Answered step by step

Verified Expert Solution

Question

1 Approved Answer

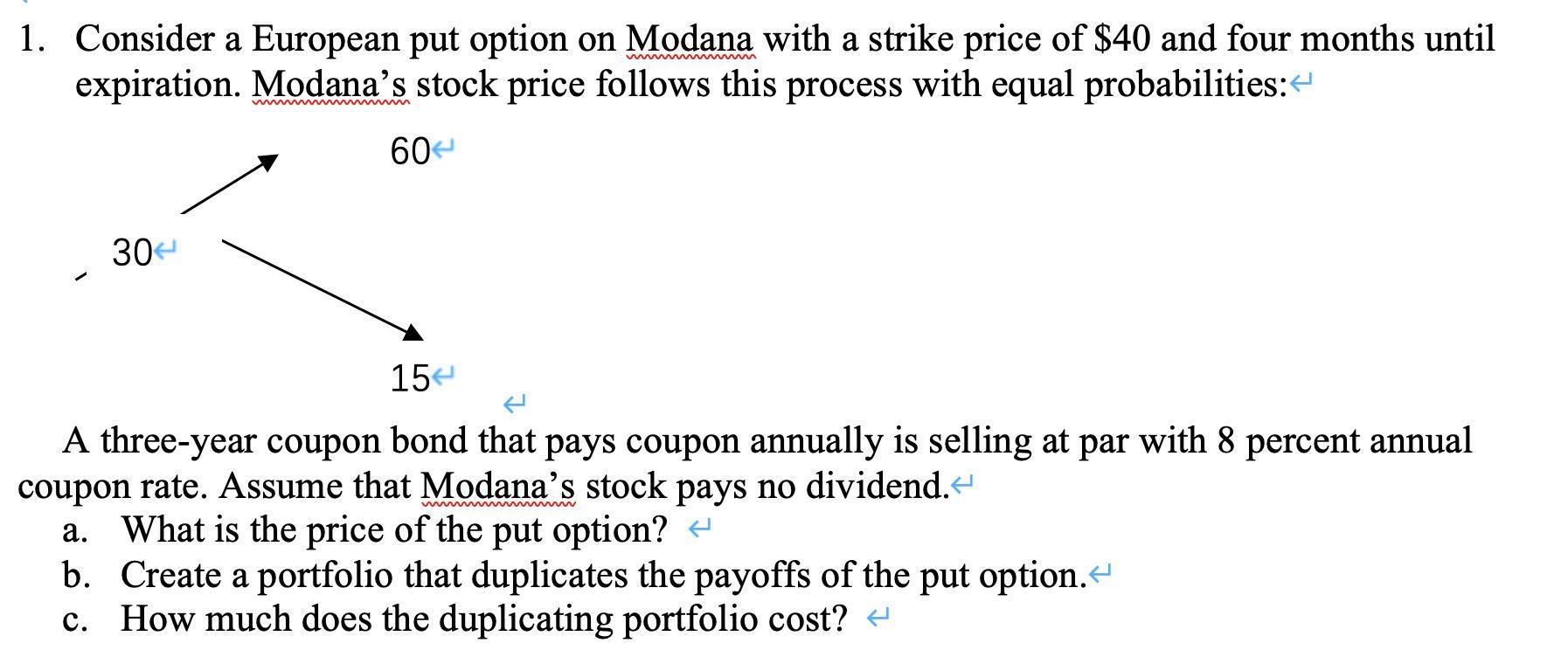

wwwwwwwwwwww 1. Consider a European put option on Modana with a strike price of $40 and four months until expiration. Modana's stock price follows

wwwwwwwwwwww 1. Consider a European put option on Modana with a strike price of $40 and four months until expiration. Modana's stock price follows this process with equal probabilities: < 60 30 15 A three-year coupon bond that pays coupon annually is selling at par with 8 percent annual coupon rate. Assume that Modana's stock pays no dividend. < a. What is the price of the put option? b. Create a portfolio that duplicates the payoffs of the put option. < c. How much does the duplicating portfolio cost?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Essentials Of Business Analytics

Authors: Jeffrey Camm, James Cochran, Michael Fry, Jeffrey Ohlmann, David Anderson, Dennis Sweeney, Thomas Williams

1st Edition

128518727X, 978-1337360135, 978-1285187273