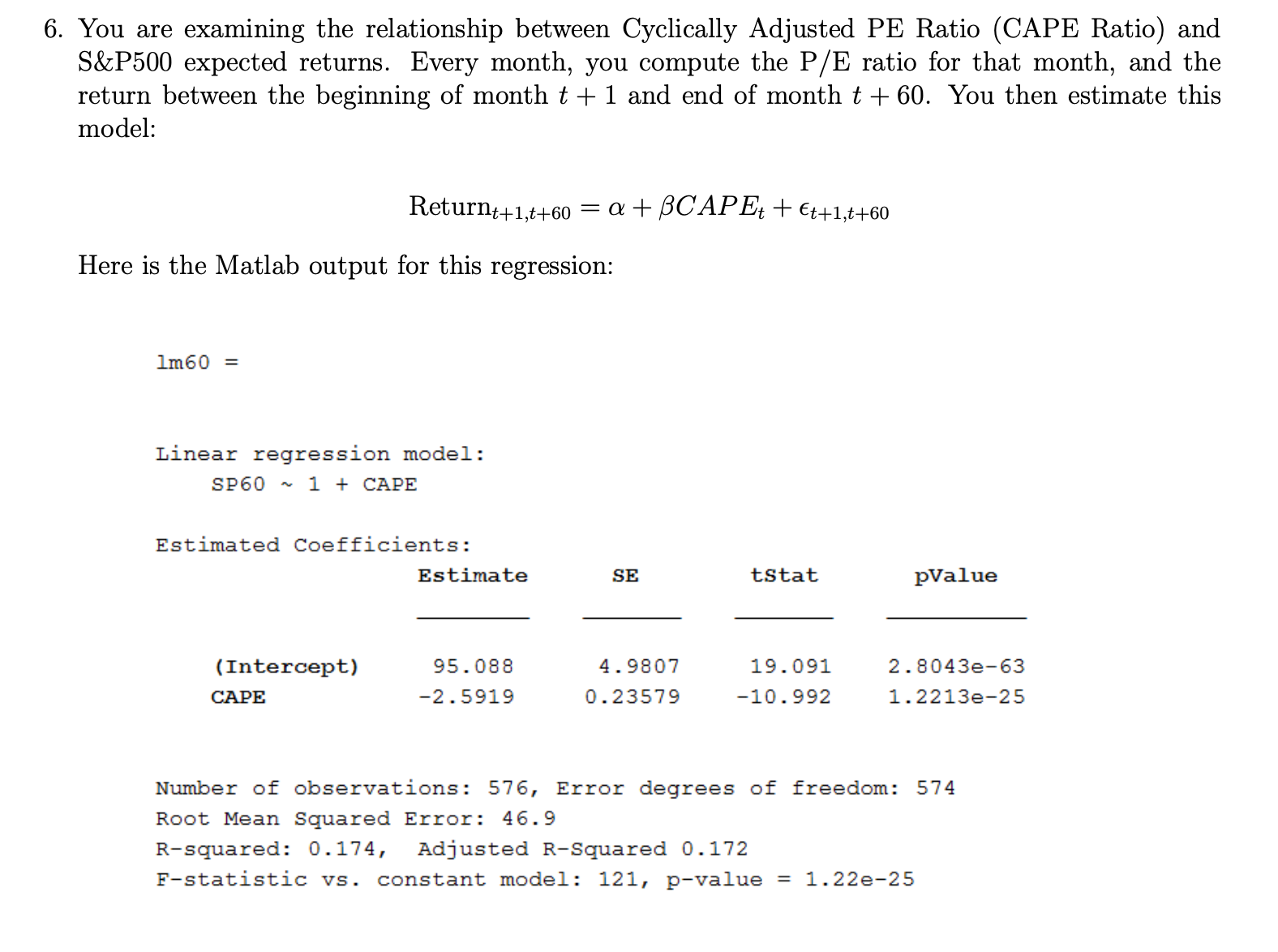

You are examining the relationship between Cyclically Adjusted PE Ratio (CAPE Ratio) and S&P500 expected returns. Every month, you compute the P/E ratio for that month, and the return between the beginning of montht+ 1 and end of montht+ 60. You then estimate this model:

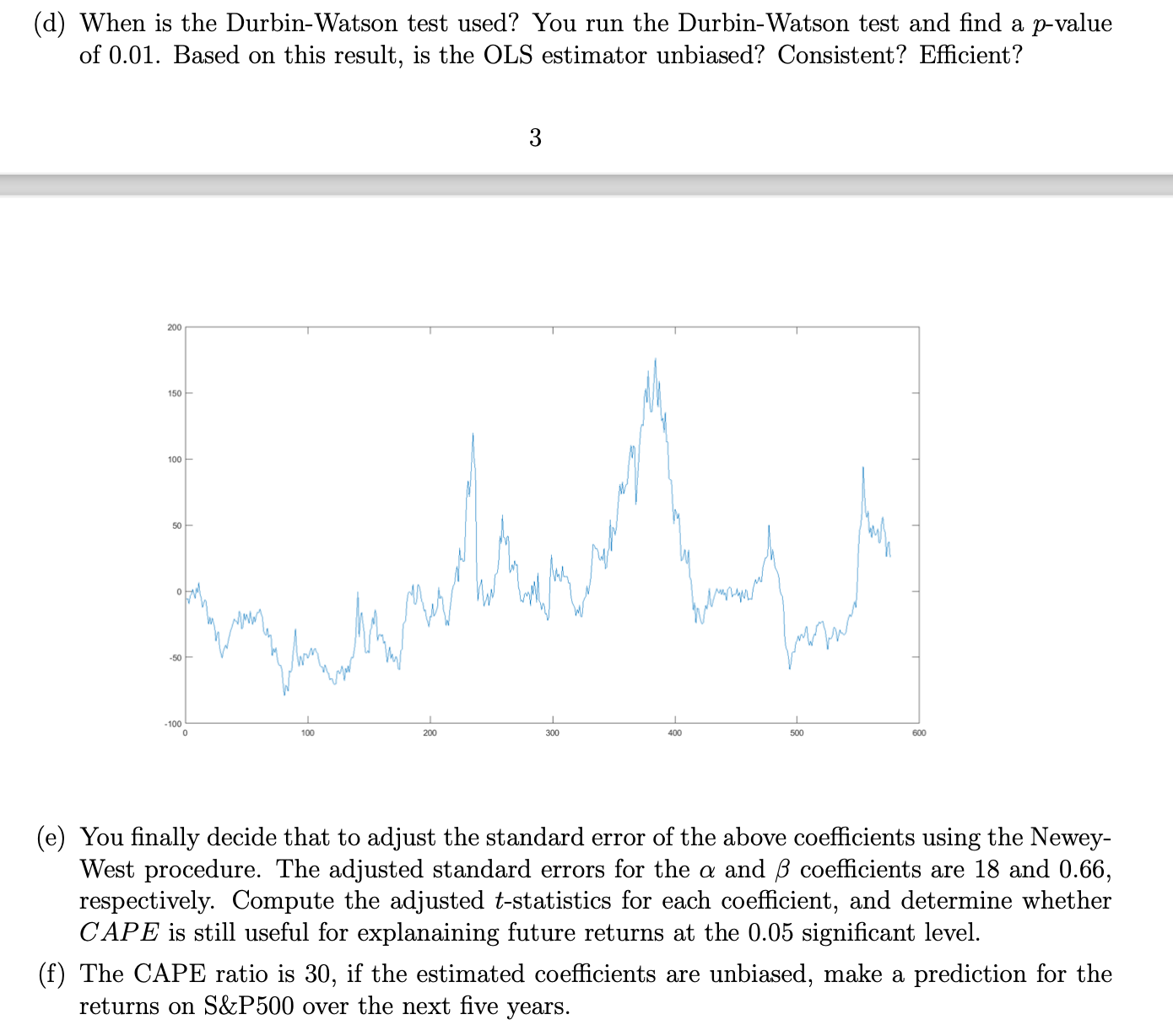

6. You are examining the relationship between Cyclically Adjusted PE Ratio (CAPE Ratio) and S&P500 expected returns. Every month, you compute the P/E ratio for that month, and the return between the beginning of month t + 1 and end of month t + 60. You then estimate this model: Returnt+1,t+60 = a + BCAPEt + Et+1,t+60 Here is the Matlab output for this regression: 1m60 = Linear regression model: SP60 ~ 1 + CAPE Estimated Coefficients: Estimate SE tstat pValue (Intercept) 95 . 088 4. 9807 19 . 091 2. 8043e-63 CAPE -2 . 5919 0. 23579 -10.992 1. 2213e-25 Number of observations: 576, Error degrees of freedom: 574 Root Mean Squared Error: 46.9 R-squared: 0.174, Adjusted R-Squared 0. 172 F-statistic vs. constant model: 121, p-value = 1.22e-25(a) Determine whether CAPE is useful for explanaining future returns. Use a 0.05 signicant level to make your decision. Explain the meaning of R2 for the regression. (b) You are concerned about that the t-statistic on the independent variable, you plot the time- series residuals of the regression below. Do you observe any potential trend in residuals? What assumption might be violated? (c) When is the BreuchPagan test used? You run the BreuchPagan test for the above regression and nd a pvalue of 0.43. Based on this result, is the OLS estimator unbiased? Consistent? Efcient? (d) When is the Durbin-Watson test used? You run the Durbin-Watson test and find a p-value of 0.01. Based on this result, is the OLS estimator unbiased? Consistent? Efficient? 3 200 150 100 50 50 -100 100 200 300 400 500 (e) You finally decide that to adjust the standard error of the above coefficients using the Newey- West procedure. The adjusted standard errors for the a and S coefficients are 18 and 0.66, respectively. Compute the adjusted t-statistics for each coefficient, and determine whether CAPE is still useful for explanatning future returns at the 0.05 significant level. (f) The CAPE ratio is 30, if the estimated coefficients are unbiased, make a prediction for the returns on S&P500 over the next five years