write the adjusting entries for each transcation

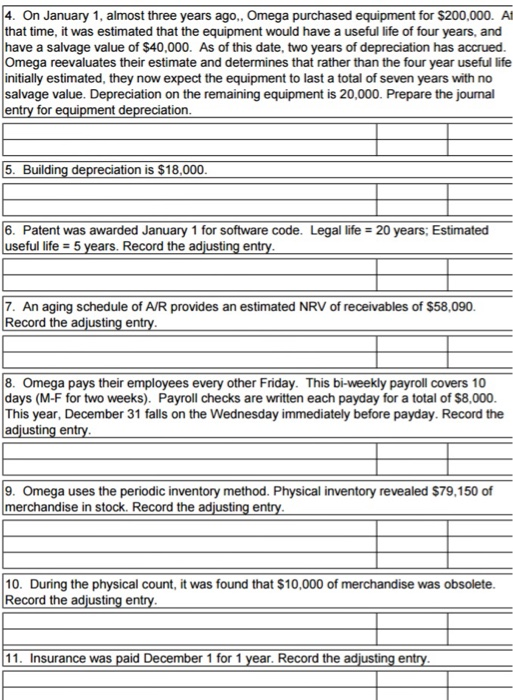

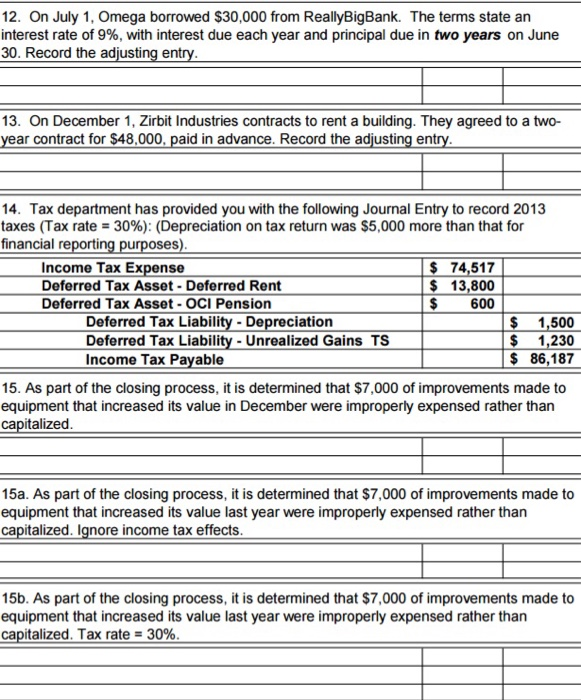

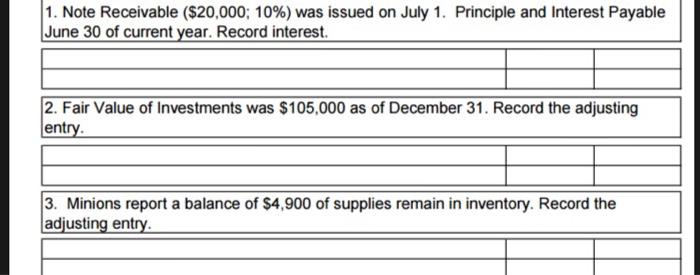

1. Note Receivable ($20,000; 10%) was issued on July 1. Principle and Interest Payable June 30 of current year. Record interest 2. Fair Value of Investments was $105,000 as of December 31. Record the adjusting entry. 3. Minions report a balance of $4,900 of supplies remain in inventory. Record the adjusting entry 4. On January 1, almost three years ago, Omega purchased equipment for $200,000. AI that time, it was estimated that the equipment would have a useful life of four years, and have a salvage value of $40,000. As of this date, two years of depreciation has accrued. Omega reevaluates their estimate and determines that rather than the four year useful life initially estimated, they now expect the equipment to last a total of seven years with no salvage value. Depreciation on the remaining equipment is 20,000. Prepare the journal entry for equipment depreciation. 5. Building depreciation is $18,000. 6. Patent was awarded January 1 for software code. Legal life = 20 years, Estimated useful life = 5 years. Record the adjusting entry 7. An aging schedule of A/R provides an estimated NRV of receivables of $58,090 Record the adjusting entry. 18. Omega pays their employees every other Friday. This bi-weekly payroll covers 10 days (M-F for two weeks). Payroll checks are written each payday for a total of $8,000. This year, December 31 falls on the Wednesday immediately before payday. Record the adjusting entry 9. Omega uses the periodic inventory method. Physical inventory revealed $79,150 of merchandise in stock. Record the adjusting entry. 10. During the physical count, it was found that $10,000 of merchandise was obsolete. Record the adjusting entry. 11. Insurance was paid December 1 for 1 year. Record the adjusting entry. 12. On July 1, Omega borrowed $30,000 from ReallyBigBank. The terms state an interest rate of 9%, with interest due each year and principal due in two years on June 30. Record the adjusting entry. 13. On December 1, Zirbit Industries contracts to rent a building. They agreed to a two- year contract for $48,000. paid in advance. Record the adjusting entry. 14. Tax department has provided you with the following Journal Entry to record 2013 taxes (Tax rate = 30%): (Depreciation on tax return was $5,000 more than that for financial reporting purposes). Income Tax Expense $ 74,517 Deferred Tax Asset - Deferred Rent $ 13,800 Deferred Tax Asset - OCI Pension $ 600 Deferred Tax Liability - Depreciation $ 1,500 Deferred Tax Liability - Unrealized Gains TS $ 1,230 Income Tax Payable $ 86,187 15. As part of the closing process, it is determined that $7,000 of improvements made to equipment that increased its value in December were improperly expensed rather than capitalized. 15a. As part of the closing process, it is determined that $7,000 of improvements made to equipment that increased its value last year were improperly expensed rather than capitalized. Ignore income tax effects 15b. As part of the closing process, it is determined that $7,000 of improvements made to equipment that increased its value last year were improperly expensed rather than capitalized. Tax rate = 30%. 1. Note Receivable ($20,000; 10%) was issued on July 1. Principle and Interest Payable June 30 of current year. Record interest 2. Fair Value of Investments was $105,000 as of December 31. Record the adjusting entry. 3. Minions report a balance of $4,900 of supplies remain in inventory. Record the adjusting entry 4. On January 1, almost three years ago, Omega purchased equipment for $200,000. AI that time, it was estimated that the equipment would have a useful life of four years, and have a salvage value of $40,000. As of this date, two years of depreciation has accrued. Omega reevaluates their estimate and determines that rather than the four year useful life initially estimated, they now expect the equipment to last a total of seven years with no salvage value. Depreciation on the remaining equipment is 20,000. Prepare the journal entry for equipment depreciation. 5. Building depreciation is $18,000. 6. Patent was awarded January 1 for software code. Legal life = 20 years, Estimated useful life = 5 years. Record the adjusting entry 7. An aging schedule of A/R provides an estimated NRV of receivables of $58,090 Record the adjusting entry. 18. Omega pays their employees every other Friday. This bi-weekly payroll covers 10 days (M-F for two weeks). Payroll checks are written each payday for a total of $8,000. This year, December 31 falls on the Wednesday immediately before payday. Record the adjusting entry 9. Omega uses the periodic inventory method. Physical inventory revealed $79,150 of merchandise in stock. Record the adjusting entry. 10. During the physical count, it was found that $10,000 of merchandise was obsolete. Record the adjusting entry. 11. Insurance was paid December 1 for 1 year. Record the adjusting entry. 12. On July 1, Omega borrowed $30,000 from ReallyBigBank. The terms state an interest rate of 9%, with interest due each year and principal due in two years on June 30. Record the adjusting entry. 13. On December 1, Zirbit Industries contracts to rent a building. They agreed to a two- year contract for $48,000. paid in advance. Record the adjusting entry. 14. Tax department has provided you with the following Journal Entry to record 2013 taxes (Tax rate = 30%): (Depreciation on tax return was $5,000 more than that for financial reporting purposes). Income Tax Expense $ 74,517 Deferred Tax Asset - Deferred Rent $ 13,800 Deferred Tax Asset - OCI Pension $ 600 Deferred Tax Liability - Depreciation $ 1,500 Deferred Tax Liability - Unrealized Gains TS $ 1,230 Income Tax Payable $ 86,187 15. As part of the closing process, it is determined that $7,000 of improvements made to equipment that increased its value in December were improperly expensed rather than capitalized. 15a. As part of the closing process, it is determined that $7,000 of improvements made to equipment that increased its value last year were improperly expensed rather than capitalized. Ignore income tax effects 15b. As part of the closing process, it is determined that $7,000 of improvements made to equipment that increased its value last year were improperly expensed rather than capitalized. Tax rate = 30%