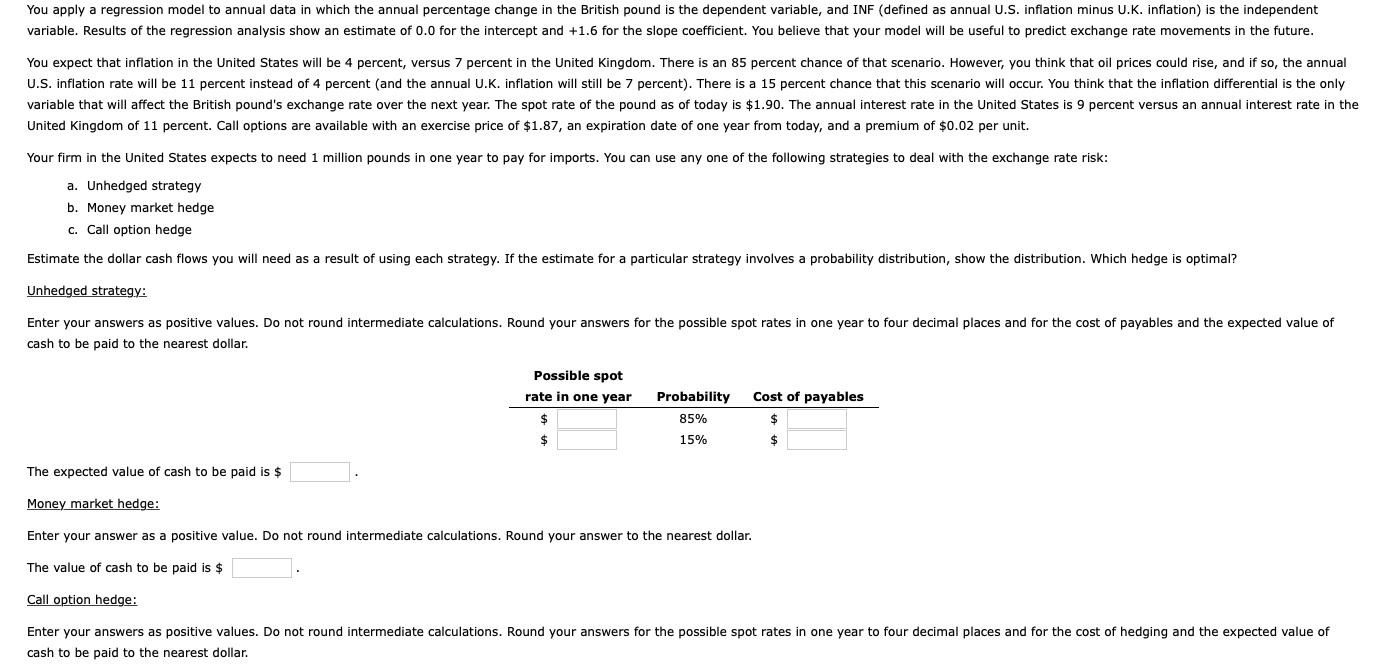

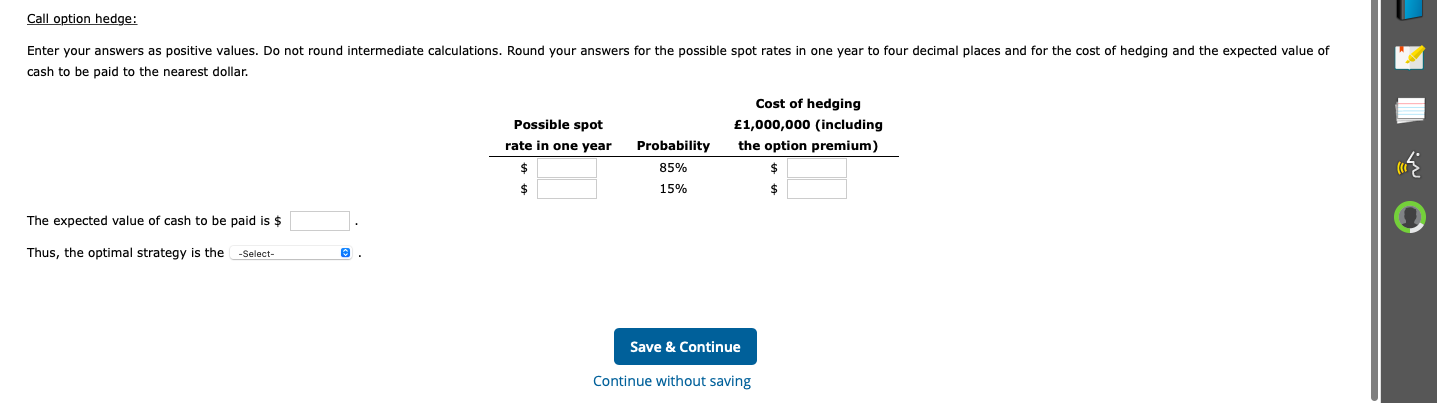

You apply a regression model to annual data in which the annual percentage change in the British pound is the dependent variable, and INF (defined as annual U.S. inflation minus U.K. inflation) is the independent variable. Results of the regression analysis show an estimate of 0.0 for the intercept and +1.6 for the slope coefficient. You believe that your model will be useful to predict exchange rate movements in the future. You expect that inflation in the United States will be 4 percent, versus 7 percent in the United Kingdom. There is an 85 percent chance of that scenario. However, you think that oil prices could rise, and if so, the annual U.S. inflation rate will be 11 percent instead of 4 percent (and the annual U.K. inflation will still be 7 percent). There is a 15 percent chance that this scenario will occur. You think that the inflation differential is the only variable that will affect the British pound's exchange rate over the next year. The spot rate of the pound as of today is $1.90. The annual interest rate in the United States is 9 percent versus an annual interest rate in the United Kingdom of 11 percent. Call options are available with an exercise price of $1.87, an expiration date of one year from today, and a premium of $0.02 per unit. Your firm in the United States expects to need 1 million pounds in one year to pay for imports. You can use any one of the following strategies to deal with the exchange rate risk: a. Unhedged strategy b. Money market hedge c. Call option hedge Estimate the dollar cash flows you will need as a result of using each strategy. If the estimate for a particular strategy involves a probability distribution, show the distribution. Which hedge is optimal? Unhedged strategy: Enter your answers as positive values. Do not round intermediate calculations. Round your answers for the possible spot rates in one year to four decimal places and for the cost of payables and the expected value of cash to be paid to the nearest dollar. Possible spot rate in one year Probability 85% 15% Cost of payables $ $ $ The expected value of cash to be paid is $ Money market hedge: Enter your answer as a positive value. Do not round intermediate calculations. Round your answer to the nearest dollar. The value of cash to be paid is $ Call option hedge: Enter your answers as positive values. Do not round intermediate calculations. Round your answers for the possible spot rates in one year to four decimal places and for the cost of hedging and the expected value of cash to be paid to the nearest dollar. Call option hedge: Enter your answers as positive values. Do not round intermediate calculations. Round your answers for the possible spot rates in one year to four decimal places and for the cost of hedging and the expected value of cash to be paid to the nearest dollar. Possible spot rate in one year Cost of hedging 1,000,000 (including the option premium) Probability 85% 15% $ $ The expected value of cash to be paid is $ Thus, the optimal strategy is the -Select- Save & Continue Continue without saving You apply a regression model to annual data in which the annual percentage change in the British pound is the dependent variable, and INF (defined as annual U.S. inflation minus U.K. inflation) is the independent variable. Results of the regression analysis show an estimate of 0.0 for the intercept and +1.6 for the slope coefficient. You believe that your model will be useful to predict exchange rate movements in the future. You expect that inflation in the United States will be 4 percent, versus 7 percent in the United Kingdom. There is an 85 percent chance of that scenario. However, you think that oil prices could rise, and if so, the annual U.S. inflation rate will be 11 percent instead of 4 percent (and the annual U.K. inflation will still be 7 percent). There is a 15 percent chance that this scenario will occur. You think that the inflation differential is the only variable that will affect the British pound's exchange rate over the next year. The spot rate of the pound as of today is $1.90. The annual interest rate in the United States is 9 percent versus an annual interest rate in the United Kingdom of 11 percent. Call options are available with an exercise price of $1.87, an expiration date of one year from today, and a premium of $0.02 per unit. Your firm in the United States expects to need 1 million pounds in one year to pay for imports. You can use any one of the following strategies to deal with the exchange rate risk: a. Unhedged strategy b. Money market hedge c. Call option hedge Estimate the dollar cash flows you will need as a result of using each strategy. If the estimate for a particular strategy involves a probability distribution, show the distribution. Which hedge is optimal? Unhedged strategy: Enter your answers as positive values. Do not round intermediate calculations. Round your answers for the possible spot rates in one year to four decimal places and for the cost of payables and the expected value of cash to be paid to the nearest dollar. Possible spot rate in one year Probability 85% 15% Cost of payables $ $ $ The expected value of cash to be paid is $ Money market hedge: Enter your answer as a positive value. Do not round intermediate calculations. Round your answer to the nearest dollar. The value of cash to be paid is $ Call option hedge: Enter your answers as positive values. Do not round intermediate calculations. Round your answers for the possible spot rates in one year to four decimal places and for the cost of hedging and the expected value of cash to be paid to the nearest dollar. Call option hedge: Enter your answers as positive values. Do not round intermediate calculations. Round your answers for the possible spot rates in one year to four decimal places and for the cost of hedging and the expected value of cash to be paid to the nearest dollar. Possible spot rate in one year Cost of hedging 1,000,000 (including the option premium) Probability 85% 15% $ $ The expected value of cash to be paid is $ Thus, the optimal strategy is the -Select- Save & Continue Continue without saving