Answered step by step

Verified Expert Solution

Question

1 Approved Answer

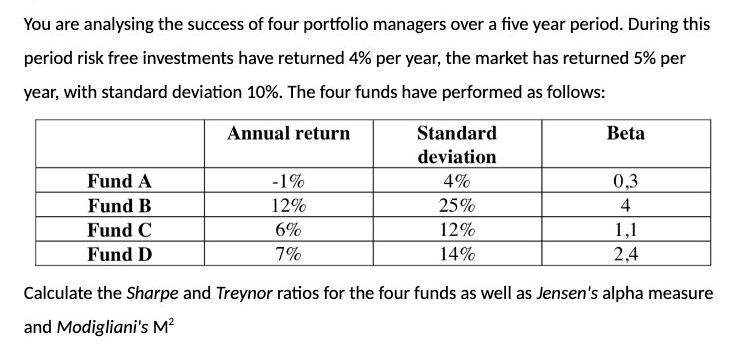

You are analysing the success of four portfolio managers over a five year period. During this period risk free investments have returned 4% per

You are analysing the success of four portfolio managers over a five year period. During this period risk free investments have returned 4% per year, the market has returned 5% per year, with standard deviation 10%. The four funds have performed as follows: Annual return Fund A Fund B Fund C Fund D -1% 12% 6% 7% Standard deviation 4% 25% 12% 14% Beta 0,3 4 1,1 2,4 Calculate the Sharpe and Treynor ratios for the four funds as well as Jensen's alpha measure and Modigliani's M

Step by Step Solution

There are 3 Steps involved in it

Step: 1

To calculate the Sharpe ratio Treynor ratio Jensens alpha and Modiglianis M for the four funds we need the following information Riskfree rate Rf 4 Market return Rm 5 Market standard deviation m 10 Fu...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Management and Cost Accounting

Authors: Colin Drury

8th edition

978-1408041802, 1408041804, 978-1408048566, 1408048566, 978-1408093887