Answered step by step

Verified Expert Solution

Question

1 Approved Answer

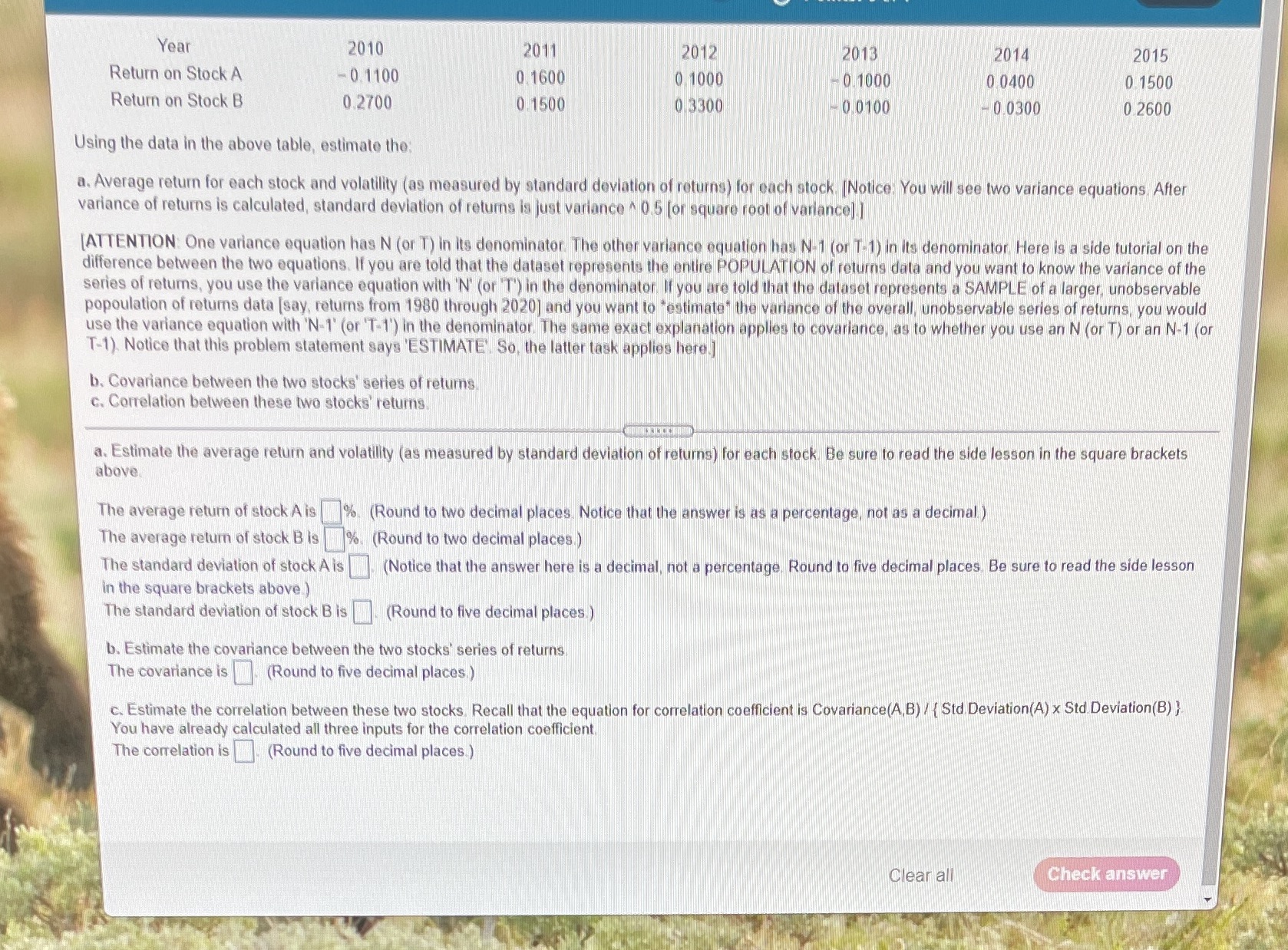

Year 2010 2011 2012 2013 2014 2015 Return on Stock A Return on Stock B -0.1100 0.1600 0.1000 0.1000 0.0400 0.1500 0.2700 0.1500 0.3300

Year 2010 2011 2012 2013 2014 2015 Return on Stock A Return on Stock B -0.1100 0.1600 0.1000 0.1000 0.0400 0.1500 0.2700 0.1500 0.3300 -0.0100 -0.0300 0.2600 Using the data in the above table, estimate the: a. Average return for each stock and volatility (as measured by standard deviation of returns) for each stock. [Notice: You will see two variance equations. After variance of returns is calculated, standard deviation of returns is just variance 0.5 [or square root of variance]] [ATTENTION: One variance equation has N (or T) in its denominator. The other variance equation has N-1 (or T-1) in its denominator Here is a side tutorial on the difference between the two equations. If you are told that the dataset represents the entire POPULATION of returns data and you want to know the variance of the series of returns, you use the variance equation with 'N' (or 'T') in the denominator. If you are told that the dataset represents a SAMPLE of a larger, unobservable popoulation of returns data [say, returns from 1980 through 2020] and you want to "estimate" the variance of the overall, unobservable series of returns, you would use the variance equation with 'N-1' (or 'T-1') in the denominator. The same exact explanation applies to covariance, as to whether you use an N (or T) or an N-1 (or T-1). Notice that this problem statement says 'ESTIMATE. So, the latter task applies here.] b. Covariance between the two stocks' series of returns. c. Correlation between these two stocks' returns. a. Estimate the average return and volatility (as measured by standard deviation of returns) for each stock. Be sure to read the side lesson in the square brackets above. The average return of stock A is The average return of stock B is The standard deviation of stock A is in the square brackets above.) The standard deviation of stock B is % %. (Round to two decimal places. Notice that the answer is as a percentage, not as a decimal) (Round to two decimal places.) (Notice that the answer here is a decimal, not a percentage. Round to five decimal places. Be sure to read the side lesson (Round to five decimal places.) b. Estimate the covariance between the two stocks' series of returns The covariance is (Round to five decimal places.) c. Estimate the correlation between these two stocks. Recall that the equation for correlation coefficient is Covariance(A,B)/ { Std Deviation(A) x Std Deviation(B)} You have already calculated all three inputs for the correlation coefficient. The correlation is (Round to five decimal places.) Clear all Check answer

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Financial Management

Authors: James R Mcguigan, R Charles Moyer, William J Kretlow

10th Edition

978-0324289114, 0324289111