Answered step by step

Verified Expert Solution

Question

1 Approved Answer

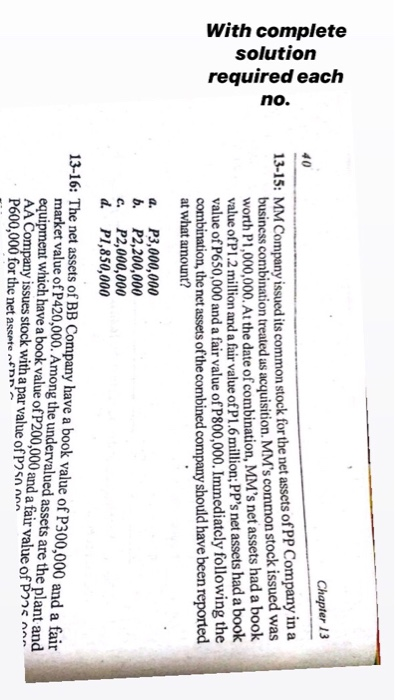

With complete solution required each no. 40 Chapter 13 13-15: MM Company issued its common stock for the net assets of PP Company in a

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cost Accounting For Managerial Planning Decision Making And Control

Authors: Andrew Schiff, Hsihui Chang, Woody M Liao, James L Boockholdt

5th Edition

0759340412, 978-0759340411