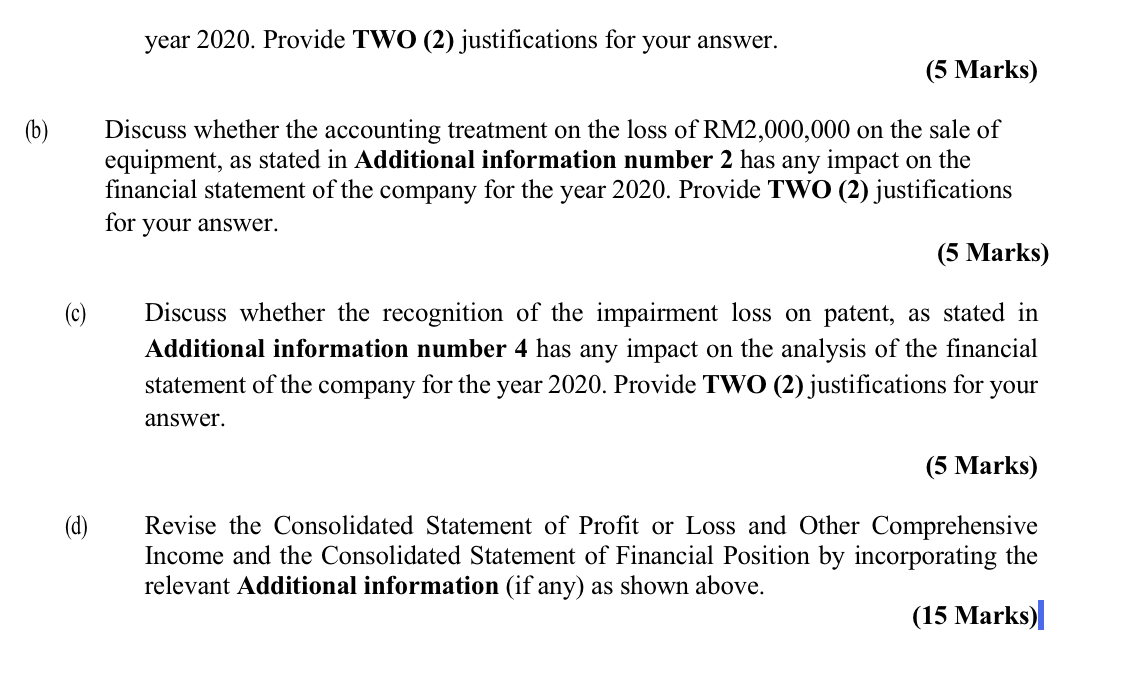

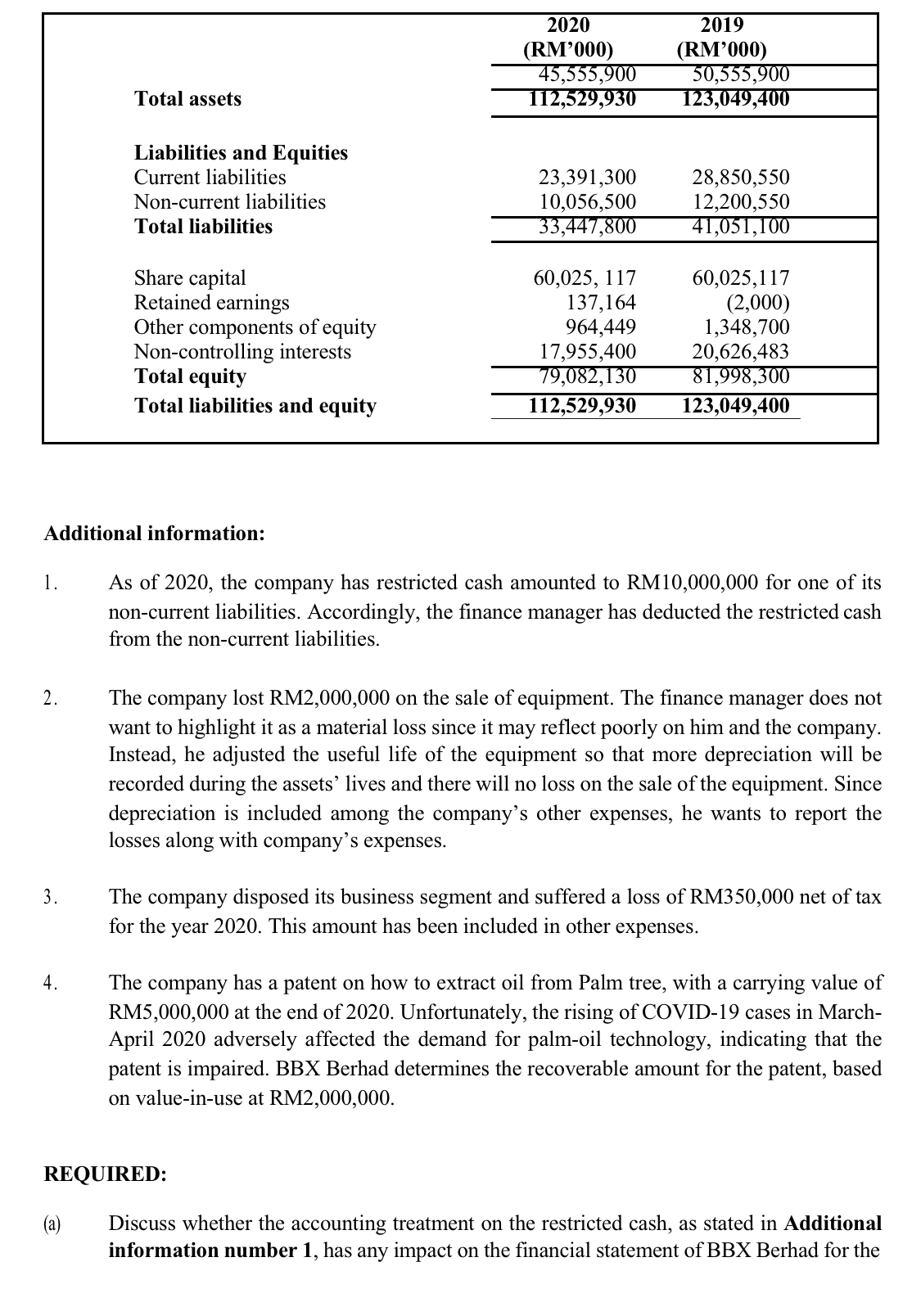

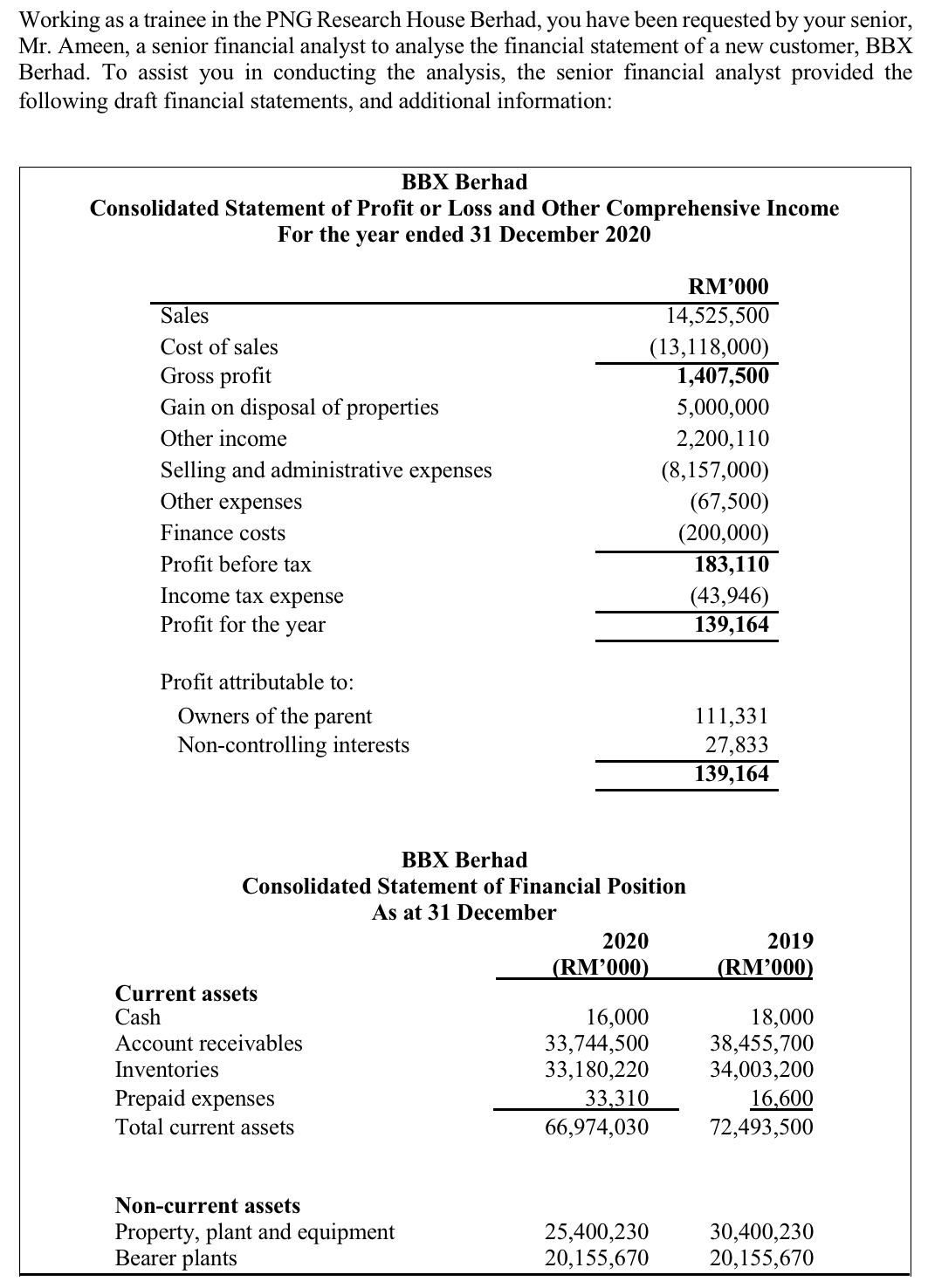

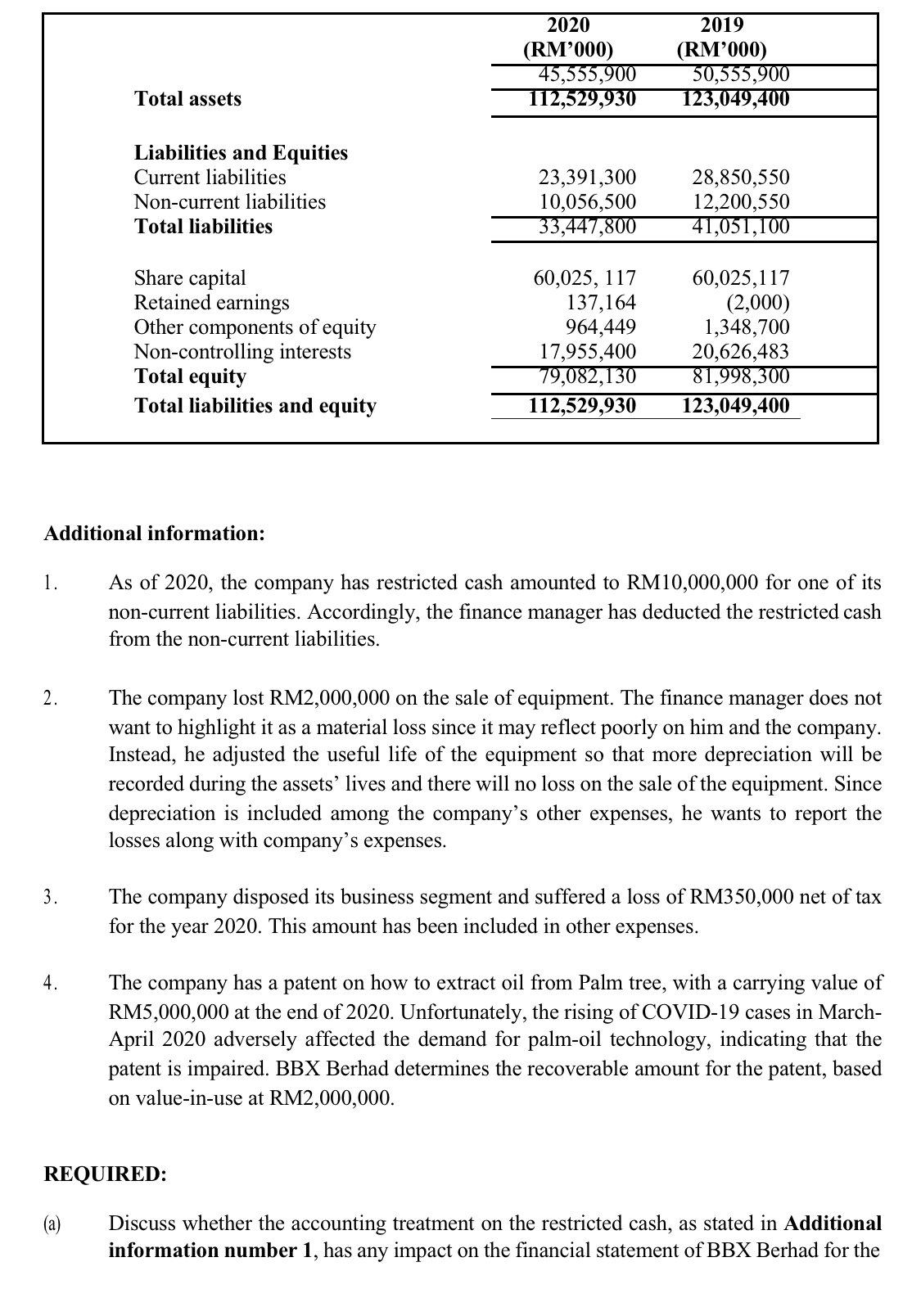

year 2020. Provide TWO (2) justifications for your answer. (5 Marks) (b) Discuss whether the accounting treatment on the loss of RM2,000,000 on the sale of equipment, as stated in Additional information number 2 has any impact on the financial statement of the company for the year 2020. Provide TWO (2) justifications for your answer. (5 Marks) (c) Discuss whether the recognition of the impairment loss on patent, as stated in Additional information number 4 has any impact on the analysis of the financial statement of the company for the year 2020. Provide TWO (2) justifications for your answer. (5 Marks) (d) Revise the Consolidated Statement of Profit or Loss and Other Comprehensive Income and the Consolidated Statement of Financial Position by incorporating the relevant Additional information (if any) as shown above. (15 Marks)Total assets Liabilities and Equities Current liabilities Non-current liabilities Total liabilities Share capital Retained earnings Other components of equity Non-controlling interests Total equity Total liabilities and equity 2020 (RM'000) 4 ,0 I I l I 9 5 I 3' 23,391,300 10,056,500 ,' 1 ,. I I 60,025, 117 137,164 964,449 17,955,400 -,u: , I 112,529,930 2019 (RM'000) I, ,1 l I all 51" 28,850,550 12,200,550 1 l I l 5 S 60,025,1 17 (2,000) 1,348,700 20,626,483 :,':,11 123,049,400 Additional information: 1. As of 2020, the company has restricted cash amounted to RM10,000,000 for one of its non-current liabilities. Accordingly, the nance manager has deducted the restricted cash from the non-current liabilities. 2. The company lost RM2,000,000 on the sale of equipment. The nance manager does not want to highlight it as a material loss since it may reect poorly on him and the company. Instead, he adjusted the useful life of the equipment so that more depreciation will be recorded during the assets' lives and there will no loss on the sale of the equipment. Since depreciation is included among the company's other expenses, he wants to report the losses along with company's expenses. 3. The company disposed its business segment and suffered a loss of RM350,000 net of tax for the year 2020. This amount has been included in other expenses. 4. The company has a patent on how to extract oil from Palm tree, with a carrying value of RM5,000,000 at the end of 2020. Unfortunately, the rising of COVID19 cases in March- April 2020 adversely affected the demand for palmoil technology, indicating that the patent is impaired. BBX Berhad determines the recoverable amount for the patent, based on value-in-use at RM2,000,000. REQUIRED: (21) Discuss whether the accounting treatment on the restricted cash, as stated in Additional information number 1 , has any impact on the fmancial statement of BBX Berhad for the Working as a trainee in the PNG Research House Berhad, you have been requested by your senior, Mr. Ameen, a senior financial analyst to analyse the financial statement of a new customer, BBX Berhad. To assist you in conducting the analysis, the senior financial analyst provided the following draft financial statements, and additional information: BBX Berhad Consolidated Statement of Profit or Loss and Other Comprehensive Income For the year ended 31 December 2020 RM'000 Sales 14,525,500 Cost of sales (13,118,000) Gross profit 1,407,500 Gain on disposal of properties 5,000,000 Other income 2,200, 110 Selling and administrative expenses (8,157,000) Other expenses (67,500) Finance costs (200,000) Profit before tax 183,110 Income tax expense (43,946) Profit for the year 139,164 Profit attributable to: Owners of the parent 111,331 Non-controlling interests 27,833 139,164 BBX Berhad Consolidated Statement of Financial Position As at 31 December 2020 2019 (RM'000) (RM'000) Current assets Cash 16,000 18,000 Account receivables 33,744,500 38,455,700 Inventories 33,180,220 34,003,200 Prepaid expenses 33,310 16,600 Total current assets 66,974,030 72,493,500 Non-current assets Property, plant and equipment 25,400,230 30,400,230 Bearer plants 20,155,670 20,155,670