Answered step by step

Verified Expert Solution

Question

1 Approved Answer

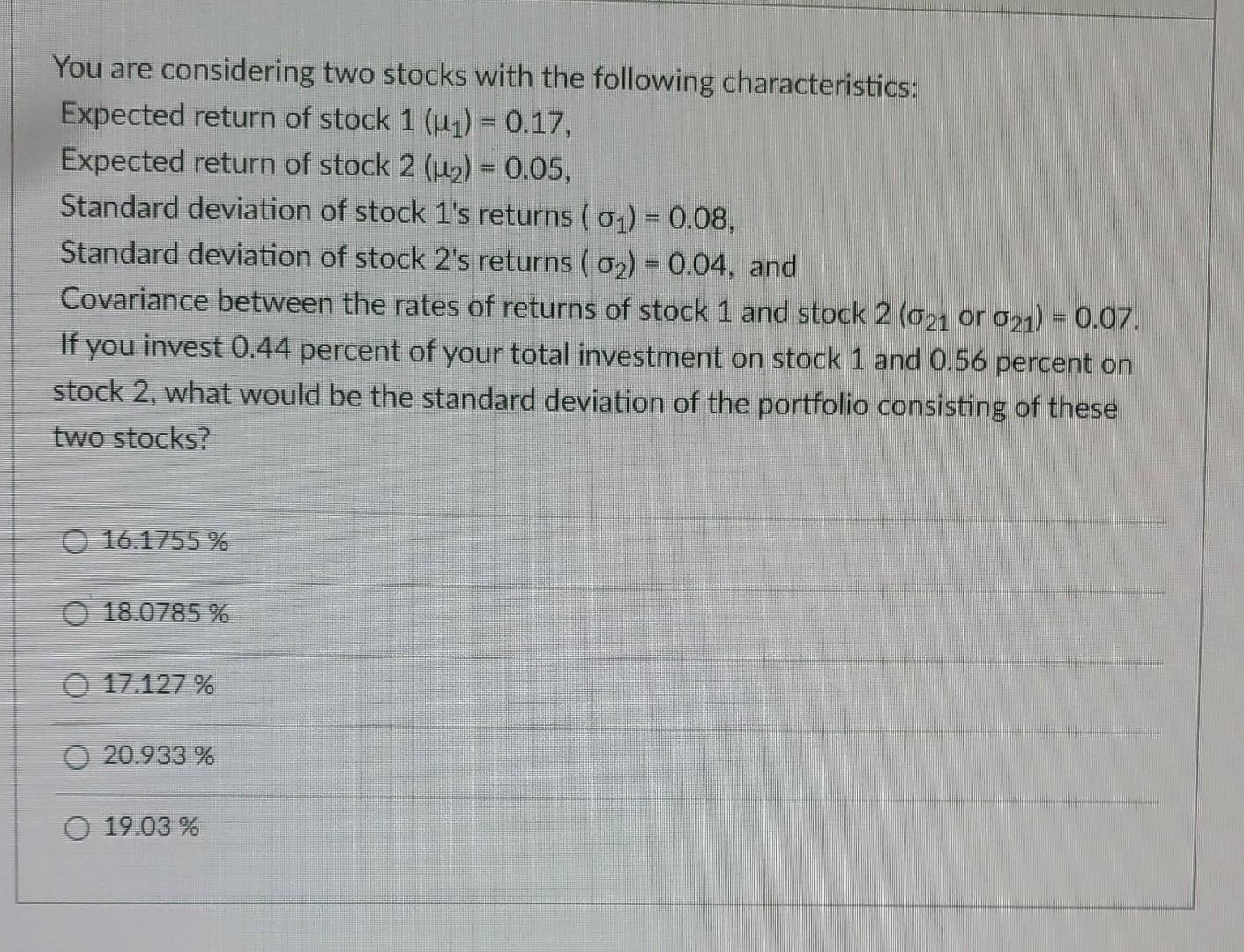

You are considering two stocks with the following characteristics: Expected return of stock 1 (41) = 0.17, Expected return of stock 2 (uz) = 0.05,

You are considering two stocks with the following characteristics: Expected return of stock 1 (41) = 0.17, Expected return of stock 2 (uz) = 0.05, Standard deviation of stock 1's returns (01) = 0.08, Standard deviation of stock 2's returns (02) = 0.04, and Covariance between the rates of returns of stock 1 and stock 2 (021 or 021) = 0.07. If you invest 0.44 percent of your total investment on stock 1 and 0.56 percent on stock 2, what would be the standard deviation of the portfolio consisting of these two stocks? O 16.1755 % O 18.0785 % 0 17.127 % 20.933 % 19.03%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting Ledger Book

Authors: Alpha Planners Publishing

1st Edition

B09VWKPJSG, 979-8432472564