Answered step by step

Verified Expert Solution

Question

1 Approved Answer

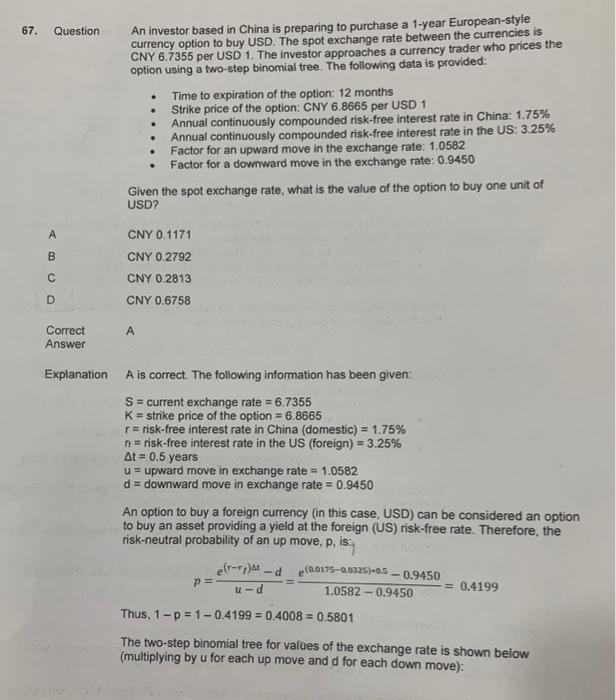

why we choose A, please i explain it step by step 67. Question Question A B C D Correct Answer Explanation A is correct. The

why we choose A, please i explain it step by step

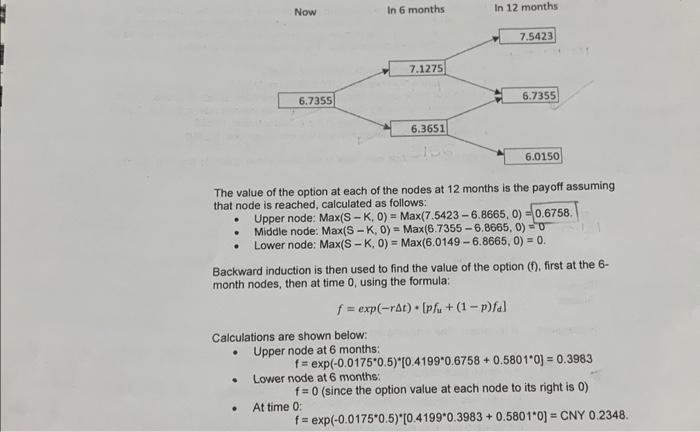

67. Question Question A B C D Correct Answer Explanation A is correct. The following information has been given: S=currentexchangerate=6.7355K=strikepriceoftheoption=6.8665r=risk-freeinterestrateinChina(domestic)=1.75%r=risk-freeinterestrateintheUS(foreign)=3.25%t=0.5yearsu=upwardmoveinexchangerate=1.0582d=downwardmoveinexchangerate=0.9450 An option to buy a foreign currency (in this case, USD) can be considered an option to buy an asset providing a yield at the foreign (US) risk-free rate. Therefore, the risk-neutral probability of an up move, p, is: p=ude(rrf)td=1.05820.9450e(0.01750.0325)0.50.9450=0.4199 Thus, 1p=10.4199=0.4008=0.5801 The two-step binomial tree for values of the exchange rate is shown below (multiplying by u for each up move and d for each down move): The value of the option at each of the nodes at 12 months is the payoff assuming that node is reached, calculated as follows: - Upper node: Max(SK,0)=Max(7.54236.8665,0)=0.6758. - Middle node: Max(SK,0)=Max(6.73556.8665,0)=0 - Lower node: Max(SK,0)=Max(6.01496.8665,0)=0. Backward induction is then used to find the value of the option ( f ), first at the 6month nodes, then at time 0 , using the formula: f=exp(rt)[pfu+(1p)fd] Calculations are shown below: - Upper node at 6 months: f=exp(0.01750.5)[0.41990.6758+0.58010]=0.3983 - Lower node at 6 months: f=0 (since the option value at each node to its right is 0 ) - At time 0: f=exp(0.01750.5)[0.41990.3983+0.58010]=CNY0.2348 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investments

Authors: Zvi Bodie, Alex Kane, Alan J. Marcus

7th Edition

007331465X, 978-0073314655