Answered step by step

Verified Expert Solution

Question

1 Approved Answer

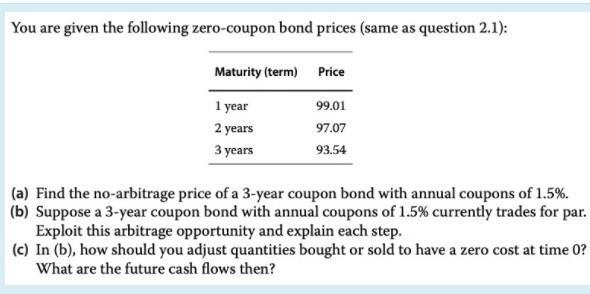

You are given the following zero-coupon bond prices (same as question 2.1): Maturity (term) Price 1 year 99.01 2 years 97.07 3 years 93.54

You are given the following zero-coupon bond prices (same as question 2.1): Maturity (term) Price 1 year 99.01 2 years 97.07 3 years 93.54 (a) Find the no-arbitrage price of a 3-year coupon bond with annual coupons of 1.5%. (b) Suppose a 3-year coupon bond with annual coupons of 1.5% currently trades for par. Exploit this arbitrage opportunity and explain each step. (c) In (b), how should you adjust quantities bought or sold to have a zero cost at time 0? What are the future cash flows then?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Theory and Corporate Policy

Authors: Thomas E. Copeland, J. Fred Weston, Kuldeep Shastri

4th edition

321127218, 978-0321179548, 321179544, 978-0321127211