Answered step by step

Verified Expert Solution

Question

1 Approved Answer

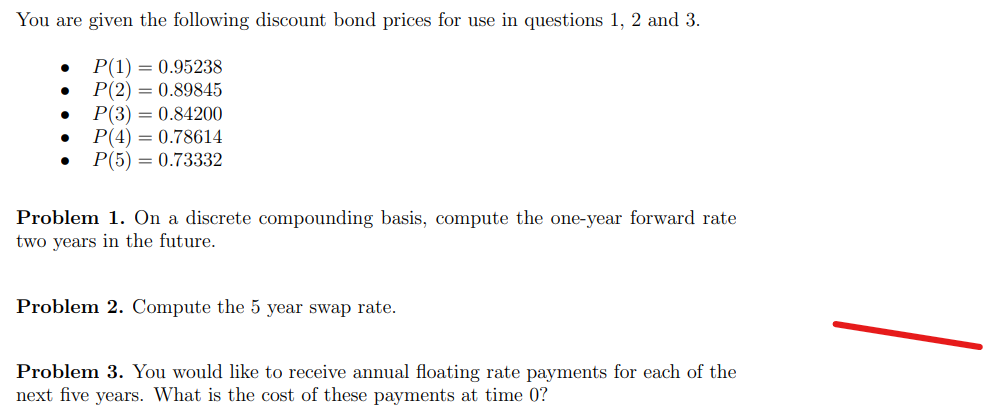

You are given the following discount bond prices for use in questions 1,2 and 3 . - P(1)=0.95238 - P(2)=0.89845 - P(3)=0.84200 - P(4)=0.78614 -

You are given the following discount bond prices for use in questions 1,2 and 3 . - P(1)=0.95238 - P(2)=0.89845 - P(3)=0.84200 - P(4)=0.78614 - P(5)=0.73332 Problem 1. On a discrete compounding basis, compute the one-year forward rate two years in the future. Problem 2. Compute the 5 year swap rate. Problem 3. You would like to receive annual floating rate payments for each of the next five years. What is the cost of these payments at time 0

You are given the following discount bond prices for use in questions 1,2 and 3 . - P(1)=0.95238 - P(2)=0.89845 - P(3)=0.84200 - P(4)=0.78614 - P(5)=0.73332 Problem 1. On a discrete compounding basis, compute the one-year forward rate two years in the future. Problem 2. Compute the 5 year swap rate. Problem 3. You would like to receive annual floating rate payments for each of the next five years. What is the cost of these payments at time 0 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Planning Demystified A Self Teaching Guide

Authors: Paul Lim

1st Edition

0071476717,0071709711