Answered step by step

Verified Expert Solution

Question

1 Approved Answer

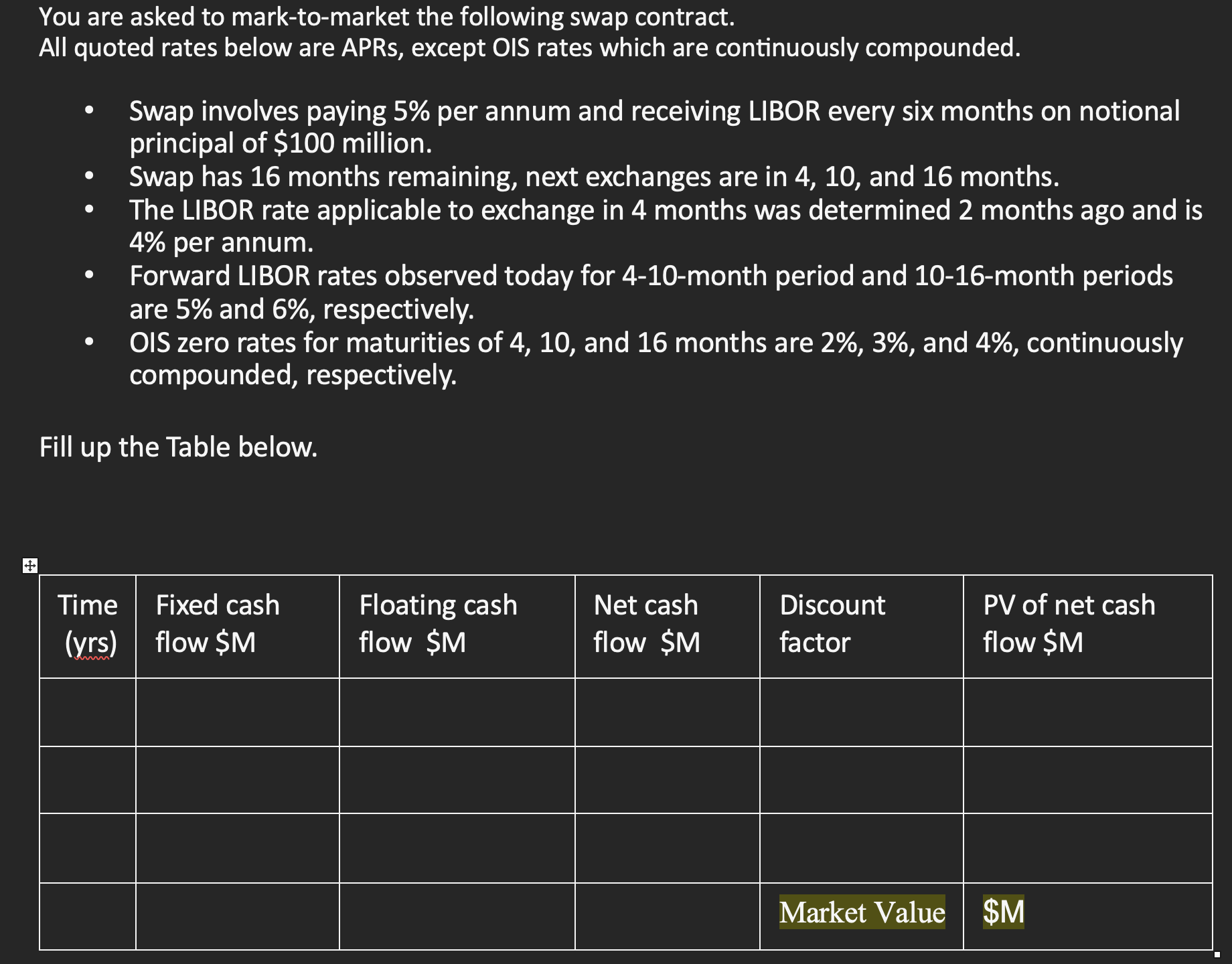

You are asked to mark-to-market the following swap contract. All quoted rates below are APRs, except OIS rates which are continuously compounded. - Swap involves

You are asked to mark-to-market the following swap contract. All quoted rates below are APRs, except OIS rates which are continuously compounded. - Swap involves paying 5\% per annum and receiving LIBOR every six months on notional principal of $100 million. - Swap has 16 months remaining, next exchanges are in 4, 10, and 16 months. - The LIBOR rate applicable to exchange in 4 months was determined 2 months ago and is 4% per annum. - Forward LIBOR rates observed today for 4-10-month period and 10-16-month periods are 5% and 6%, respectively. - OIS zero rates for maturities of 4,10 , and 16 months are 2%,3%, and 4%, continuously compounded, respectively. Fill up the Table below

You are asked to mark-to-market the following swap contract. All quoted rates below are APRs, except OIS rates which are continuously compounded. - Swap involves paying 5\% per annum and receiving LIBOR every six months on notional principal of $100 million. - Swap has 16 months remaining, next exchanges are in 4, 10, and 16 months. - The LIBOR rate applicable to exchange in 4 months was determined 2 months ago and is 4% per annum. - Forward LIBOR rates observed today for 4-10-month period and 10-16-month periods are 5% and 6%, respectively. - OIS zero rates for maturities of 4,10 , and 16 months are 2%,3%, and 4%, continuously compounded, respectively. Fill up the Table below Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Raising Venture Capital

Authors: Rupert Pearce, Simon Barnes

1st Edition

0470027576, 978-0470027578