Answered step by step

Verified Expert Solution

Question

1 Approved Answer

You are given that the fair price to pay at time for a derivative paying X at time T is V = e)E[X|F], where

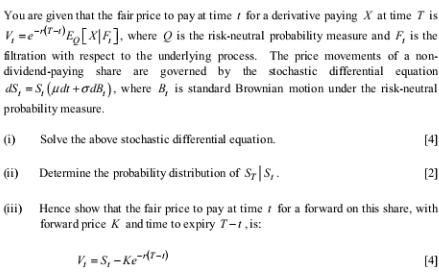

You are given that the fair price to pay at time for a derivative paying X at time T is V = e)E[X|F], where Q is the risk-neutral probability measure and F, is the filtration with respect to the underlying process. The price movements of a non- dividend-paying share are governed by the stochastic differential equation dS, =S, (udt+odB,), where B, is standard Brownian motion under the risk-neutral probability measure. Solve the above stochastic differential equation. Determine the probability distribution of Sr|S,. Hence show that the fair price to pay at time for a forward on this share, with forward price K and time to expiry T-1.is: V=S-Ke-(T-1) (i) (ii) (iii) [4] [2] [4]

Step by Step Solution

★★★★★

3.39 Rating (171 Votes )

There are 3 Steps involved in it

Step: 1

i Given the SDE dSt Stdt dBt We can solve this using It...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

An Introduction to the Mathematics of Financial Derivatives

Authors: Ali Hirsa, Salih N. Neftci

3rd edition

012384682X, 978-0123846822