Answered step by step

Verified Expert Solution

Question

1 Approved Answer

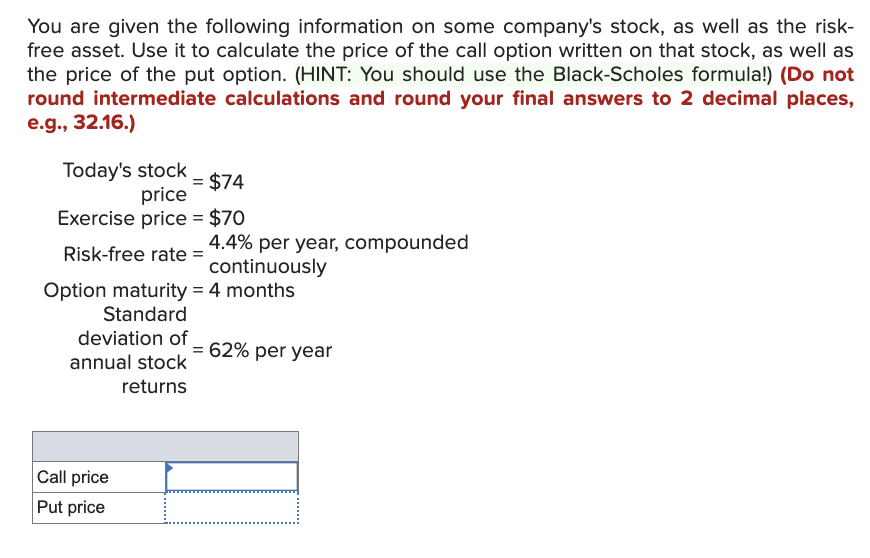

You are given the following information on some company's stock, as well as the risk - free asset. Use it to calculate the price of

You are given the following information on some company's stock, as well as the risk

free asset. Use it to calculate the price of the call option written on that stock, as well as

the price of the put option. HINT: You should use the BlackScholes formula!Do not

round intermediate calculations and round your final answers to decimal places,

eg

Today's stock

price $

Exercise price $

Riskfree rate per year, compounded

Option maturity months

Standard deviation of annual stock per year

returns

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance And Financial Intermediation

Authors: Harold L. Cole

1st Edition

0190941707, 978-0190941703