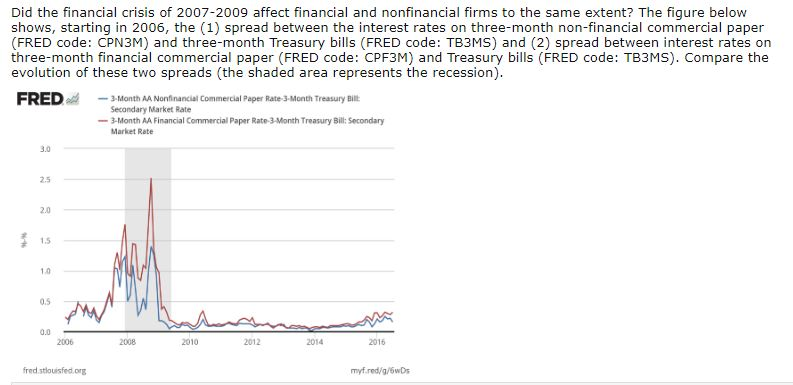

Which of the following statements are true about the risk spread? should vary directly with the bond's yield and inversely with its price. is also known as the default-risk premium. it is the difference between a bond's purchase price and selling price. it is the difference between the bond's yield and the yield on a U.S. Treasury bond of the same maturity. be lower for highly speculative bonds than investment grade bonds. Which of the following are conclusions drawn from interpreting the term structure of interest rates? Yields on long-term bonds tend to be larger than short-term bonds. The volatility in short-term bond yields tends to be smaller than those on long-term bonds. Short- and long-term interest rates tend to move in the same together. Short- and long-term interest rates tend to move in opposite directions. The volatility in short-term bond yields tends to be larger than those on long-term bonds. Which of the following statements pertaining to the yield curve is not true? The yield curve can be flat if interest rates are expected to remain unchanged in the future Yield curves usually slope upwards, reflecting expectations that interest rates will rise The yield curve can be downward sloping if interest rates are expected to fall in the future. The yield curve can be downward sloping if interest rates are expected to rise in the future. Yield curves usually slope upwards, reflecting expectations that interest rates will fall Did the financial crisis of 2007-2009 affect financial and nonfinancial firms to the same extent? The figure below shows, starting in 2006, the (1) spread between the interest rates on three-month (FRED code: CPN3M) and three-month Treasury bills (FRED code: TB3MS) and (2) spread between interest rates on three-month financial commercial paper (FRED code: CPF3M) and Treasury bills (FRED code: TB3MS). Compare the evolution of these two spreads (the shaded area represents the recession). FRED - 3 Month AA Nonfinancial Commercial Paper Rate 3-Month Treasury Bill Secondary Market Rate - 3-Month AA Financial Commercial Paper Rate 3 Month Treasury Bill: Secondary Market Rate 2006 2008 2010 2012 2014 2016 fred.stlouisfed.org myfred/g/5wDs Which of the following statements are true about the risk spread? should vary directly with the bond's yield and inversely with its price. is also known as the default-risk premium. it is the difference between a bond's purchase price and selling price. it is the difference between the bond's yield and the yield on a U.S. Treasury bond of the same maturity. be lower for highly speculative bonds than investment grade bonds. Which of the following are conclusions drawn from interpreting the term structure of interest rates? Yields on long-term bonds tend to be larger than short-term bonds. The volatility in short-term bond yields tends to be smaller than those on long-term bonds. Short- and long-term interest rates tend to move in the same together. Short- and long-term interest rates tend to move in opposite directions. The volatility in short-term bond yields tends to be larger than those on long-term bonds. Which of the following statements pertaining to the yield curve is not true? The yield curve can be flat if interest rates are expected to remain unchanged in the future Yield curves usually slope upwards, reflecting expectations that interest rates will rise The yield curve can be downward sloping if interest rates are expected to fall in the future. The yield curve can be downward sloping if interest rates are expected to rise in the future. Yield curves usually slope upwards, reflecting expectations that interest rates will fall Did the financial crisis of 2007-2009 affect financial and nonfinancial firms to the same extent? The figure below shows, starting in 2006, the (1) spread between the interest rates on three-month (FRED code: CPN3M) and three-month Treasury bills (FRED code: TB3MS) and (2) spread between interest rates on three-month financial commercial paper (FRED code: CPF3M) and Treasury bills (FRED code: TB3MS). Compare the evolution of these two spreads (the shaded area represents the recession). FRED - 3 Month AA Nonfinancial Commercial Paper Rate 3-Month Treasury Bill Secondary Market Rate - 3-Month AA Financial Commercial Paper Rate 3 Month Treasury Bill: Secondary Market Rate 2006 2008 2010 2012 2014 2016 fred.stlouisfed.org myfred/g/5wDs