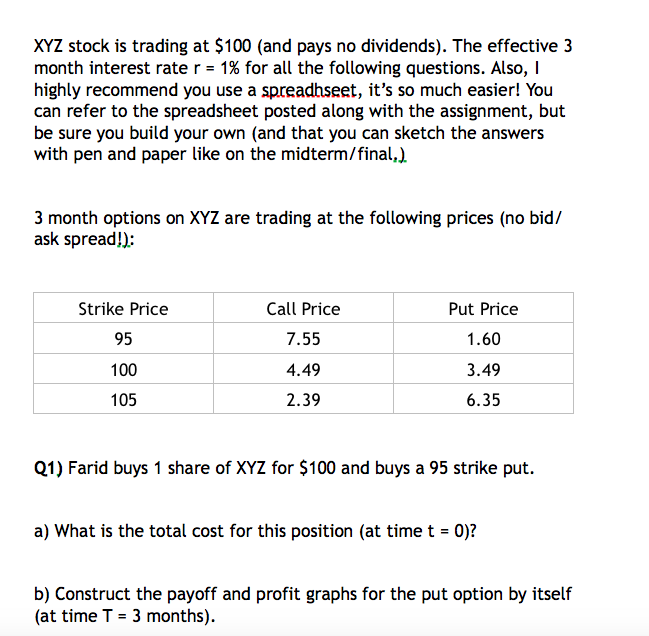

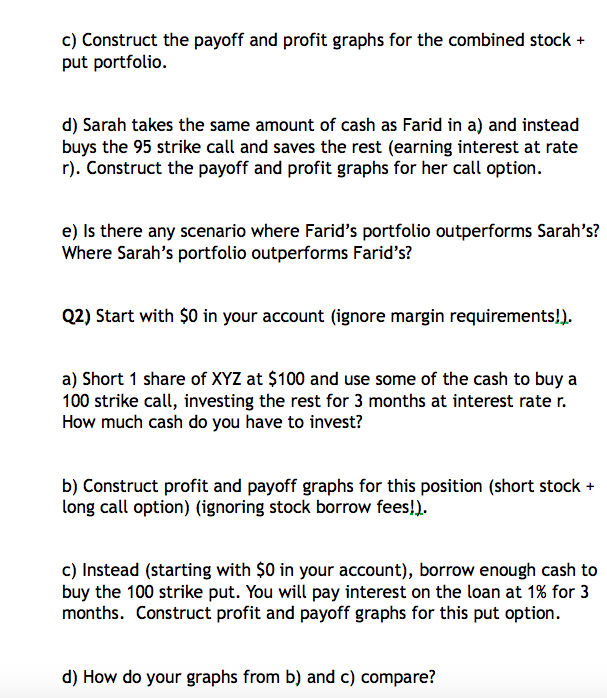

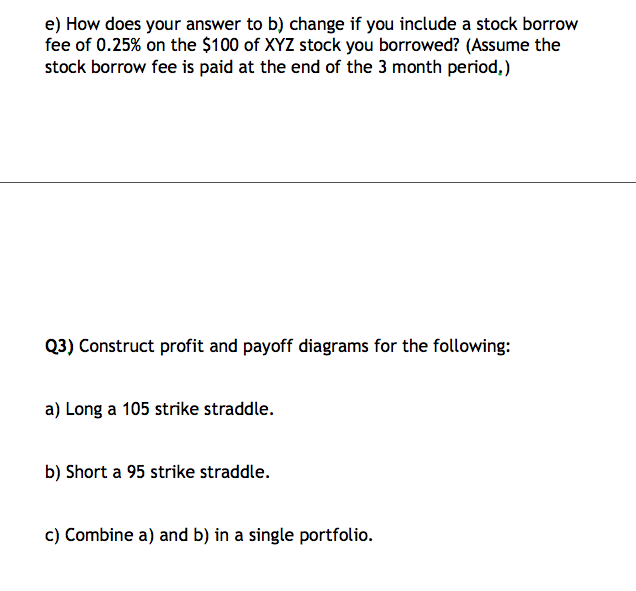

XYZ stock is trading at $100 (and pays no dividends). The effective 3 month interest rate r = 1% for all the following questions. Also, I highly recommend you use a spreadhseet, it's so much easier! You can refer to the spreadsheet posted along with the assignment, but be sure you build your own (and that you can sketch the answers with pen and paper like on the midterm/final,). 3 month options on XYZ are trading at the following prices (no bid/ ask spread!): Strike Price 95 Call Price 7.55 4.49 2.39 Put Price 1.60 3.49 6.35 100 105 Q1) Farid buys 1 share of XYZ for $100 and buys a 95 strike put. a) What is the total cost for this position (at time t = 0)? b) Construct the payoff and profit graphs for the put option by itself (at time T = 3 months). c) Construct the payoff and profit graphs for the combined stock + put portfolio. d) Sarah takes the same amount of cash as Farid in a) and instead buys the 95 strike call and saves the rest (earning interest at rate r). Construct the payoff and profit graphs for her call option. e) Is there any scenario where Farid's portfolio outperforms Sarah's? Where Sarah's portfolio outperforms Farid's? Q2) Start with $0 in your account (ignore margin requirements!). a) Short 1 share of XYZ at $100 and use some of the cash to buy a 100 strike call, investing the rest for 3 months at interest rater. How much cash do you have to invest? b) Construct profit and payoff graphs for this position (short stock + long call option) (ignoring stock borrow fees!).. c) Instead (starting with $0 in your account), borrow enough cash to buy the 100 strike put. You will pay interest on the loan at 1% for 3 months. Construct profit and payoff graphs for this put option. d) How do your graphs from b) and c) compare? e) How does your answer to b) change if you include a stock borrow fee of 0.25% on the $100 of XYZ stock you borrowed? (Assume the stock borrow fee is paid at the end of the 3 month period,) Q3) Construct profit and payoff diagrams for the following: a) Long a 105 strike straddle. b) Short a 95 strike straddle. c) Combine a) and b) in a single portfolio. XYZ stock is trading at $100 (and pays no dividends). The effective 3 month interest rate r = 1% for all the following questions. Also, I highly recommend you use a spreadhseet, it's so much easier! You can refer to the spreadsheet posted along with the assignment, but be sure you build your own (and that you can sketch the answers with pen and paper like on the midterm/final,). 3 month options on XYZ are trading at the following prices (no bid/ ask spread!): Strike Price 95 Call Price 7.55 4.49 2.39 Put Price 1.60 3.49 6.35 100 105 Q1) Farid buys 1 share of XYZ for $100 and buys a 95 strike put. a) What is the total cost for this position (at time t = 0)? b) Construct the payoff and profit graphs for the put option by itself (at time T = 3 months). c) Construct the payoff and profit graphs for the combined stock + put portfolio. d) Sarah takes the same amount of cash as Farid in a) and instead buys the 95 strike call and saves the rest (earning interest at rate r). Construct the payoff and profit graphs for her call option. e) Is there any scenario where Farid's portfolio outperforms Sarah's? Where Sarah's portfolio outperforms Farid's? Q2) Start with $0 in your account (ignore margin requirements!). a) Short 1 share of XYZ at $100 and use some of the cash to buy a 100 strike call, investing the rest for 3 months at interest rater. How much cash do you have to invest? b) Construct profit and payoff graphs for this position (short stock + long call option) (ignoring stock borrow fees!).. c) Instead (starting with $0 in your account), borrow enough cash to buy the 100 strike put. You will pay interest on the loan at 1% for 3 months. Construct profit and payoff graphs for this put option. d) How do your graphs from b) and c) compare? e) How does your answer to b) change if you include a stock borrow fee of 0.25% on the $100 of XYZ stock you borrowed? (Assume the stock borrow fee is paid at the end of the 3 month period,) Q3) Construct profit and payoff diagrams for the following: a) Long a 105 strike straddle. b) Short a 95 strike straddle. c) Combine a) and b) in a single portfolio