Answered step by step

Verified Expert Solution

Question

1 Approved Answer

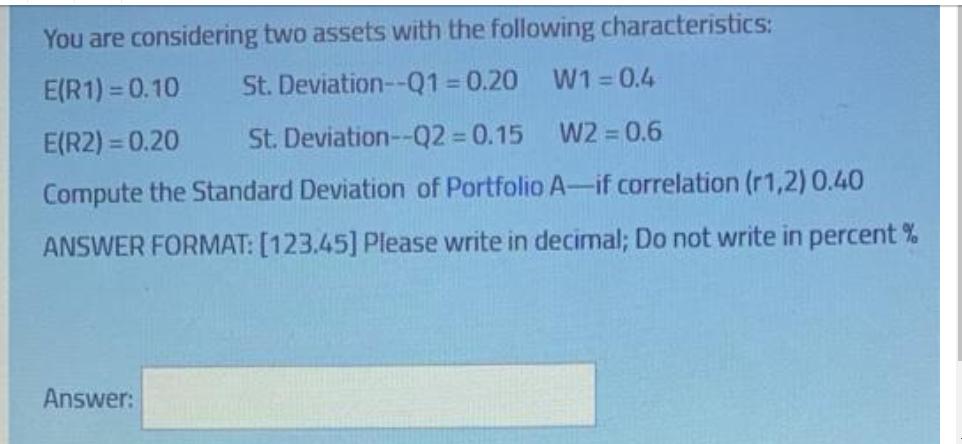

You are considering two assets with the following characteristics: E(R1)=0.10 St. Deviation--Q1=0.20 E(R2) = 0.20 St. Deviation--Q2=0.15 W1 = 0.4 W2=0.6 Compute the Standard

You are considering two assets with the following characteristics: E(R1)=0.10 St. Deviation--Q1=0.20 E(R2) = 0.20 St. Deviation--Q2=0.15 W1 = 0.4 W2=0.6 Compute the Standard Deviation of Portfolio A-if correlation (r1,2) 0.40 ANSWER FORMAT: [123.45] Please write in decimal; Do not write in percent % Answer:

Step by Step Solution

There are 3 Steps involved in it

Step: 1

We can calculate the standard deviation of Portfolio A p using the following steps ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investment Analysis and Portfolio Management

Authors: Frank K. Reilly, Keith C. Brown

10th Edition

538482109, 1133711774, 538482389, 9780538482103, 9781133711773, 978-0538482387