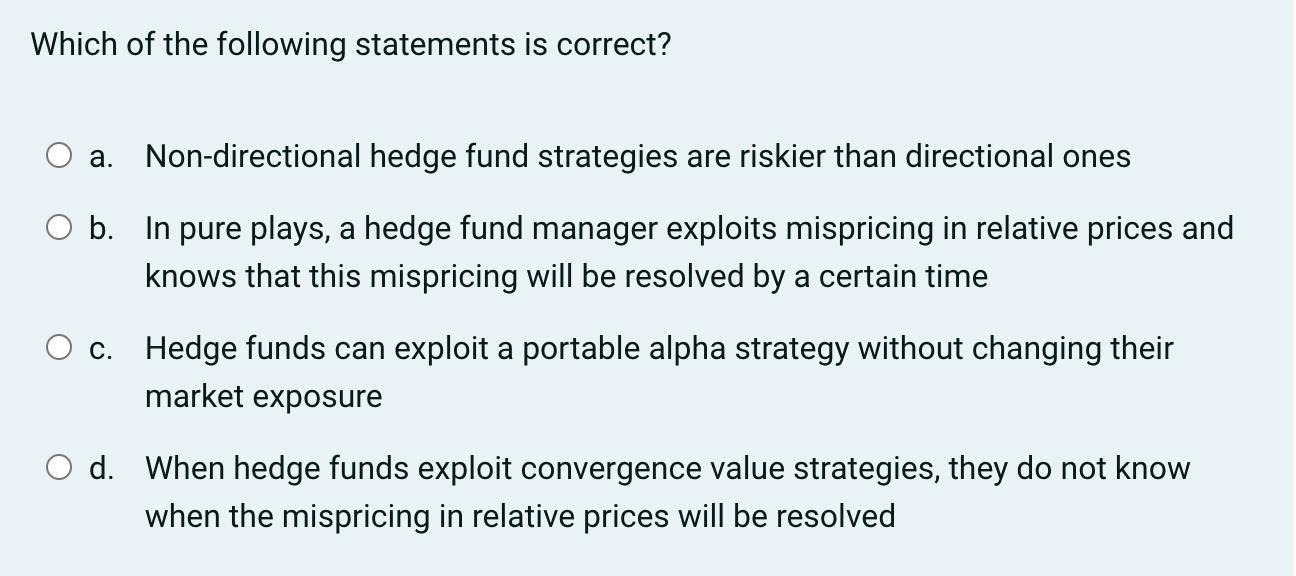

Which of the following statements is correct? a. Non-directional hedge fund strategies are riskier than directional ones O b. In pure plays, a hedge

Which of the following statements is correct? a. Non-directional hedge fund strategies are riskier than directional ones O b. In pure plays, a hedge fund manager exploits mispricing in relative prices and knows that this mispricing will be resolved by a certain time c. Hedge funds can exploit a portable alpha strategy without changing their market exposure O d. When hedge funds exploit convergence value strategies, they do not know when the mispricing in relative prices will be resolved

Step by Step Solution

3.59 Rating (163 Votes )

There are 3 Steps involved in it

Step: 1

option b In pure plays a hedg...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Lee J Krajewski, Larry P Ritzman, Manoj K Malhotra

9th edition

9788131728840, 136065767, 8131728846, 978-0136065760