Question

You are an audit senior with the firm of Mike and Kiwi LLP. You were just informed that you will be taking over as the

You are an audit senior with the firm of Mike and Kiwi LLP. You were just informed that you will be taking over as the in charge auditor to a new client for you, Stanley Inc for the year ended December 31, 2021. The previous incharge had to leave the job before the end of the audit to be with his wife who gave birth to their twin boys 6 weeks earlier than expected. The incharge did not have a chance to check the work done by the audit trainees.

Your firm has audited Stanley Inc. for the past 6 years and the management letter each year has revealed several control deficiencies. While your firm has identified several errors in the financial statements in the past, management always agreed to some of the adjustments your firm identified as material and accordingly have always received an unqualified opinion.

The draft audit report is dated March 15, 2022.

Exhibit 1

Description of Stanleys Operations

Stanley Inc. is a privately held company that was founded in 2007 by Andy Summer, who is also Stanleys CEO. In 2007 Andy sold 25% of his company to a group of private investors. The investors receive quarterly dividends that are calculated based upon a combination of sales and net income. The investors, all experienced business-people, serve as Andys board of directors and give him advice on the strategic direction of the company. The Board relies on the external audit to provide them with assurance that their dividends are based on reliable figures.

Stanley buys computers and related equipment in bulk at wholesale prices and resells these items at a markup to a loyal base of corporate customers. While this is a competitive industry, demand is growing and Stanley stands out with its excellent customer service. Andy is very involved in most of the operating decisions. To ensure staff continue to provide excellent customer service and act with integrity, he plans to implement a code of ethics at some point in the future.

Stanley operates five warehouses, each carrying a mix of inventory items. In total there are three main categories of inventory, including:

- computer hardware standard

- computer parts and peripherals and

- computer software.

The first type of inventory, computer hardware, consists of specialized computer hardware, desktop computers, and laptop computers. This inventory is more costly than other types of inventories. While it generates a higher profit margin, new technology is always emerging that customers are asking for. Because the company makes inventory orders months in advance, Stanley occasionally overestimates demand. After three or four months products are usually difficult to sell, but they are kept because most can be returned to the supplier.

The second type of inventory relates to standard computer parts and peripherals, such as monitor and printers. This type of inventory generates a significant portion of Stanleys sales. The third type of inventory is software, ranging from operating systems to business applications (such as financial reporting software).

This year, Stanley implemented an integrated computer system to manage the general ledger as well as inventory, purchases, and sales. The system was developed by external consultants and is maintained by Stanleys IT department. Stanley is confident that this new system will result in more accurate financial information and statements.

To help retain the sales team and motivate and retain senior management, in April 2021 the Board approved a bonus scheme for the sales team and senior management based on sales as an added form of compensation.

On May 30, 2021 Monica Fung was hired as the controller and reported to the CEO. Monica replaced the previous controller who had resigned suddenly in early February 2021 as a result of a dispute he had with the CEO. Monica is a CPA who last worked fulltime in an accounting firm in 2016 where she obtained her accounting designation. Since that time Monica has focussed her efforts on staying at home and raising her children. The CEO knew Monica from his school days at the business school at a Canadian University and decided to hire Monica as the controller as she was looking to start working fulltime again and was available immediately to start work at Stanley Inc.

Monica prepares monthly financial statements for the CEO. She also compares budget versus actual results and highlights all large variances. However, to date the CEO has not followed up with her for any explanations for any large variances between actual and budget.

The amount of damaged inventory has been gradually increasing over the past eight months. Damaged inventory has been piling up in a corner of the warehouse. The CEO suggested holding a liquidation sale to get rid of this inventory to free up space in the warehouse.

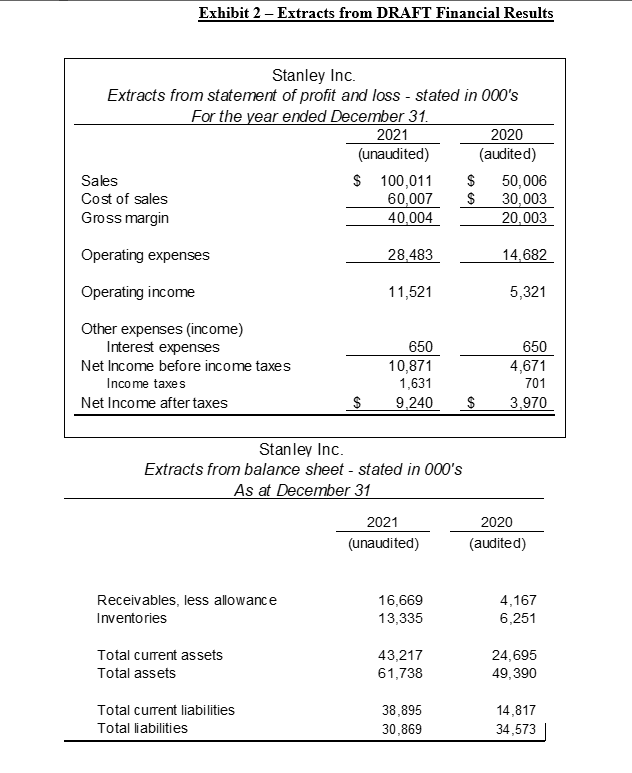

Exhibit 2 Extracts from DRAFT Financial Results

Exhibit 3

SECTIONS FROM THE AUDIT TRAINEEs AUDIT FILE

Part C

The audit procedures relating to inventory from an audit trainees audit files were as follows:

Inventory

At the main warehouse a full count was undertaken on December 31, 2021 by 15 teams of two counters from the warehouse department with Stanelys controller providing overall supervision. Each team of two is allocated several bays within the warehouse to count and they were provided with sequentially numbered inventory sheets which contain product codes and quantities extracted from the inventory records. The counters move through each allocated bay counting the inventory and confirming that it agrees with the inventory sheets. Where a discrepancy was found, they noted this on the sheet.

The warehouse is large and approximately 10% of the bays have been rented out to third parties with similar operations; these are scattered throughout the warehouse. For completeness, the counters were asked to count the inventory for all bays noting that the third-party inventories were recorded on separate blank inventory sheets.

Some of Stanleys goods are high in value and are stored in a locked area of the warehouse. All counting teams were given the code to access this area. There were no despatches of inventory during the count and there were no deliveries from suppliers. Each area is counted once by the allocated team; the sheets are completed in ink, signed by the team and returned after each bay is counted. As no two teams are allocated the same bays, there will be no need to flag that an area has been counted. On completion of the count, the controller will confirm with each team that they have returned their inventory sheets.

Required

i) In respect of the inventory count procedures performed by Stanley Inc, identify and explain four deficiencies that could result in counting errors. Suggest four additional count procedures/controls to prevent the count deficiencies that you identified:

Provide your answer in the table:

Inventory Count Deficiency Explanation of how the deficiency could lead to an errorAdditional Procedure/Control to Prevent the Deficiency

Inventory Count Deficiency (Explanation of how the deficiency could lead to an error Additional Procedure/Control to Prevent the Deficiency

Exhibit 2 - Extracts from DRAFT Financial Results

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Wealth Mastery Unveiled By Marcus M Dawson A Millennial S Guide To Financial Freedom And Success

Authors: Marcus M. Dawson

1st Edition

979-8865054313