Answered step by step

Verified Expert Solution

Question

1 Approved Answer

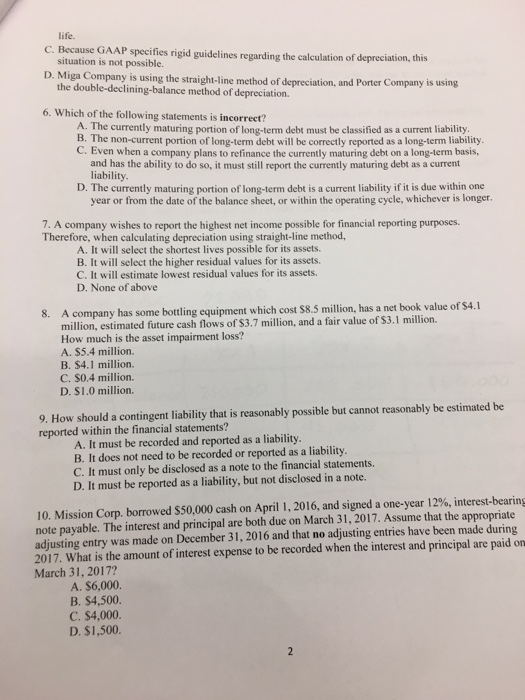

Which of the following statements is incorrect? The currently maturing portion long-term debt must be classified as a current liability. The non-current portion of long-term

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Advanced Audit And Assurance The Auditors Bible

Authors: Nhyira Premium IBL

1st Edition

B0BCXSXSJ7, 979-8829719432