Question: XYZ is a calendar-year corporation that began business on January 1, 2018. For the year, it reported the following information in its current-year audited

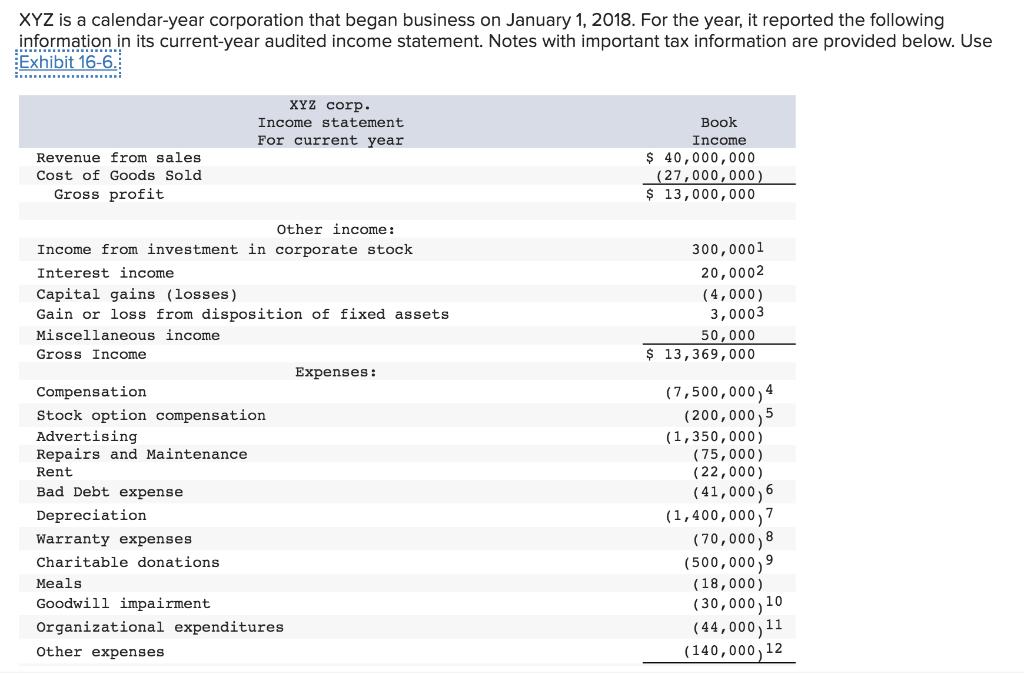

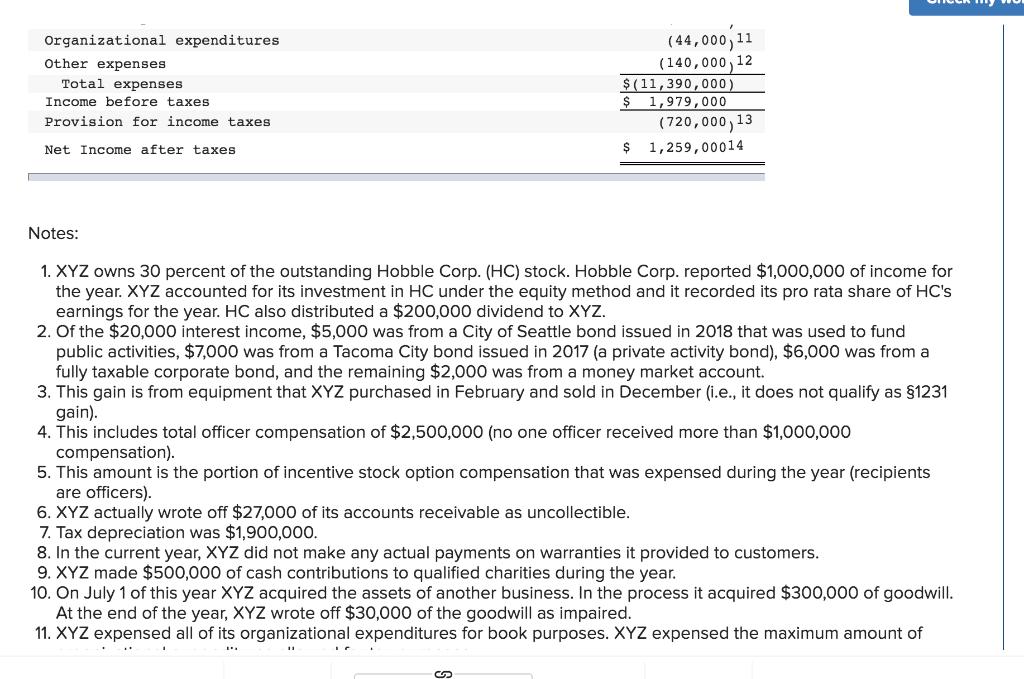

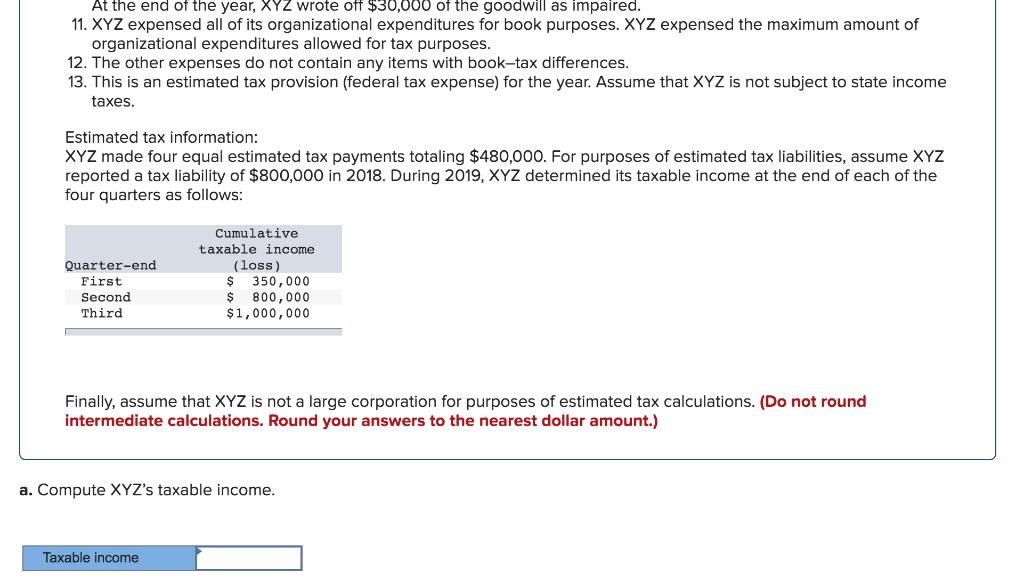

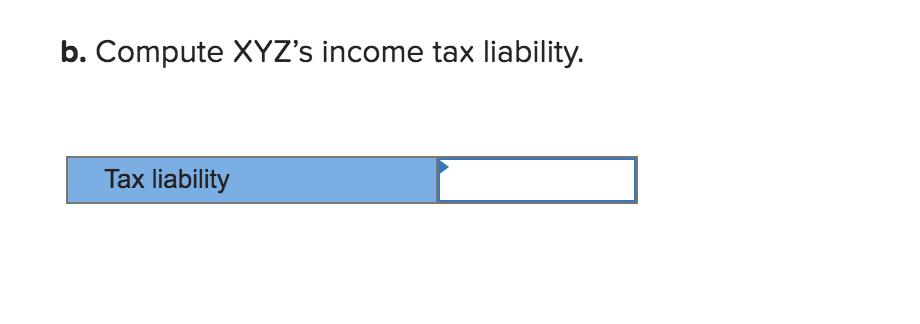

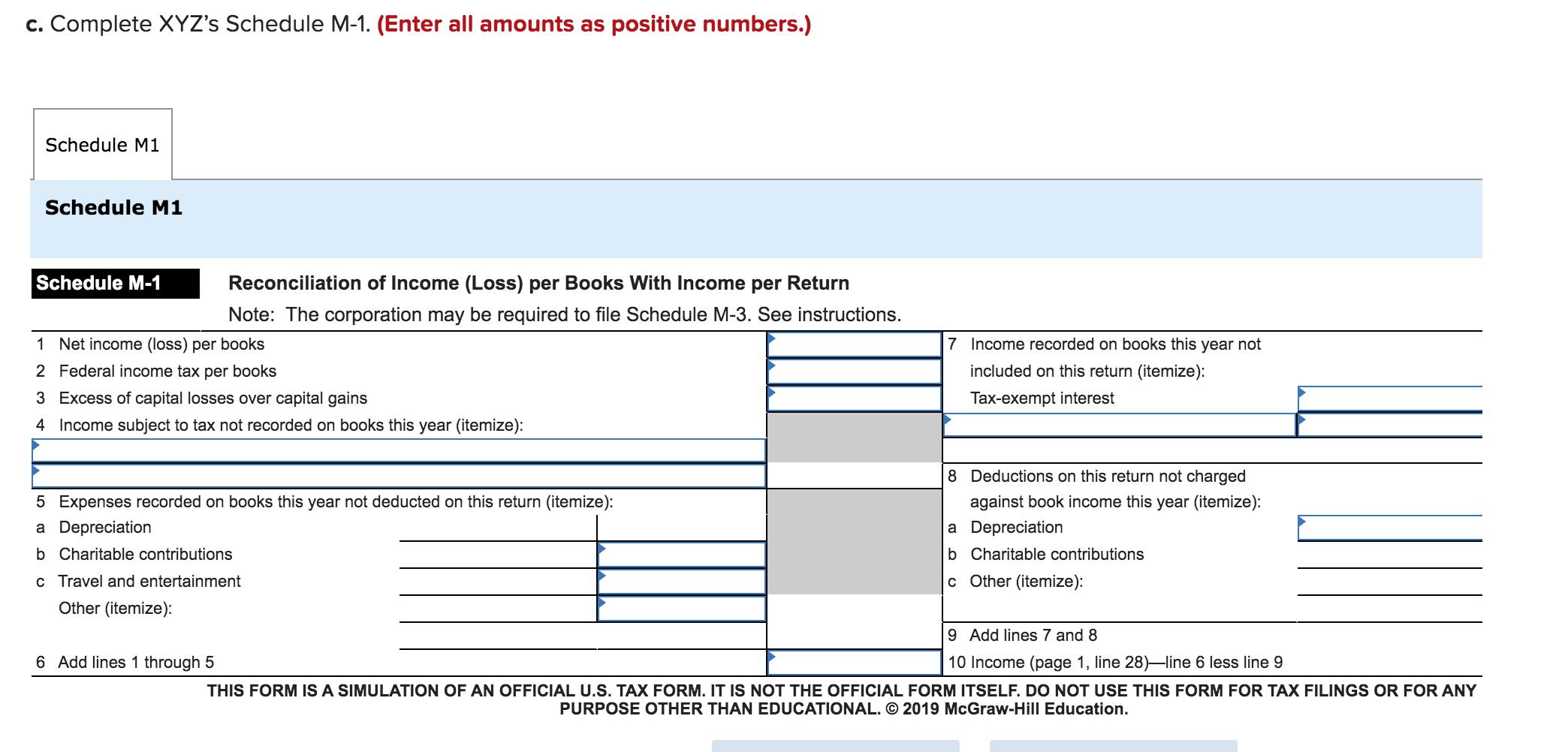

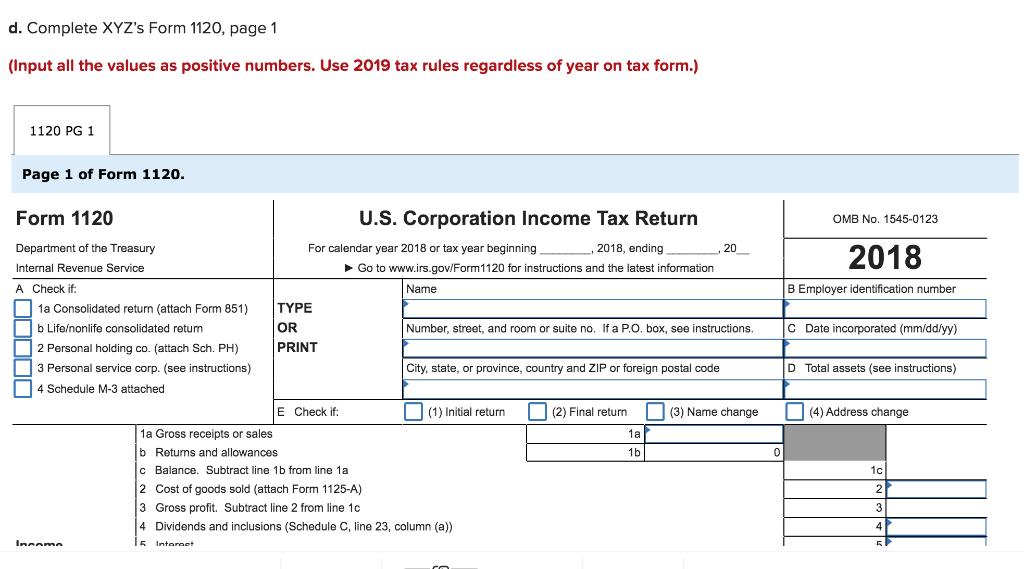

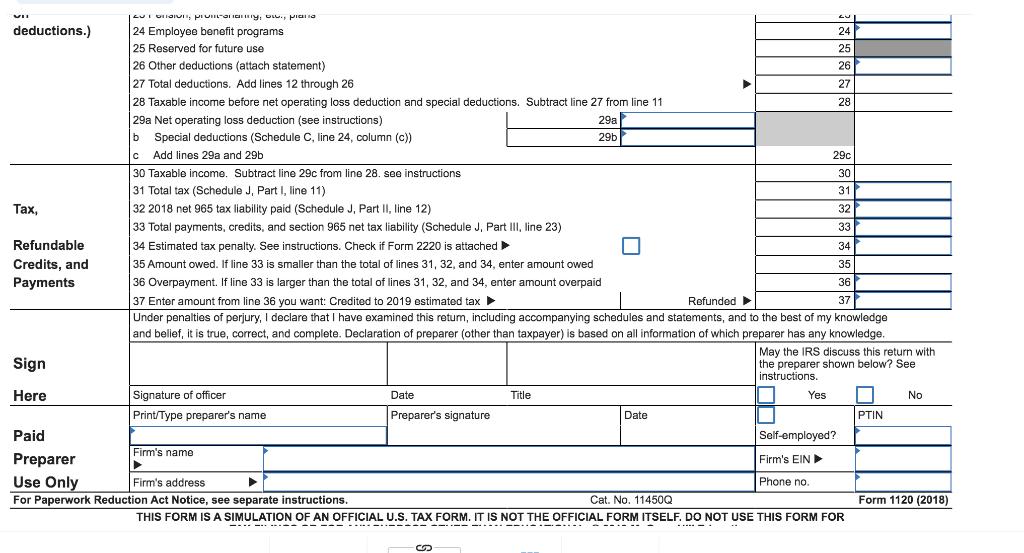

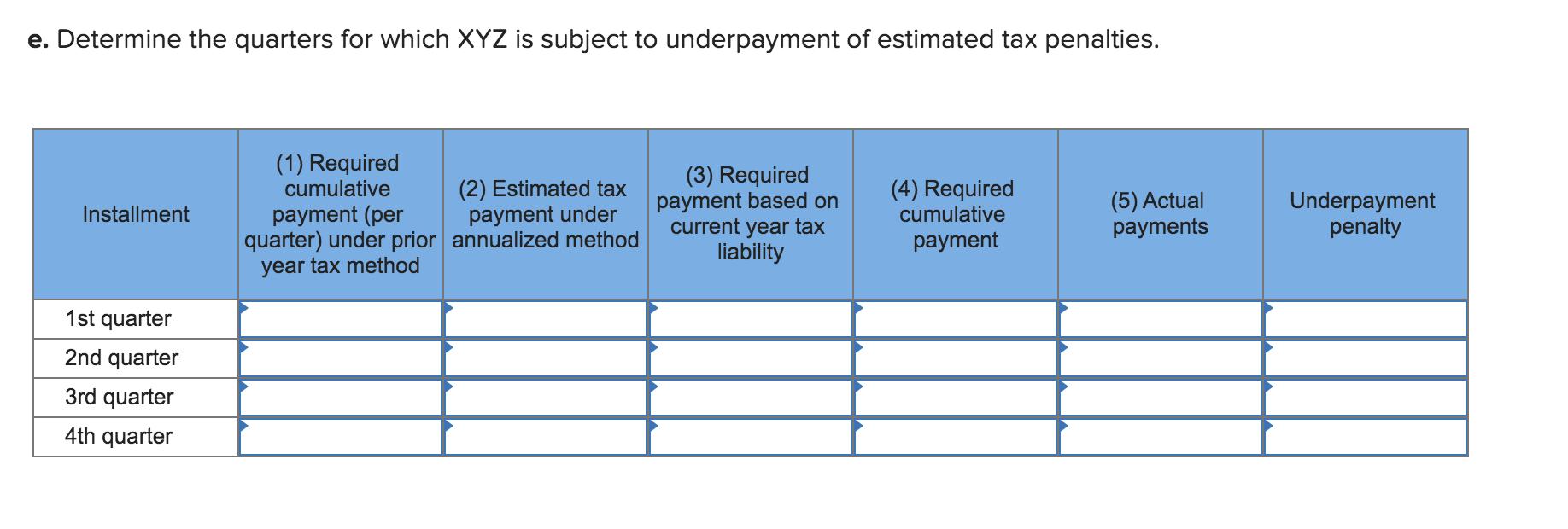

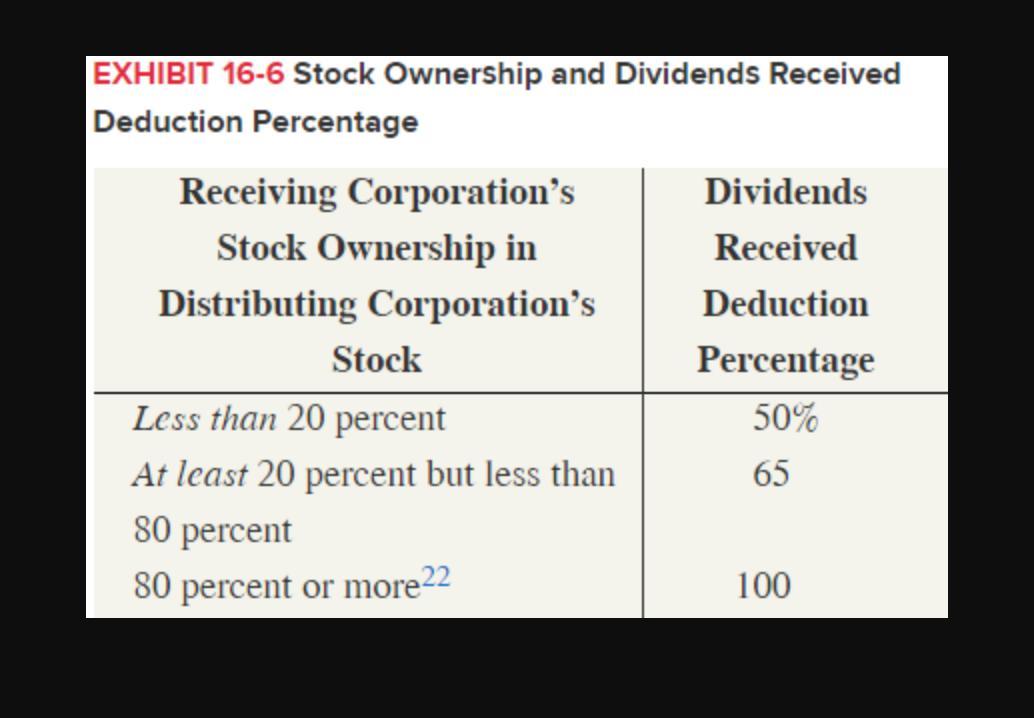

XYZ is a calendar-year corporation that began business on January 1, 2018. For the year, it reported the following information in its current-year audited income statement. Notes with important tax information are provided below. Use Exhibit 16-6. ................... XYZ corp. Income statement Book For current year Income $ 40,000,000 (27,000,000) $ 13,000,000 Revenue from sales Cost of Goods Sold Gross profit Other income: Income from investment in corporate stock 300,0001 Interest income 20,0002 Capital gains (losses) Gain or loss from disposition of fixed assets (4,000) 3,0003 Miscellaneous income 50,000 $ 13,369,000 Gross Income Expenses: (7,500,000,4 (200,000,5 (1,350,000) (75,000) (22,000) Compensation Stock option compensation Advertising Repairs and Maintenance Rent Bad Debt expense (41,000,6 (1,400,000,7 (70,000,8 (500,000,9 (18,000) Depreciation Warranty expenses Charitable donations Meals (30,000,10 (44,000,11 (140,000,12 Goodwill impairment Organizational expenditures Other expenses (44,000,11 (140,000, 12 $(11,390,000) $ Organizational expenditures Other expenses Total expenses Income before taxes 1,979,000 (720,000,13 $ 1,259,00014 Provision for income taxes Net Income after taxes Notes: 1. XYZ owns 30 percent of the outstanding Hobble Corp. (HC) stock. Hobble Corp. reported $1,000,000 of income for the year. XYZ accounted for its investment in HC under the equity method and it recorded its pro rata share of HC's earnings for the year. HC also distributed a $200,000 dividend to XYZ. 2. Of the $20,000 interest income, $5,000 was from a City of Seattle bond issued in 2018 that was used to fund public activities, $7,000 was from a Tacoma City bond issued in 2017 (a private activity bond), $6,000 was from a fully taxable corporate bond, and the remaining $2,000 was from a money market account. 3. This gain is from equipment that XYZ purchased in February and sold in December (i.e., it does not qualify as 1231 gain). 4. This includes total officer compensation of $2,500,000 (no one officer received more than $1,000,000 compensation). 5. This amount is the portion of incentive stock option compensation that was expensed during the year (recipients are officers). 6. XYZ actually wrote off $27,000 of its accounts receivable as uncollectible. 7. Tax depreciation was $1,900,000. 8. In the current year, XYZ did not make any actual payments on warranties it provided to customers. 9. XYZ made $500,000 of cash contributions to qualified charities during the year. 10. On July 1 of this year XYZ acquired the assets of another business. In the process it acquired $300,000 of goodwill. At the end of the year, XYZ wrote off $30,000 of the goodwill as impaired. 11. XYZ expensed all of its organizational expenditures for book purposes. XYZ expensed the maximum amount of At the end of the year, XYZ wrote off $30,000 of the goodwill as impaired. 11. XYZ expensed all of its organizational expenditures for book purposes. XYZ expensed the maximum amount of organizational expenditures allowed for tax purposes. 12. The other expenses do not contain any items with book-tax differences. 13. This is an estimated tax provision (federal tax expense) for the year. Assume that XYZ is not subject to state income taxes. Estimated tax information: XYZ made four equal estimated tax payments totaling $480,000. For purposes of estimated tax liabilities, assume XYZ reported a tax liability of $800,000 in 2018. During 2019, XYZ determined its taxable income at the end of each of the four quarters as follows: Cumulative taxable income (loss) $ Quarter-end First 350,000 Second Third $ 00, 000 $1,000,000 Finally, assume that XYZ is not a large corporation for purposes of estimated tax calculations. (Do not round intermediate calculations. Round your answers to the nearest dollar amount.) a. Compute XYZ's taxable income. Taxable income b. Compute XYZ's income tax liability. Tax liability c. Complete XYZ's Schedule M-1. (Enter all amounts as positive numbers.) Schedule M1 Schedule M1 Schedule M-1 Reconciliation of Income (Loss) per Books With Income per Return Note: The corporation may be required to file Schedule M-3. See instructions. 1 Net income (loss) per books 7 Income recorded on books this year not 2 Federal income tax per books included on this return (itemize): 3 Excess of capital losses over capital gains Tax-exempt interest 4 Income subject to tax not recorded on books this year (itemize): 8 Deductions on this return not charged 5 Expenses recorded on books this year not deducted on this return (itemize): against book income this year (itemize): a Depreciation a Depreciation b Charitable contributions b Charitable contributions c Travel and entertainment c Other (itemize): Other (itemize): 9 Add lines 7 and 8 6 Add lines 1 through 5 10 Income (page 1, line 28)-line 6 less line 9 THIS FORM IS A SIMULATION OF AN OFFICIAL U.S. TAX FORM. IT IS NOT THE OFFICIAL FORM ITSELF. DO NOT USE THIS FORM FOR TAX FILINGS OR FOR ANY PURPOSE OTHER THAN EDUCATIONAL. 2019 McGraw-Hill Education. d. Complete XYZ's Form 1120, page 1 (Input all the values as positive numbers. Use 2019 tax rules regardless of year on tax form.) 1120 PG 1 Page 1 of Form 1120. Form 1120 U.S. Corporation Income Tax Return OMB No. 1545-0123 Department of the Treasury For calendar year 2018 or tax year beginning 2018, ending ,20 2018 Internal Revenue Service Go to www.irs.gov/Form1120 for instructions and the latest information A Check if: B Employer identification number Name 1a Consolidated return (attach Form 851) b Life/nonlife consolidated retum OR Number, street, and room or suite no. If a P.O. box, see instructions. C Date incorporated (mm/dd/yy) | 2 Personal holding co. (attach Sch. PH) PRINT 3 Personal service corp. (see instructions) City, state, or province, country and ZIP or foreign postal code D Total assets (see instructions) 4 Schedule M-3 attached E Check if: (1) Initial return |(2) Final return O (3) Name change (4) Address change 1a Gross receipts or sales 1a b Returns and allowances 1b c Balance. Subtract line 1b from line 1a 1c 2 Cost of goods sold (attach Form 1125-A) 3 Gross profit. Subtract line 2 from line 1c 4 Dividends and inclusions (Schedule C, line 23, column (a)) 3 4 Income 5 Intereet deductions.) 24 Employee benefit programs 24 25 Reserved for future use 26 Other deductions (attach statement) 27 Total deductions. Add lines 12 through 26 28 Taxable income before net operating loss deduction and special deductions. Subtract line 27 from line 11 29a Net operating loss deduction (see instructions) b Special deductions (Schedule C, line 24, column (c) c Add lines 29a and 29b 30 Taxable income. Subtract line 29c from line 28. see instructions 25 26 27 28 29a 29b 29c 30 31 Total tax (Schedule J, Part I, line 11) 31 32 2018 net 965 tax liability paid (Schedule J, Part II, line 12) 33 Total payments, credits, and section 965 net tax liability (Schedule J, Part III, line 23) , 32 33 Refundable 34 Estimated tax penalty. See instructions. Check if Form 2220 is attached 34 Credits, and 35 Amount owed. If line 33 is smalier than the total of lines 31, 32, and 34, enter amount owed 35 Payments 36 Overpayment. If line 33 is larger than the total of lines 31, 32, and 34, enter amount overpaid 36 37 37 Enter amount from line 36 you want: Credited to 2019 estimated tax Under penalties of perjury, I declare that I have examined this retum, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge. Refunded May the IRS discuss this return with the preparer shown below? See instructions. Sign Here Signature of officer Date Title Yes No Print/Type preparer's name Preparer's signature Date PTIN Paid Self-employed? Firm's name Preparer Firm's EIN Use Only Firm's address Phone no. For Paperwork Reduction Act Notice, see separate instructions. Cat. No. 11450Q Form 1120 (2018) THIS FORM IS A SIMULATION OF AN OFFICIAL U.S. TAX FORM. IT IS NOT THE OFFICIAL FORM ITSELF. DO NOT USE THIS FORM FOR ---- -- - ----- -- ---------- ------ ------ --..-------- ----- -- -. - e. Determine the quarters for which XYZ is subject to underpayment of estimated tax penalties. (1) Required cumulative (3) Required payment based on current year tax liability (2) Estimated tax payment under (4) Required cumulative (5) Actual payments Underpayment penalty Installment payment (per quarter) under prior annualized method year tax method payment 1st quarter 2nd quarter 3rd quarter 4th quarter EXHIBIT 16-6 Stock Ownership and Dividends Received Deduction Percentage Receiving Corporation's Dividends Stock Ownership in Received Distributing Corporation's Deduction Stock Percentage Less than 20 percent 50% At least 20 percent but less than 65 80 percent 80 percent or more22 100 XYZ is a calendar-year corporation that began business on January 1, 2018. For the year, it reported the following information in its current-year audited income statement. Notes with important tax information are provided below. Use Exhibit 16-6. ................... XYZ corp. Income statement Book For current year Income $ 40,000,000 (27,000,000) $ 13,000,000 Revenue from sales Cost of Goods Sold Gross profit Other income: Income from investment in corporate stock 300,0001 Interest income 20,0002 Capital gains (losses) Gain or loss from disposition of fixed assets (4,000) 3,0003 Miscellaneous income 50,000 $ 13,369,000 Gross Income Expenses: (7,500,000,4 (200,000,5 (1,350,000) (75,000) (22,000) Compensation Stock option compensation Advertising Repairs and Maintenance Rent Bad Debt expense (41,000,6 (1,400,000,7 (70,000,8 (500,000,9 (18,000) Depreciation Warranty expenses Charitable donations Meals (30,000,10 (44,000,11 (140,000,12 Goodwill impairment Organizational expenditures Other expenses (44,000,11 (140,000, 12 $(11,390,000) $ Organizational expenditures Other expenses Total expenses Income before taxes 1,979,000 (720,000,13 $ 1,259,00014 Provision for income taxes Net Income after taxes Notes: 1. XYZ owns 30 percent of the outstanding Hobble Corp. (HC) stock. Hobble Corp. reported $1,000,000 of income for the year. XYZ accounted for its investment in HC under the equity method and it recorded its pro rata share of HC's earnings for the year. HC also distributed a $200,000 dividend to XYZ. 2. Of the $20,000 interest income, $5,000 was from a City of Seattle bond issued in 2018 that was used to fund public activities, $7,000 was from a Tacoma City bond issued in 2017 (a private activity bond), $6,000 was from a fully taxable corporate bond, and the remaining $2,000 was from a money market account. 3. This gain is from equipment that XYZ purchased in February and sold in December (i.e., it does not qualify as 1231 gain). 4. This includes total officer compensation of $2,500,000 (no one officer received more than $1,000,000 compensation). 5. This amount is the portion of incentive stock option compensation that was expensed during the year (recipients are officers). 6. XYZ actually wrote off $27,000 of its accounts receivable as uncollectible. 7. Tax depreciation was $1,900,000. 8. In the current year, XYZ did not make any actual payments on warranties it provided to customers. 9. XYZ made $500,000 of cash contributions to qualified charities during the year. 10. On July 1 of this year XYZ acquired the assets of another business. In the process it acquired $300,000 of goodwill. At the end of the year, XYZ wrote off $30,000 of the goodwill as impaired. 11. XYZ expensed all of its organizational expenditures for book purposes. XYZ expensed the maximum amount of At the end of the year, XYZ wrote off $30,000 of the goodwill as impaired. 11. XYZ expensed all of its organizational expenditures for book purposes. XYZ expensed the maximum amount of organizational expenditures allowed for tax purposes. 12. The other expenses do not contain any items with book-tax differences. 13. This is an estimated tax provision (federal tax expense) for the year. Assume that XYZ is not subject to state income taxes. Estimated tax information: XYZ made four equal estimated tax payments totaling $480,000. For purposes of estimated tax liabilities, assume XYZ reported a tax liability of $800,000 in 2018. During 2019, XYZ determined its taxable income at the end of each of the four quarters as follows: Cumulative taxable income (loss) $ Quarter-end First 350,000 Second Third $ 00, 000 $1,000,000 Finally, assume that XYZ is not a large corporation for purposes of estimated tax calculations. (Do not round intermediate calculations. Round your answers to the nearest dollar amount.) a. Compute XYZ's taxable income. Taxable income b. Compute XYZ's income tax liability. Tax liability c. Complete XYZ's Schedule M-1. (Enter all amounts as positive numbers.) Schedule M1 Schedule M1 Schedule M-1 Reconciliation of Income (Loss) per Books With Income per Return Note: The corporation may be required to file Schedule M-3. See instructions. 1 Net income (loss) per books 7 Income recorded on books this year not 2 Federal income tax per books included on this return (itemize): 3 Excess of capital losses over capital gains Tax-exempt interest 4 Income subject to tax not recorded on books this year (itemize): 8 Deductions on this return not charged 5 Expenses recorded on books this year not deducted on this return (itemize): against book income this year (itemize): a Depreciation a Depreciation b Charitable contributions b Charitable contributions c Travel and entertainment c Other (itemize): Other (itemize): 9 Add lines 7 and 8 6 Add lines 1 through 5 10 Income (page 1, line 28)-line 6 less line 9 THIS FORM IS A SIMULATION OF AN OFFICIAL U.S. TAX FORM. IT IS NOT THE OFFICIAL FORM ITSELF. DO NOT USE THIS FORM FOR TAX FILINGS OR FOR ANY PURPOSE OTHER THAN EDUCATIONAL. 2019 McGraw-Hill Education. d. Complete XYZ's Form 1120, page 1 (Input all the values as positive numbers. Use 2019 tax rules regardless of year on tax form.) 1120 PG 1 Page 1 of Form 1120. Form 1120 U.S. Corporation Income Tax Return OMB No. 1545-0123 Department of the Treasury For calendar year 2018 or tax year beginning 2018, ending ,20 2018 Internal Revenue Service Go to www.irs.gov/Form1120 for instructions and the latest information A Check if: B Employer identification number Name 1a Consolidated return (attach Form 851) b Life/nonlife consolidated retum OR Number, street, and room or suite no. If a P.O. box, see instructions. C Date incorporated (mm/dd/yy) | 2 Personal holding co. (attach Sch. PH) PRINT 3 Personal service corp. (see instructions) City, state, or province, country and ZIP or foreign postal code D Total assets (see instructions) 4 Schedule M-3 attached E Check if: (1) Initial return |(2) Final return O (3) Name change (4) Address change 1a Gross receipts or sales 1a b Returns and allowances 1b c Balance. Subtract line 1b from line 1a 1c 2 Cost of goods sold (attach Form 1125-A) 3 Gross profit. Subtract line 2 from line 1c 4 Dividends and inclusions (Schedule C, line 23, column (a)) 3 4 Income 5 Intereet deductions.) 24 Employee benefit programs 24 25 Reserved for future use 26 Other deductions (attach statement) 27 Total deductions. Add lines 12 through 26 28 Taxable income before net operating loss deduction and special deductions. Subtract line 27 from line 11 29a Net operating loss deduction (see instructions) b Special deductions (Schedule C, line 24, column (c) c Add lines 29a and 29b 30 Taxable income. Subtract line 29c from line 28. see instructions 25 26 27 28 29a 29b 29c 30 31 Total tax (Schedule J, Part I, line 11) 31 32 2018 net 965 tax liability paid (Schedule J, Part II, line 12) 33 Total payments, credits, and section 965 net tax liability (Schedule J, Part III, line 23) , 32 33 Refundable 34 Estimated tax penalty. See instructions. Check if Form 2220 is attached 34 Credits, and 35 Amount owed. If line 33 is smalier than the total of lines 31, 32, and 34, enter amount owed 35 Payments 36 Overpayment. If line 33 is larger than the total of lines 31, 32, and 34, enter amount overpaid 36 37 37 Enter amount from line 36 you want: Credited to 2019 estimated tax Under penalties of perjury, I declare that I have examined this retum, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge. Refunded May the IRS discuss this return with the preparer shown below? See instructions. Sign Here Signature of officer Date Title Yes No Print/Type preparer's name Preparer's signature Date PTIN Paid Self-employed? Firm's name Preparer Firm's EIN Use Only Firm's address Phone no. For Paperwork Reduction Act Notice, see separate instructions. Cat. No. 11450Q Form 1120 (2018) THIS FORM IS A SIMULATION OF AN OFFICIAL U.S. TAX FORM. IT IS NOT THE OFFICIAL FORM ITSELF. DO NOT USE THIS FORM FOR ---- -- - ----- -- ---------- ------ ------ --..-------- ----- -- -. - e. Determine the quarters for which XYZ is subject to underpayment of estimated tax penalties. (1) Required cumulative (3) Required payment based on current year tax liability (2) Estimated tax payment under (4) Required cumulative (5) Actual payments Underpayment penalty Installment payment (per quarter) under prior annualized method year tax method payment 1st quarter 2nd quarter 3rd quarter 4th quarter EXHIBIT 16-6 Stock Ownership and Dividends Received Deduction Percentage Receiving Corporation's Dividends Stock Ownership in Received Distributing Corporation's Deduction Stock Percentage Less than 20 percent 50% At least 20 percent but less than 65 80 percent 80 percent or more22 100 XYZ is a calendar-year corporation that began business on January 1, 2018. For the year, it reported the following information in its current-year audited income statement. Notes with important tax information are provided below. Use Exhibit 16-6. ................... XYZ corp. Income statement Book For current year Income $ 40,000,000 (27,000,000) $ 13,000,000 Revenue from sales Cost of Goods Sold Gross profit Other income: Income from investment in corporate stock 300,0001 Interest income 20,0002 Capital gains (losses) Gain or loss from disposition of fixed assets (4,000) 3,0003 Miscellaneous income 50,000 $ 13,369,000 Gross Income Expenses: (7,500,000,4 (200,000,5 (1,350,000) (75,000) (22,000) Compensation Stock option compensation Advertising Repairs and Maintenance Rent Bad Debt expense (41,000,6 (1,400,000,7 (70,000,8 (500,000,9 (18,000) Depreciation Warranty expenses Charitable donations Meals (30,000,10 (44,000,11 (140,000,12 Goodwill impairment Organizational expenditures Other expenses (44,000,11 (140,000, 12 $(11,390,000) $ Organizational expenditures Other expenses Total expenses Income before taxes 1,979,000 (720,000,13 $ 1,259,00014 Provision for income taxes Net Income after taxes Notes: 1. XYZ owns 30 percent of the outstanding Hobble Corp. (HC) stock. Hobble Corp. reported $1,000,000 of income for the year. XYZ accounted for its investment in HC under the equity method and it recorded its pro rata share of HC's earnings for the year. HC also distributed a $200,000 dividend to XYZ. 2. Of the $20,000 interest income, $5,000 was from a City of Seattle bond issued in 2018 that was used to fund public activities, $7,000 was from a Tacoma City bond issued in 2017 (a private activity bond), $6,000 was from a fully taxable corporate bond, and the remaining $2,000 was from a money market account. 3. This gain is from equipment that XYZ purchased in February and sold in December (i.e., it does not qualify as 1231 gain). 4. This includes total officer compensation of $2,500,000 (no one officer received more than $1,000,000 compensation). 5. This amount is the portion of incentive stock option compensation that was expensed during the year (recipients are officers). 6. XYZ actually wrote off $27,000 of its accounts receivable as uncollectible. 7. Tax depreciation was $1,900,000. 8. In the current year, XYZ did not make any actual payments on warranties it provided to customers. 9. XYZ made $500,000 of cash contributions to qualified charities during the year. 10. On July 1 of this year XYZ acquired the assets of another business. In the process it acquired $300,000 of goodwill. At the end of the year, XYZ wrote off $30,000 of the goodwill as impaired. 11. XYZ expensed all of its organizational expenditures for book purposes. XYZ expensed the maximum amount of At the end of the year, XYZ wrote off $30,000 of the goodwill as impaired. 11. XYZ expensed all of its organizational expenditures for book purposes. XYZ expensed the maximum amount of organizational expenditures allowed for tax purposes. 12. The other expenses do not contain any items with book-tax differences. 13. This is an estimated tax provision (federal tax expense) for the year. Assume that XYZ is not subject to state income taxes. Estimated tax information: XYZ made four equal estimated tax payments totaling $480,000. For purposes of estimated tax liabilities, assume XYZ reported a tax liability of $800,000 in 2018. During 2019, XYZ determined its taxable income at the end of each of the four quarters as follows: Cumulative taxable income (loss) $ Quarter-end First 350,000 Second Third $ 00, 000 $1,000,000 Finally, assume that XYZ is not a large corporation for purposes of estimated tax calculations. (Do not round intermediate calculations. Round your answers to the nearest dollar amount.) a. Compute XYZ's taxable income. Taxable income b. Compute XYZ's income tax liability. Tax liability c. Complete XYZ's Schedule M-1. (Enter all amounts as positive numbers.) Schedule M1 Schedule M1 Schedule M-1 Reconciliation of Income (Loss) per Books With Income per Return Note: The corporation may be required to file Schedule M-3. See instructions. 1 Net income (loss) per books 7 Income recorded on books this year not 2 Federal income tax per books included on this return (itemize): 3 Excess of capital losses over capital gains Tax-exempt interest 4 Income subject to tax not recorded on books this year (itemize): 8 Deductions on this return not charged 5 Expenses recorded on books this year not deducted on this return (itemize): against book income this year (itemize): a Depreciation a Depreciation b Charitable contributions b Charitable contributions c Travel and entertainment c Other (itemize): Other (itemize): 9 Add lines 7 and 8 6 Add lines 1 through 5 10 Income (page 1, line 28)-line 6 less line 9 THIS FORM IS A SIMULATION OF AN OFFICIAL U.S. TAX FORM. IT IS NOT THE OFFICIAL FORM ITSELF. DO NOT USE THIS FORM FOR TAX FILINGS OR FOR ANY PURPOSE OTHER THAN EDUCATIONAL. 2019 McGraw-Hill Education. d. Complete XYZ's Form 1120, page 1 (Input all the values as positive numbers. Use 2019 tax rules regardless of year on tax form.) 1120 PG 1 Page 1 of Form 1120. Form 1120 U.S. Corporation Income Tax Return OMB No. 1545-0123 Department of the Treasury For calendar year 2018 or tax year beginning 2018, ending ,20 2018 Internal Revenue Service Go to www.irs.gov/Form1120 for instructions and the latest information A Check if: B Employer identification number Name 1a Consolidated return (attach Form 851) b Life/nonlife consolidated retum OR Number, street, and room or suite no. If a P.O. box, see instructions. C Date incorporated (mm/dd/yy) | 2 Personal holding co. (attach Sch. PH) PRINT 3 Personal service corp. (see instructions) City, state, or province, country and ZIP or foreign postal code D Total assets (see instructions) 4 Schedule M-3 attached E Check if: (1) Initial return |(2) Final return O (3) Name change (4) Address change 1a Gross receipts or sales 1a b Returns and allowances 1b c Balance. Subtract line 1b from line 1a 1c 2 Cost of goods sold (attach Form 1125-A) 3 Gross profit. Subtract line 2 from line 1c 4 Dividends and inclusions (Schedule C, line 23, column (a)) 3 4 Income 5 Intereet deductions.) 24 Employee benefit programs 24 25 Reserved for future use 26 Other deductions (attach statement) 27 Total deductions. Add lines 12 through 26 28 Taxable income before net operating loss deduction and special deductions. Subtract line 27 from line 11 29a Net operating loss deduction (see instructions) b Special deductions (Schedule C, line 24, column (c) c Add lines 29a and 29b 30 Taxable income. Subtract line 29c from line 28. see instructions 25 26 27 28 29a 29b 29c 30 31 Total tax (Schedule J, Part I, line 11) 31 32 2018 net 965 tax liability paid (Schedule J, Part II, line 12) 33 Total payments, credits, and section 965 net tax liability (Schedule J, Part III, line 23) , 32 33 Refundable 34 Estimated tax penalty. See instructions. Check if Form 2220 is attached 34 Credits, and 35 Amount owed. If line 33 is smalier than the total of lines 31, 32, and 34, enter amount owed 35 Payments 36 Overpayment. If line 33 is larger than the total of lines 31, 32, and 34, enter amount overpaid 36 37 37 Enter amount from line 36 you want: Credited to 2019 estimated tax Under penalties of perjury, I declare that I have examined this retum, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge. Refunded May the IRS discuss this return with the preparer shown below? See instructions. Sign Here Signature of officer Date Title Yes No Print/Type preparer's name Preparer's signature Date PTIN Paid Self-employed? Firm's name Preparer Firm's EIN Use Only Firm's address Phone no. For Paperwork Reduction Act Notice, see separate instructions. Cat. No. 11450Q Form 1120 (2018) THIS FORM IS A SIMULATION OF AN OFFICIAL U.S. TAX FORM. IT IS NOT THE OFFICIAL FORM ITSELF. DO NOT USE THIS FORM FOR ---- -- - ----- -- ---------- ------ ------ --..-------- ----- -- -. - e. Determine the quarters for which XYZ is subject to underpayment of estimated tax penalties. (1) Required cumulative (3) Required payment based on current year tax liability (2) Estimated tax payment under (4) Required cumulative (5) Actual payments Underpayment penalty Installment payment (per quarter) under prior annualized method year tax method payment 1st quarter 2nd quarter 3rd quarter 4th quarter EXHIBIT 16-6 Stock Ownership and Dividends Received Deduction Percentage Receiving Corporation's Dividends Stock Ownership in Received Distributing Corporation's Deduction Stock Percentage Less than 20 percent 50% At least 20 percent but less than 65 80 percent 80 percent or more22 100 XYZ is a calendar-year corporation that began business on January 1, 2018. For the year, it reported the following information in its current-year audited income statement. Notes with important tax information are provided below. Use Exhibit 16-6. ................... XYZ corp. Income statement Book For current year Income $ 40,000,000 (27,000,000) $ 13,000,000 Revenue from sales Cost of Goods Sold Gross profit Other income: Income from investment in corporate stock 300,0001 Interest income 20,0002 Capital gains (losses) Gain or loss from disposition of fixed assets (4,000) 3,0003 Miscellaneous income 50,000 $ 13,369,000 Gross Income Expenses: (7,500,000,4 (200,000,5 (1,350,000) (75,000) (22,000) Compensation Stock option compensation Advertising Repairs and Maintenance Rent Bad Debt expense (41,000,6 (1,400,000,7 (70,000,8 (500,000,9 (18,000) Depreciation Warranty expenses Charitable donations Meals (30,000,10 (44,000,11 (140,000,12 Goodwill impairment Organizational expenditures Other expenses (44,000,11 (140,000, 12 $(11,390,000) $ Organizational expenditures Other expenses Total expenses Income before taxes 1,979,000 (720,000,13 $ 1,259,00014 Provision for income taxes Net Income after taxes Notes: 1. XYZ owns 30 percent of the outstanding Hobble Corp. (HC) stock. Hobble Corp. reported $1,000,000 of income for the year. XYZ accounted for its investment in HC under the equity method and it recorded its pro rata share of HC's earnings for the year. HC also distributed a $200,000 dividend to XYZ. 2. Of the $20,000 interest income, $5,000 was from a City of Seattle bond issued in 2018 that was used to fund public activities, $7,000 was from a Tacoma City bond issued in 2017 (a private activity bond), $6,000 was from a fully taxable corporate bond, and the remaining $2,000 was from a money market account. 3. This gain is from equipment that XYZ purchased in February and sold in December (i.e., it does not qualify as 1231 gain). 4. This includes total officer compensation of $2,500,000 (no one officer received more than $1,000,000 compensation). 5. This amount is the portion of incentive stock option compensation that was expensed during the year (recipients are officers). 6. XYZ actually wrote off $27,000 of its accounts receivable as uncollectible. 7. Tax depreciation was $1,900,000. 8. In the current year, XYZ did not make any actual payments on warranties it provided to customers. 9. XYZ made $500,000 of cash contributions to qualified charities during the year. 10. On July 1 of this year XYZ acquired the assets of another business. In the process it acquired $300,000 of goodwill. At the end of the year, XYZ wrote off $30,000 of the goodwill as impaired. 11. XYZ expensed all of its organizational expenditures for book purposes. XYZ expensed the maximum amount of At the end of the year, XYZ wrote off $30,000 of the goodwill as impaired. 11. XYZ expensed all of its organizational expenditures for book purposes. XYZ expensed the maximum amount of organizational expenditures allowed for tax purposes. 12. The other expenses do not contain any items with book-tax differences. 13. This is an estimated tax provision (federal tax expense) for the year. Assume that XYZ is not subject to state income taxes. Estimated tax information: XYZ made four equal estimated tax payments totaling $480,000. For purposes of estimated tax liabilities, assume XYZ reported a tax liability of $800,000 in 2018. During 2019, XYZ determined its taxable income at the end of each of the four quarters as follows: Cumulative taxable income (loss) $ Quarter-end First 350,000 Second Third $ 00, 000 $1,000,000 Finally, assume that XYZ is not a large corporation for purposes of estimated tax calculations. (Do not round intermediate calculations. Round your answers to the nearest dollar amount.) a. Compute XYZ's taxable income. Taxable income b. Compute XYZ's income tax liability. Tax liability c. Complete XYZ's Schedule M-1. (Enter all amounts as positive numbers.) Schedule M1 Schedule M1 Schedule M-1 Reconciliation of Income (Loss) per Books With Income per Return Note: The corporation may be required to file Schedule M-3. See instructions. 1 Net income (loss) per books 7 Income recorded on books this year not 2 Federal income tax per books included on this return (itemize): 3 Excess of capital losses over capital gains Tax-exempt interest 4 Income subject to tax not recorded on books this year (itemize): 8 Deductions on this return not charged 5 Expenses recorded on books this year not deducted on this return (itemize): against book income this year (itemize): a Depreciation a Depreciation b Charitable contributions b Charitable contributions c Travel and entertainment c Other (itemize): Other (itemize): 9 Add lines 7 and 8 6 Add lines 1 through 5 10 Income (page 1, line 28)-line 6 less line 9 THIS FORM IS A SIMULATION OF AN OFFICIAL U.S. TAX FORM. IT IS NOT THE OFFICIAL FORM ITSELF. DO NOT USE THIS FORM FOR TAX FILINGS OR FOR ANY PURPOSE OTHER THAN EDUCATIONAL. 2019 McGraw-Hill Education. d. Complete XYZ's Form 1120, page 1 (Input all the values as positive numbers. Use 2019 tax rules regardless of year on tax form.) 1120 PG 1 Page 1 of Form 1120. Form 1120 U.S. Corporation Income Tax Return OMB No. 1545-0123 Department of the Treasury For calendar year 2018 or tax year beginning 2018, ending ,20 2018 Internal Revenue Service Go to www.irs.gov/Form1120 for instructions and the latest information A Check if: B Employer identification number Name 1a Consolidated return (attach Form 851) b Life/nonlife consolidated retum OR Number, street, and room or suite no. If a P.O. box, see instructions. C Date incorporated (mm/dd/yy) | 2 Personal holding co. (attach Sch. PH) PRINT 3 Personal service corp. (see instructions) City, state, or province, country and ZIP or foreign postal code D Total assets (see instructions) 4 Schedule M-3 attached E Check if: (1) Initial return |(2) Final return O (3) Name change (4) Address change 1a Gross receipts or sales 1a b Returns and allowances 1b c Balance. Subtract line 1b from line 1a 1c 2 Cost of goods sold (attach Form 1125-A) 3 Gross profit. Subtract line 2 from line 1c 4 Dividends and inclusions (Schedule C, line 23, column (a)) 3 4 Income 5 Intereet deductions.) 24 Employee benefit programs 24 25 Reserved for future use 26 Other deductions (attach statement) 27 Total deductions. Add lines 12 through 26 28 Taxable income before net operating loss deduction and special deductions. Subtract line 27 from line 11 29a Net operating loss deduction (see instructions) b Special deductions (Schedule C, line 24, column (c) c Add lines 29a and 29b 30 Taxable income. Subtract line 29c from line 28. see instructions 25 26 27 28 29a 29b 29c 30 31 Total tax (Schedule J, Part I, line 11) 31 32 2018 net 965 tax liability paid (Schedule J, Part II, line 12) 33 Total payments, credits, and section 965 net tax liability (Schedule J, Part III, line 23) , 32 33 Refundable 34 Estimated tax penalty. See instructions. Check if Form 2220 is attached 34 Credits, and 35 Amount owed. If line 33 is smalier than the total of lines 31, 32, and 34, enter amount owed 35 Payments 36 Overpayment. If line 33 is larger than the total of lines 31, 32, and 34, enter amount overpaid 36 37 37 Enter amount from line 36 you want: Credited to 2019 estimated tax Under penalties of perjury, I declare that I have examined this retum, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge. Refunded May the IRS discuss this return with the preparer shown below? See instructions. Sign Here Signature of officer Date Title Yes No Print/Type preparer's name Preparer's signature Date PTIN Paid Self-employed? Firm's name Preparer Firm's EIN Use Only Firm's address Phone no. For Paperwork Reduction Act Notice, see separate instructions. Cat. No. 11450Q Form 1120 (2018) THIS FORM IS A SIMULATION OF AN OFFICIAL U.S. TAX FORM. IT IS NOT THE OFFICIAL FORM ITSELF. DO NOT USE THIS FORM FOR ---- -- - ----- -- ---------- ------ ------ --..-------- ----- -- -. - e. Determine the quarters for which XYZ is subject to underpayment of estimated tax penalties. (1) Required cumulative (3) Required payment based on current year tax liability (2) Estimated tax payment under (4) Required cumulative (5) Actual payments Underpayment penalty Installment payment (per quarter) under prior annualized method year tax method payment 1st quarter 2nd quarter 3rd quarter 4th quarter EXHIBIT 16-6 Stock Ownership and Dividends Received Deduction Percentage Receiving Corporation's Dividends Stock Ownership in Received Distributing Corporation's Deduction Stock Percentage Less than 20 percent 50% At least 20 percent but less than 65 80 percent 80 percent or more22 100

Step by Step Solution

3.41 Rating (157 Votes )

There are 3 Steps involved in it

Description Book Income Dr Cr Booktax adjustments Taxable Income Dr Cr Dr Cr Revenue from sales 40000000 40000000 Cost of Goods Sold 27000000 27000000 Gross profit 13000000 13000000 Other income Incom... View full answer

Get step-by-step solutions from verified subject matter experts