Answered step by step

Verified Expert Solution

Question

1 Approved Answer

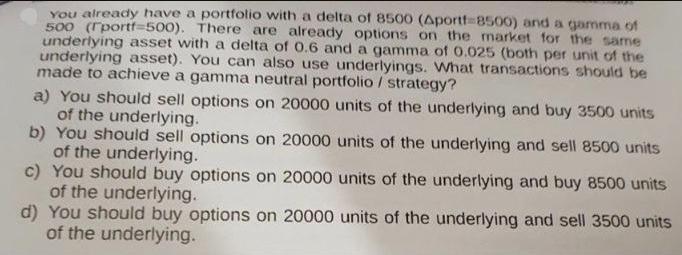

You already have a portfolio with a delta of 8500 (Aportf-8500) and a gamma of 500 (portf-500). There are already options on the market

You already have a portfolio with a delta of 8500 (Aportf-8500) and a gamma of 500 (portf-500). There are already options on the market for the same underlying asset with a delta of 0.6 and a gamma of 0.025 (both per unit of the underlying asset). You can also use underlyings. What transactions should be made to achieve a gamma neutral portfolio / strategy? a) You should sell options on 20000 units of the underlying and buy 3500 units of the underlying. b) You should sell options on 20000 units of the underlying and sell 8500 units of the underlying. c) You should buy options on 20000 units of the underlying and buy 8500 units of the underlying. d) You should buy options on 20000 units of the underlying and sell 3500 units of the underlying.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

The detailed answer for the above question is provided below To achieve a gammaneutral portfoliostra...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Project Management A Systems Approach To Planning Scheduling And Controlling

Authors: Harold Kerzner

13th Edition

1119805376, 978-1119805373