Answered step by step

Verified Expert Solution

Question

1 Approved Answer

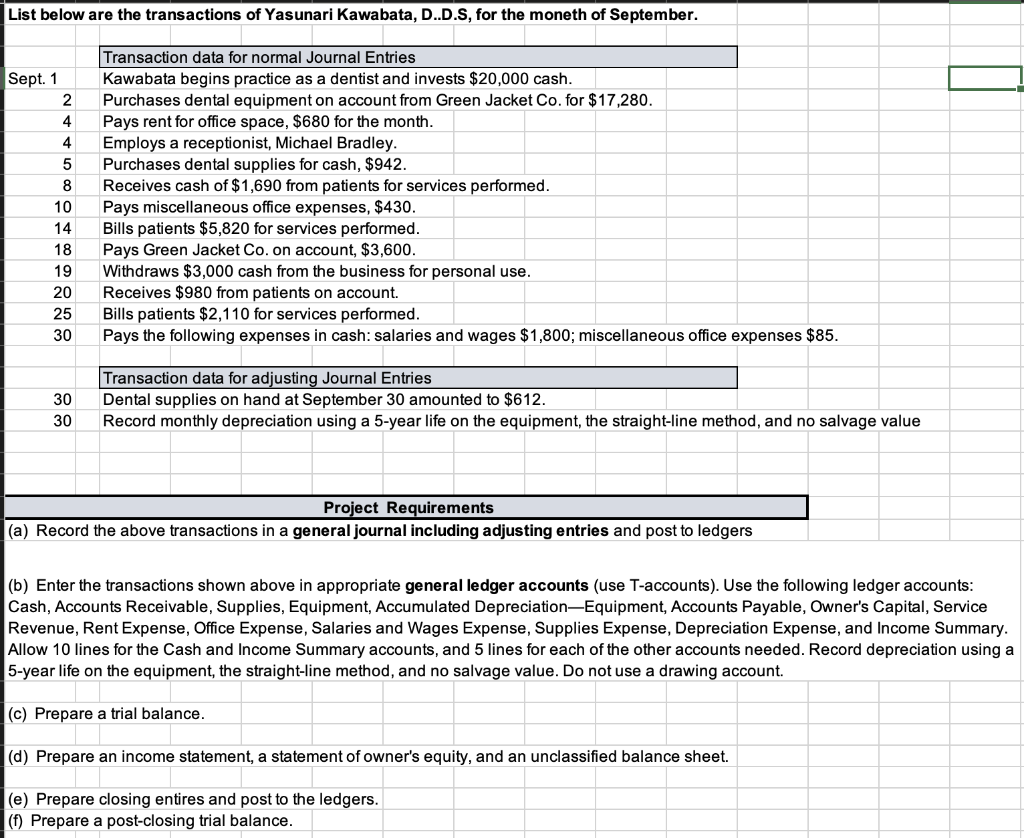

ye ye List below are the transactions of Yasunari Kawabata, D..D.S, for the moneth of September. Sept. 1 2 4 4 5 8 10 14

List below are the transactions of Yasunari Kawabata, D..D.S, for the moneth of September. Sept. 1 2 4 4 5 8 10 14 18 19 20 25 30 30 30 Transaction data for normal Journal Entries Kawabata begins practice as a dentist and invests $20,000 cash. Purchases dental equipment on account from Green Jacket Co. for $17,280. Pays rent for office space, $680 for the month. Employs a receptionist, Michael Bradley. Purchases dental supplies for cash, $942. Receives cash of $1 ,690 from patients for services erformed. Pays miscellaneous office expenses, $430. Bills patients $5,820 for services performed. Pays Green Jacket co. on account, $3,600. Withdraws $3,000 cash from the business for personal use. Receives $980 from patients on account. Bills patients $2,110 for services performed. Pays the following expenses in cash: salaries and wages $1 ,800; miscellaneous office expenses $85. Transaction data for ad'ustin Journal Entries Dental supplies on hand at September 30 amounted to $612. Record monthly depreciation using a 5-year life on the equipment, the straight-line method, and no salvage value Proect Re uirements (a) Record the above transactions in a general journal including adjusting entries and postto ledgers (b) Enter the transactions shown above in appropriate general ledger accounts (use T-accounts). Use the following ledger accounts: Cash, Accounts Receivable, Supplies, Equipment, Accumulated DepreciationEquipment, Accounts Payable, Owner's Capital, Service Revenue, Rent Expense, Offce Expense, Salaries and Wages Expense, Supplies Expense, Depreciation Expense, and Income Summary. Allow 1 0 lines for the Cash and Income Summary accounts, and 5 lines for each of the other accounts needed. Record depreciation using a 5-year life on the equipment, the straight-line method, and no salvage value. DO not use a drawing account. (c) Prepare a trial balance. (d) Prepare an income statement, a statement of owner's equity, and an unclassified balance sheet. (e) Prepare closing entires and postto the ledgers. (f) Prepare a post-closing trial balance.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Management Accounting For Business

Authors: Colin Drury, Mike Tayles

8th Edition

1473778808, 978-1473778801