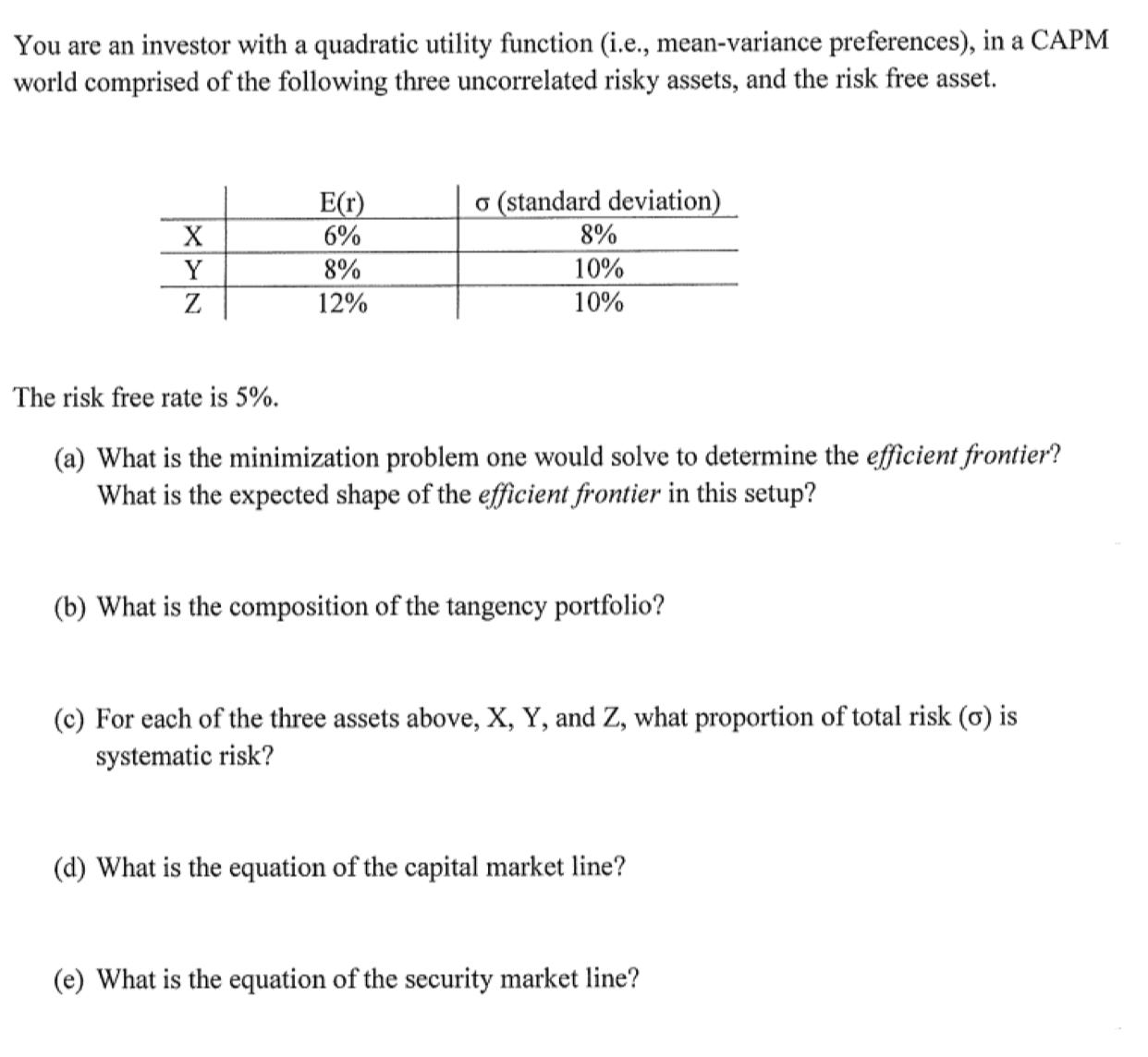

Question: You are an investor with a quadratic utility function ( i . e . , mean - variance preferences ) , in a CAPM world

You are an investor with a quadratic utility function ie meanvariance preferences in a CAPM

world comprised of the following three uncorrelated risky assets, and the risk free asset.

The risk free rate is

a What is the minimization problem one would solve to determine the efficient frontier?

What is the expected shape of the efficient frontier in this setup?

b What is the composition of the tangency portfolio?

c For each of the three assets above, X Y and Z what proportion of total risk is

systematic risk?

d What is the equation of the capital market line?

e What is the equation of the security market line?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock