Answered step by step

Verified Expert Solution

Question

1 Approved Answer

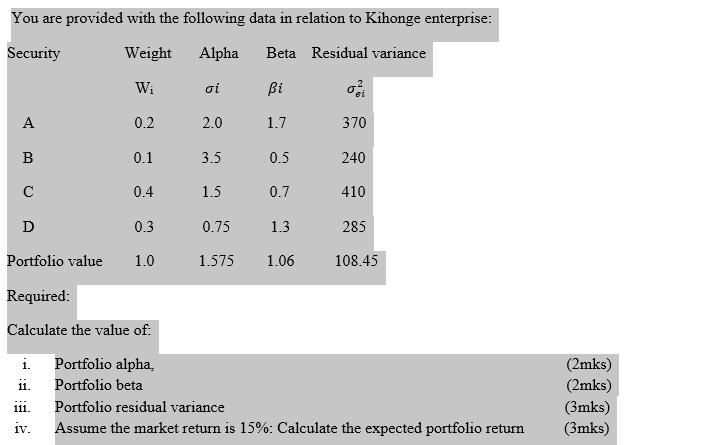

You are provided with the following data in relation to Kihonge enterprise: Security Weight Alpha Beta Residual variance Wi A 0.2 2.0 1.7 370

You are provided with the following data in relation to Kihonge enterprise: Security Weight Alpha Beta Residual variance Wi A 0.2 2.0 1.7 370 B 0.1 3.5 0.5 240 C 0.4 1.5 0.7 410 D 0.3 0.75 1.3 285 Portfolio value 1.0 1.575 1.06 108.45 Required: Calculate the value of: i. Portfolio alpha, (2mks) 11. Portfolio beta (2mks) 111. Portfolio residual variance (3mks) iv. Assume the market return is 15%: Calculate the expected portfolio return (3mks)

Step by Step Solution

★★★★★

3.40 Rating (156 Votes )

There are 3 Steps involved in it

Step: 1

lets calculate the requested portfolio metrics for Kihonge enterprise i Portfolio Alpha Portfolio alpha represents the excess return of the portfolio ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial and managerial accounting

Authors: Jerry J. Weygandt, Paul D. Kimmel, Donald E. Kieso

1st edition

111800423X, 9781118233443, 1118016114, 9781118004234, 1118233441, 978-1118016114