Answered step by step

Verified Expert Solution

Question

1 Approved Answer

You are a fund manager who has been given the following portfolio: Portfolio Delta exposure You have access to the following two options Delta

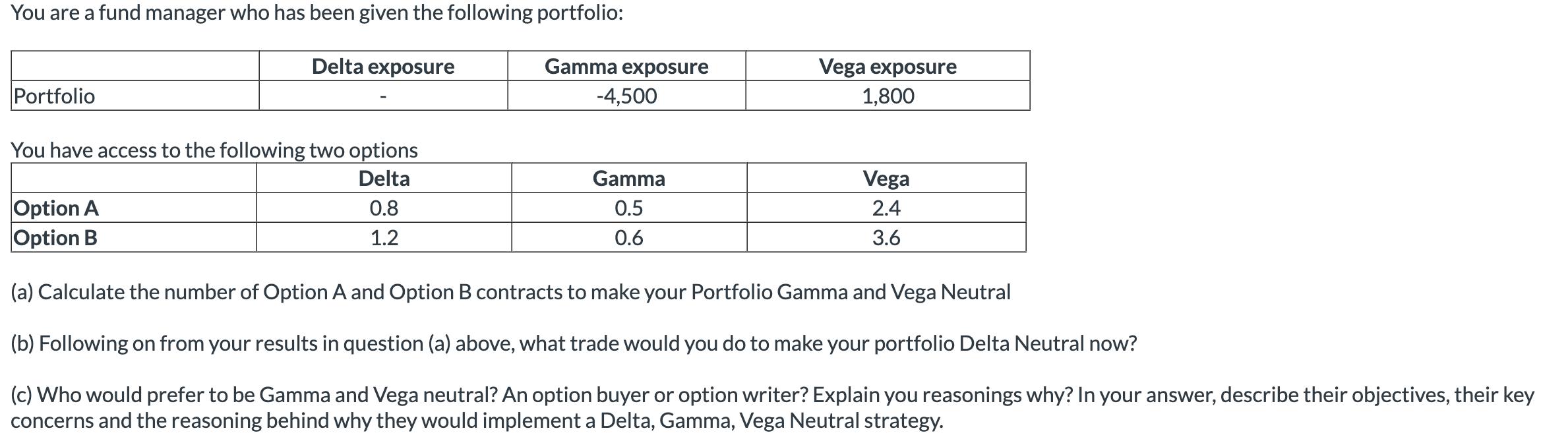

You are a fund manager who has been given the following portfolio: Portfolio Delta exposure You have access to the following two options Delta 0.8 1.2 Option A Option B Gamma exposure -4,500 Gamma 0.5 0.6 Vega exposure 1,800 Vega 2.4 3.6 (a) Calculate the number of Option A and Option B contracts to make your Portfolio Gamma and Vega Neutral (b) Following on from your results in question (a) above, what trade would you do to make your portfolio Delta Neutral now? (c) Who would prefer to be Gamma and Vega neutral? An option buyer or option writer? Explain you reasonings why? In your answer, describe their objectives, their key concerns and the reasoning behind why they would implement a Delta, Gamma, Vega Neutral strategy.

Step by Step Solution

★★★★★

3.55 Rating (159 Votes )

There are 3 Steps involved in it

Step: 1

To calculate the number of Option A and Option B contracts needed to make the portfolio gamma and vega neutral we can use the following formulas Number of Option A contracts Portfolio Gamma Exposure G...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Smith and Roberson Business Law

Authors: Richard A. Mann, Barry S. Roberts

15th Edition

1285141903, 1285141903, 9781285141909, 978-0538473637