Answered step by step

Verified Expert Solution

Question

1 Approved Answer

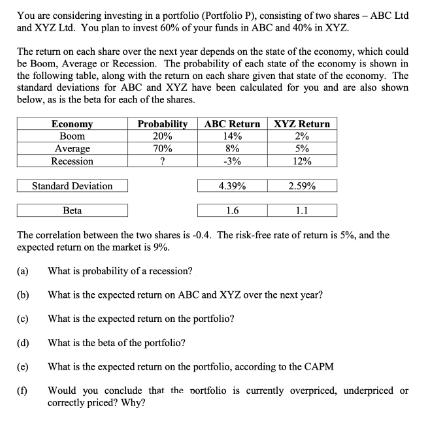

You are considering investing in a portfolio (Portfolio P), consisting of two shares - ABC Ltd and XYZ Ltd. You plan to invest 60%

You are considering investing in a portfolio (Portfolio P), consisting of two shares - ABC Ltd and XYZ Ltd. You plan to invest 60% of your funds in ABC and 40% in XYZ. The return on each share over the next year depends on the state of the economy, which could be Boom, Average or Recession. The probability of each state of the economy is shown in the following table, along with the return on each share given that state of the economy. The standard deviations for ABC and XYZ have been calculated for you and are also shown below, as is the beta for each of the shares. Economy Boom Average Recession (a) (b) (c) (d) (c) (f) Standard Deviation Beta Probability 20% 70% ? ABC Return XYZ Return 14% 2% 8% 5% -3% 12% 4.39% 1.6 2.59% 1.1 The correlation between the two shares is -0.4. The risk-free rate of return is 5%, and the expected return on the market is 9%. What is probability of a recession? What is the expected return on ABC and XYZ over the next year? What is the expected return on the portfolio? What is the beta of the portfolio? What is the expected return on the portfolio, according to the CAPM Would you conclude that the portfolio is currently overpriced, underpriced or correctly priced? Why?

Step by Step Solution

★★★★★

3.26 Rating (144 Votes )

There are 3 Steps involved in it

Step: 1

In the given illustration we have seen probability of boom is 20 probability of avg is 70 A we are g...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Financial Management

Authors: James R Mcguigan, R Charles Moyer, William J Kretlow

10th Edition

978-0324289114, 0324289111