Question: You are a senior auditor with Rodriguez & Jones, a small auditing firm located in Canterbury, an eastern suburb of Melbourne, Victoria. Your team has

You are a senior auditor with Rodriguez & Jones, a small auditing firm located in Canterbury, an eastern suburb of Melbourne, Victoria. Your team has been assigned to the audit of a new client, Miller’s Merchandise, for the year ended 30th June 2021. Miller’s Merchandise is a Deepdene-based wholesaler offering for sale everything from baby food and beverages, to snacks and vegetables, and everything in between.

You are planning the audit of accounts payable, where preparatory work has revealed the following:

- Miller’s Merchandise purchases its stock from a list of approved suppliers, with purchase orders processed electronically through a business-to-business ecommerce system. This system uses a fast chain model of supply, with suppliers electronically transmitting their invoices – this automated approach means supplier invoices are credited directly to the accounts payable file of Miller’s Merchandise upon receipt of the purchase order. You are concerned about the impact this might have on the existence assertion.

- A key control to safeguard the Valuation and Allocation assertion, is the use of key entry validation – an IT control whereby the Number of Units Purchased is multiplied by the Unit Cost, and compared with the Total Cost as per the supplier’s invoice.

- As is always the case with accounts payable and purchases, you are have flagged the need to investigate the risk associated with the completeness assertion.

- As Miller’s Merchandise operates both in a B2B and B2C environments, you need to test the security and operation of these systems. You are concerned there may be some overlap, thereby putting the classification assertion at risk.

- The owner of Miller’s Merchandise (Suzie Miller) owns and operates another business, Brazeele Mottley, out of Broadmeadows. To make most use of the combined purchasing power, Suzie combines purchases for both businesses where possible. This makes you concerned the rights and obligation assertion for Miller’s Merchandise’s accounts payable may be at risk.

- Interrogate the 2020/2021 accounts payable data provided, developing visualizations to identify potential issues to follow up during the audit. Specifically you are required to comment on the following assertions ‘at risk’:

- Existence;

- Valuation and Allocation;

- Completeness;

- Classification;

- Rights and Obligations.

For each of the above:

- Explain what the assertion means as it relates to Miller’s Merchandise;

- Present relevant data visualisations for the assertion being investigated;

- Discussion/Interpretation of Findings/Data Visualisations.

- Discuss the most appropriate audit strategy to adopt when auditing the accounts payable for Miller’s Merchandise.

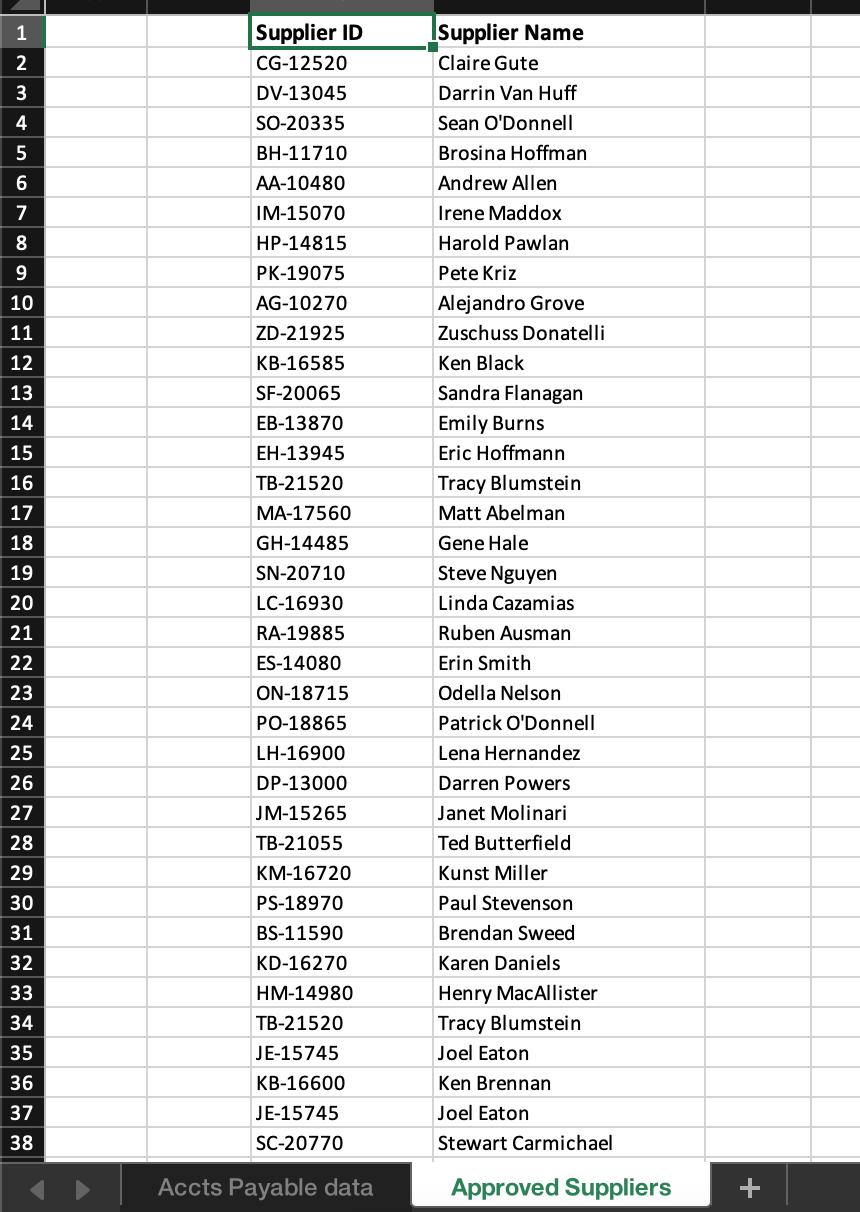

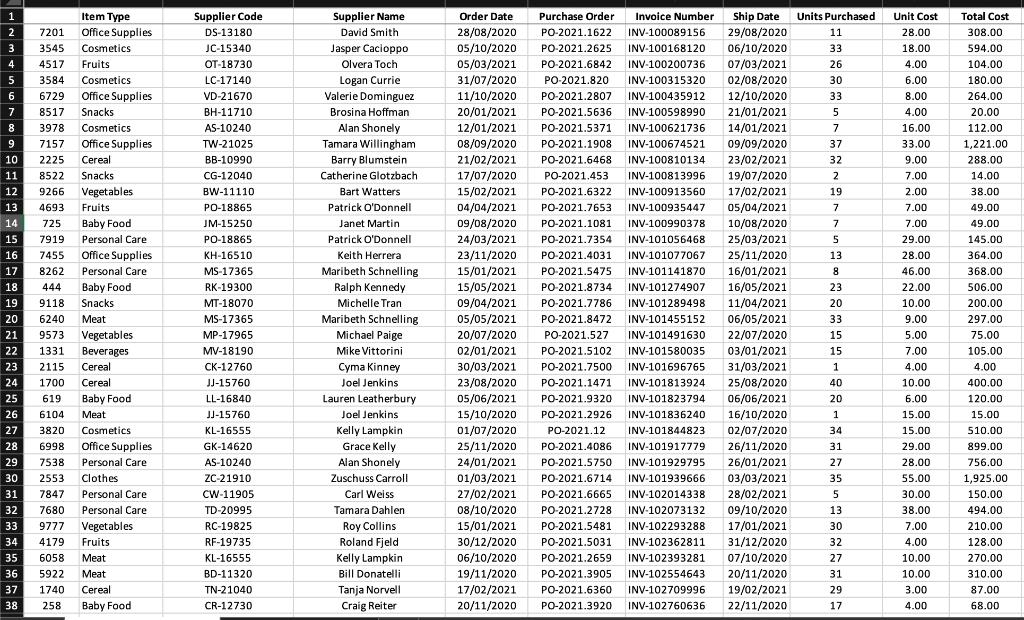

1 23456700 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 Supplier ID CG-12520 DV-13045 SO-20335 BH-11710 AA-10480 IM-15070 HP-14815 PK-19075 AG-10270 ZD-21925 KB-16585 SF-20065 EB-13870 EH-13945 TB-21520 MA-17560 GH-14485 SN-20710 LC-16930 RA-19885 ES-14080 ON-18715 PO-18865 LH-16900 DP-13000 JM-15265 TB-21055 KM-16720 PS-18970 BS-11590 KD-16270 HM-14980 TB-21520 JE-15745 KB-16600 JE-15745 SC-20770 Accts Payable data Supplier Name Claire Gute Darrin Van Huff Sean O'Donnell Brosina Hoffman Andrew Allen Irene Maddox Harold Pawlan Pete Kriz Alejandro Grove Zuschuss Donatelli Ken Black Sandra Flanagan Emily Burns Eric Hoffmann Tracy Blumstein Matt Abelman Gene Hale Steve Nguyen Linda Cazamias Ruben Ausman Erin Smith Odella Nelson Patrick O'Donnell Lena Hernandez Darren Powers Janet Molinari Ted Butterfield Kunst Miller Paul Stevenson Brendan Sweed Karen Daniels Henry MacAllister Tracy Blumstein Joel Eaton Ken Brennan Joel Eaton Stewart Carmichael Approved Suppliers +

Step by Step Solution

3.58 Rating (218 Votes )

There are 3 Steps involved in it

A1 Analysis of Existence Assertion i Explanation of existence assertion as it relates to Millers Merchandise The meaning of the Existence Assertion is that the accounts payable balance that is reporte... View full answer

Get step-by-step solutions from verified subject matter experts