Answered step by step

Verified Expert Solution

Question

1 Approved Answer

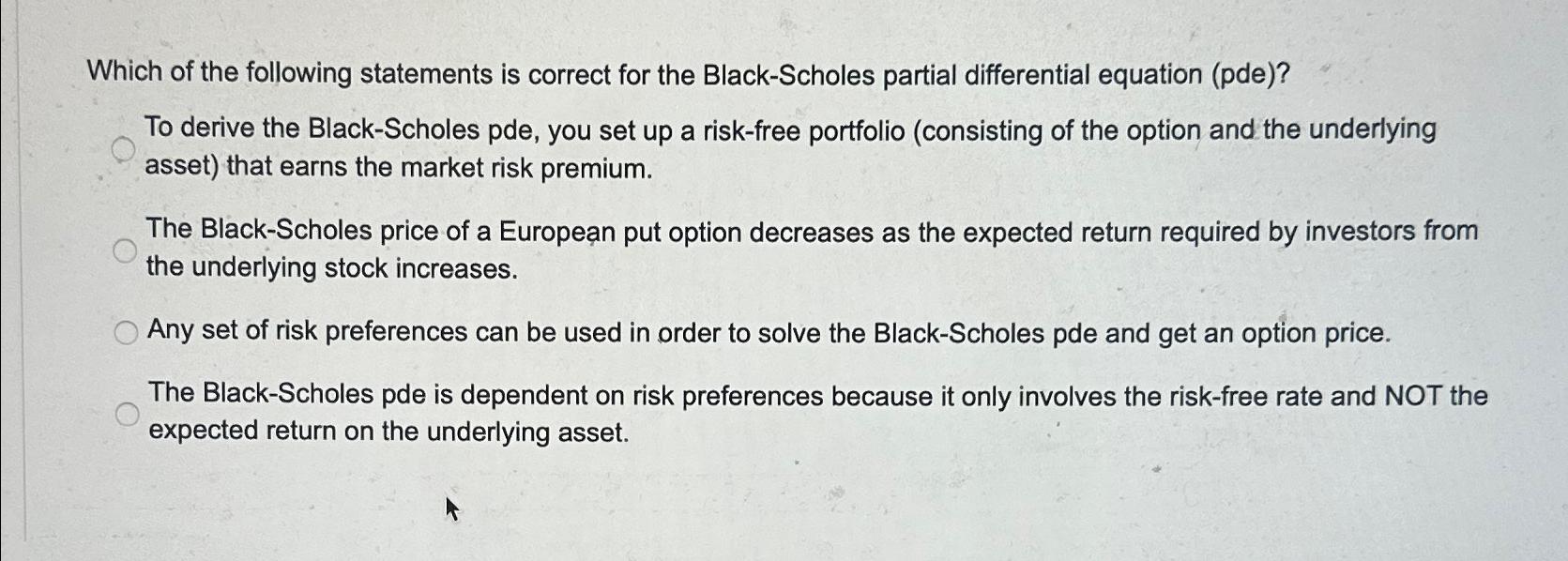

Which of the following statements is correct for the Black - Scholes partial differential equation ( pde ) ? To derive the Black - Scholes

Which of the following statements is correct for the BlackScholes partial differential equation pde

To derive the BlackScholes pde, you set up a riskfree portfolio consisting of the option and the underlying asset that earns the market risk premium.

The BlackScholes price of a European put option decreases as the expected return required by investors from the underlying stock increases.

Any set of risk preferences can be used in order to solve the BlackScholes pde and get an option price.

The BlackScholes pde is dependent on risk preferences because it only involves the riskfree rate and NOT the expected return on the underlying asset.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Term Structure Models A Graduate Course

Authors: Damir Filipovic

2009th Edition

364226915X, 978-3642269158