Question

You are considering purchasing a call option with a current stock price of $80 and an exercise price of $82, the option has 91 days

You are considering purchasing a call option with a current stock price of $80 and an exercise price of $82, the option has 91 days to maturity (use a 365-day base), the yearly risk-free rate is currently 2% and the volatility for the option is 0.35.

Calculate the overnight profit or loss on the delta-hedged portfolio if the stock price increases to $84 and if it decreases to $76.

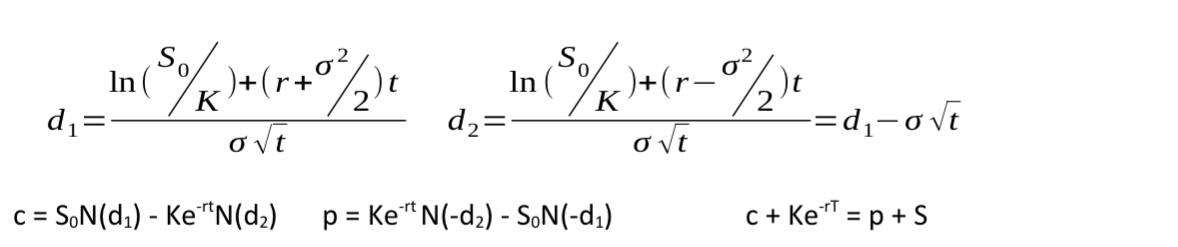

d1=tln(S0/K)+(r+2/2)td2=tln(S0/K)+(r2/2)t=d1tc=S0N(d1)KerrN(d2)p=KeertN(d2)S0N(d1)c+KerT=p+SStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding Healthcare Financial Management

Authors: Louis C. Gapenski, George H. Pink

6th Edition

1567933629, 9781567933628