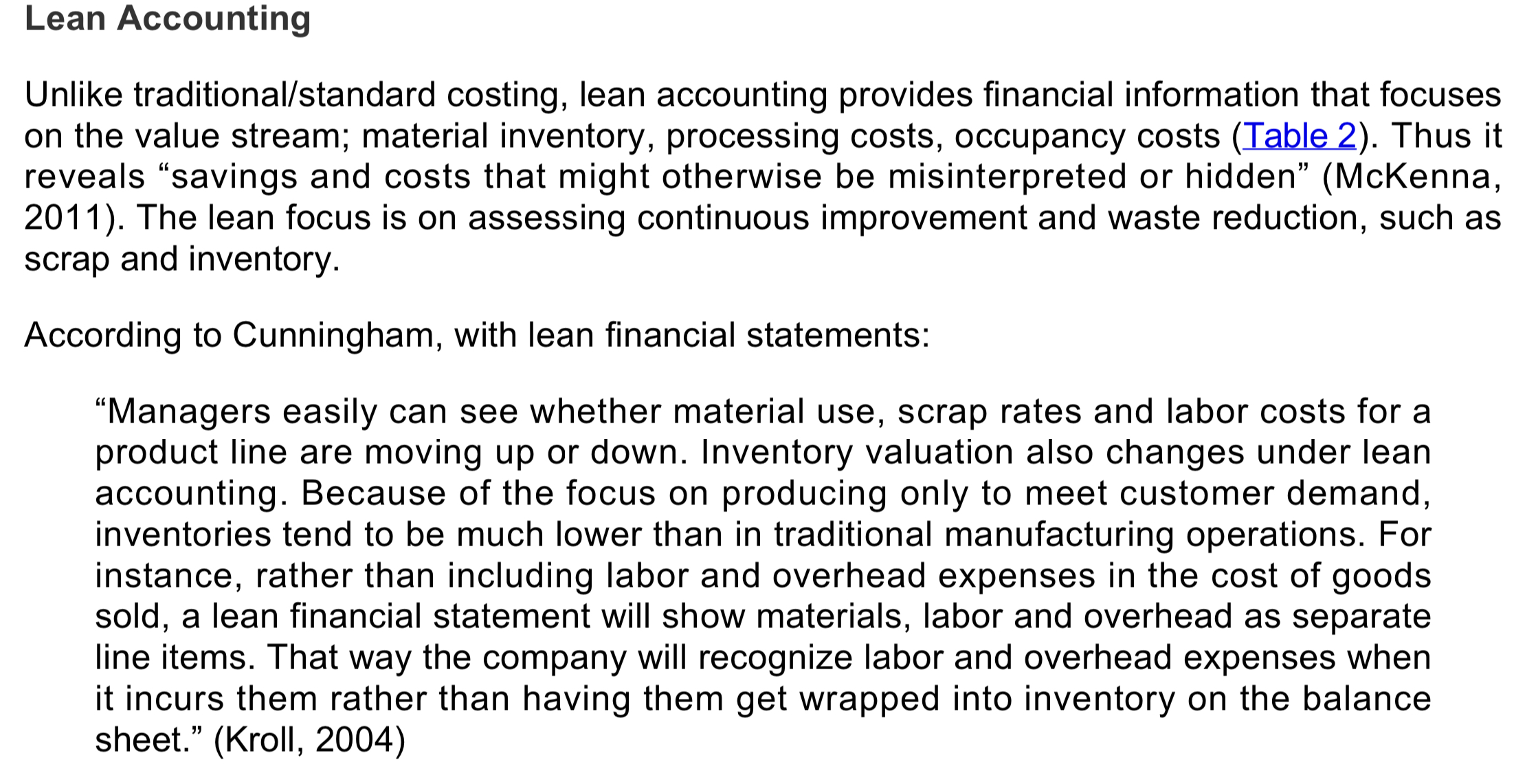

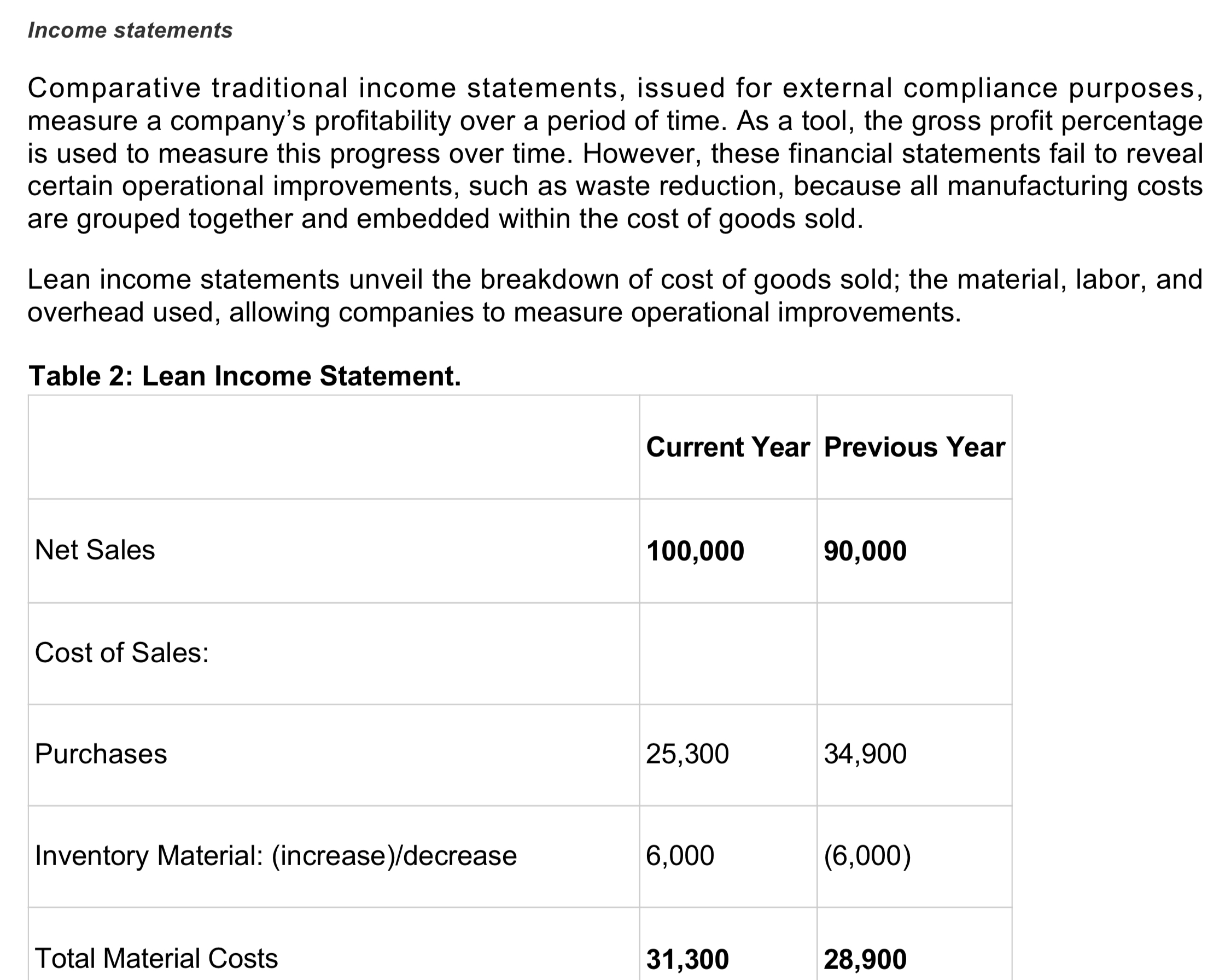

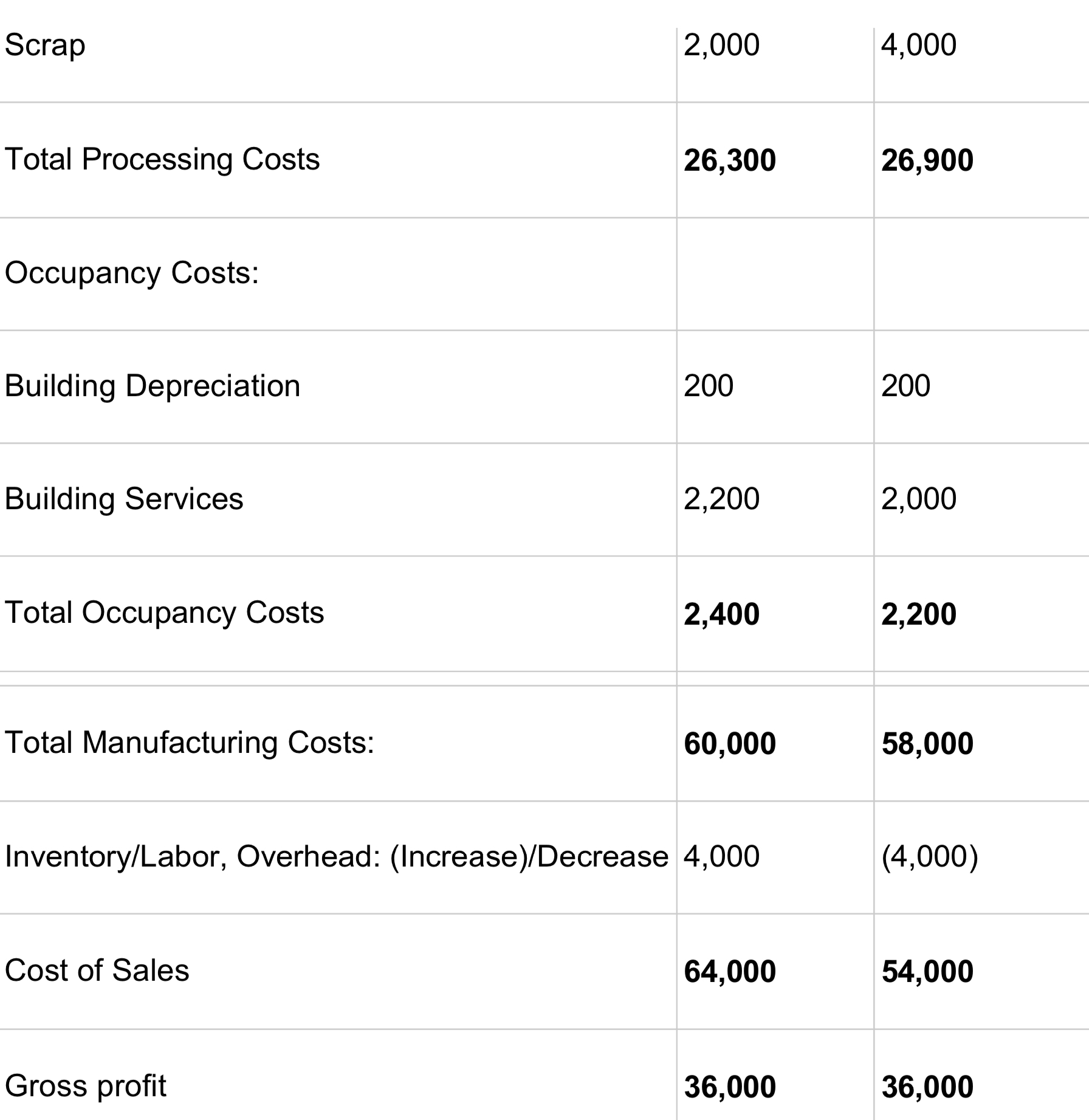

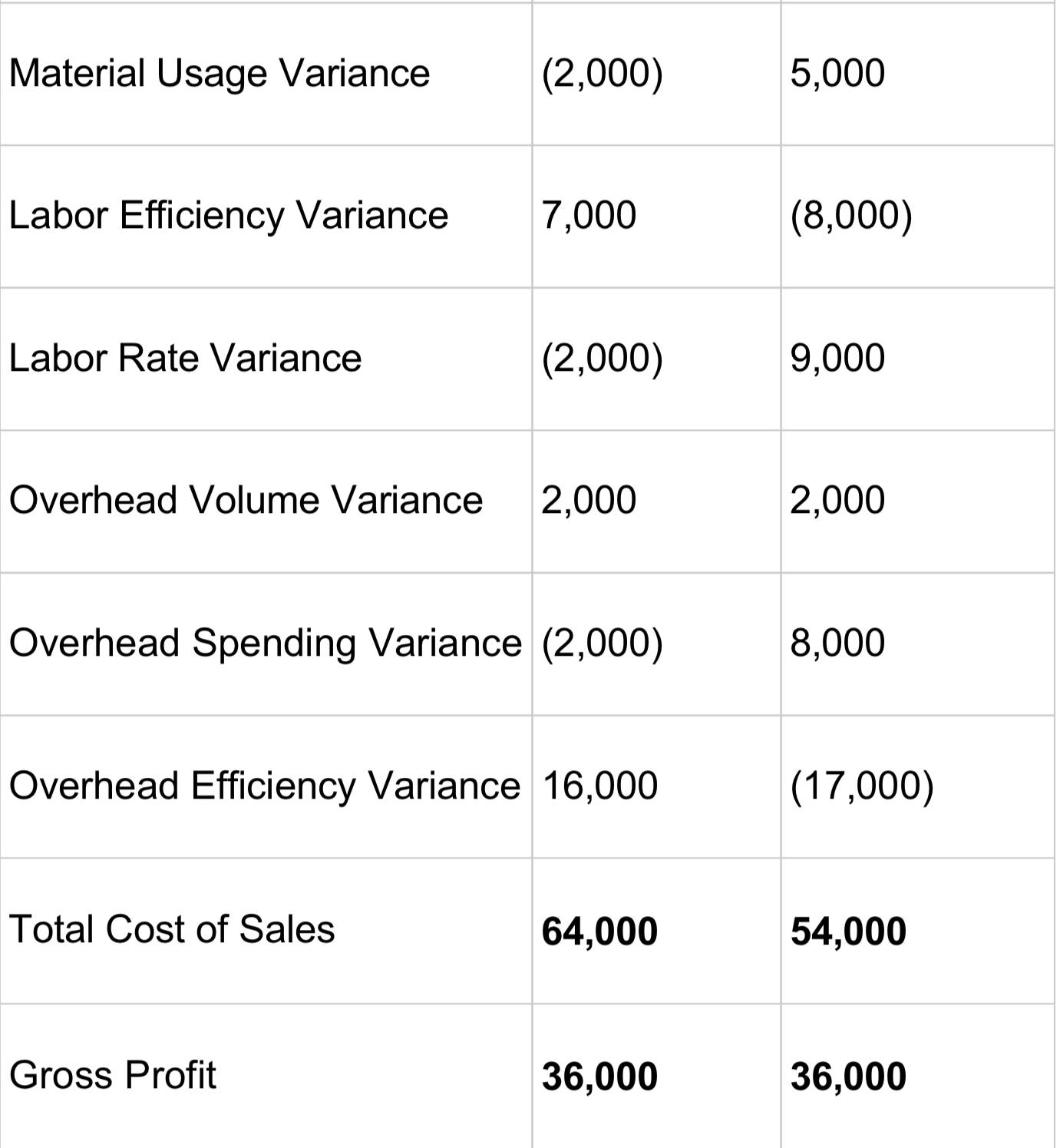

Table 1: Traditional Income Statement. Current Year Previous Year Net Sales 100,000 90,000 Less: Standard Cost of Sales 48,000 45,000 Material Price Variance (3,000) 10,000 Approaches in Cost Accounting Traditional costing system The primary purpose of accounting information, whether internal or external, is to provide management and investors with useful information to make sound decisions. \"When standard cost accounting was developed in the early 19003, most companies' cost structures consisted of 60% direct labor, 30% materials and 10% overhead\" (Kroll, 2004). Manufacturing cost structures included very little for overhead, therefore companies allocated overhead costs to products in the same proportion as direct labor. It was volume driven. For example, consider when a company is producing two products, a standard and a customized product. Although the customized product might consume more overhead in terms of indirect material, supervision, the overhead would be allocated equally to both products based on the number of units produced. This would understate the unit cost of the customized product. \"Overhead was so insignificant that even if the allocation was incorrect, it wasn't a big deal\" (Kroll, 2004). However, as machinery and processes in factories evolved, a new era of cost accounting arose. As manufacturers adjusted their approach to cost structures, they changed their cost accounting techniques and tools. Traditional used tools such as standard cost of sales and variance adjustments on the income statement (Table 1), budgeting and performance reports, and variance analysis and responsibility centers. Accountants could no longer use the direct labor cost driver as the trigger for all indirect manufacturing costs. Determining and selecting an appropriate cost driver for indirect costs became a must. Cost accounting tools using multiple cost drivers were adopted. For example, utilities expense might be triggered by the number of machine hours and by the number of late night shifts. Later, ABC (activity-based costing) techniques were developed and used. Lean Accounting Unlike traditional/standard costing, lean accounting provides financial information that focuses on the value stream; material inventory, processing costs, occupancy costs (Iahle_2). Thus it reveals \"savings and costs that might otherwise be misinterpreted or hidden\" (McKenna, 2011). The lean focus is on assessing continuous improvement and waste reduction, such as scrap and inventory. According to Cunningham, with lean financial statements: \"Managers easily can see whether material use, scrap rates and labor costs for a product line are moving up or down. Inventory valuation also changes under lean accounting. Because of the focus on producing only to meet customer demand, inventories tend to be much lower than in traditional manufacturing operations. For instance, rather than including labor and overhead expenses in the cost of goods sold, a lean financial statement will show materials, labor and overhead as separate line items. That way the company will recognize labor and overhead expenses when it incurs them rather than having them get wrapped into inventory on the balance sheet.\" (Kroll, 2004) Income statements Comparative traditional income statements, issued for external compliance purposes, measure a company's profitability over a period of time. As a tool, the gross profit percentage is used to measure this progress over time. However, these financial statements fail to reveal certain operational improvements, such as waste reduction, because all manufacturing costs are grouped together and embedded within the cost of goods sold. Lean income statements unveil the breakdown of cost of goods sold; the material, labor, and overhead used, allowing companies to measure operational improvements. Table 2: Lean Income Statement. Current Year Previous Year Net Sales 100,000 90,000 Cost of Sales: Purchases 25,300 34,900 Inventory Material: (increase)/decrease 6,000 (6,000) Total Material Costs 31,300 28,900 Scrap 2,000 4,000 Total Processing Costs 26,300 26,900 Occupancy Costs: Building Depreciation 200 200 Building Services 2,200 2,000 Total Occupancy Costs 2,400 2,200 Total Manufacturing Costs: 60,000 58,000 Inventory/Labor, Overhead: (Increase)/Decrease 4,000 (4,000) Cost of Sales 64,000 54,000 Gross profit 36,000 36,000Processing Costs: Factory Wages Factory Salaries Factory Benefits Services and Supplies Equipment and Depreciation 11,000 2,100 7,000 2,200 2,000 1 1,500 2,000 5,000 2,500 1,900 Material Usage Variance (2,000) Labor Efficiency Variance 7,000 Labor Rate Variance (2,000) Overhead Volume Variance 2,000 Overhead Spending Variance (2,000) Overhead Efficiency Variance 16,000 Total Cost of Sales 64,000 Gross Profit 36,000 5,000 (8,000) 9,000 2,000 8,000 (17,000) 54,000 36,000

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance