Answered step by step

Verified Expert Solution

Question

1 Approved Answer

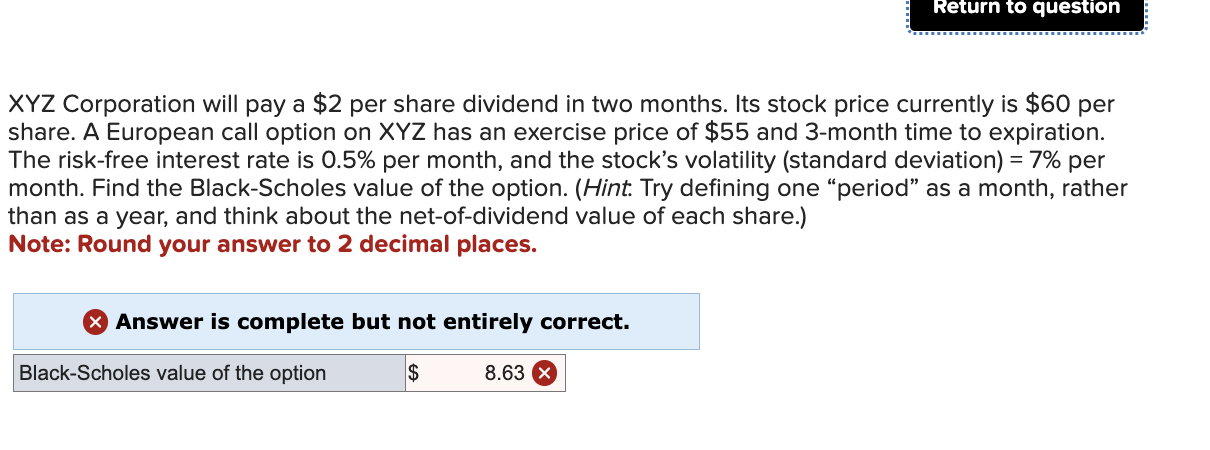

XYZ Corporation will pay a $ 2 per share dividend in two months. Its stock price currently is $ 6 0 per share. A European

XYZ Corporation will pay a $ per share dividend in two months. Its stock price currently is $ per

share. A European call option on XYZ has an exercise price of $ and month time to expiration.

The riskfree interest rate is per month, and the stock's volatility standard deviation per

month. Find the BlackScholes value of the option. Hint Try defining one "period" as a month, rather

than as a year, and think about the netofdividend value of each share.

Note: Round your answer to decimal places.

Answer is complete but not entirely correct.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

How Finance Works

Authors: Mihir Desai

1st Edition

1633696707, 978-1633696709