Answered step by step

Verified Expert Solution

Question

1 Approved Answer

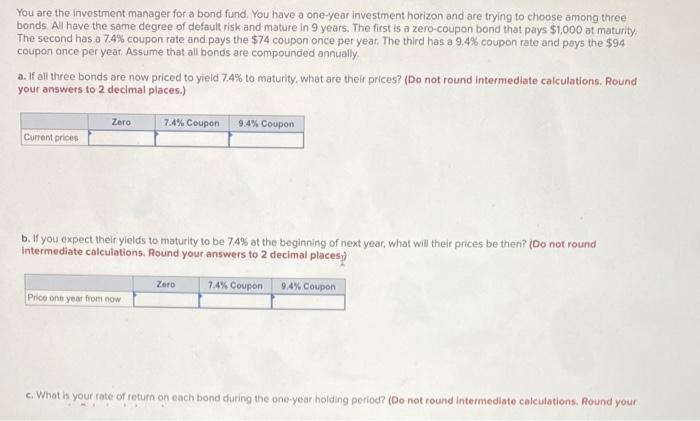

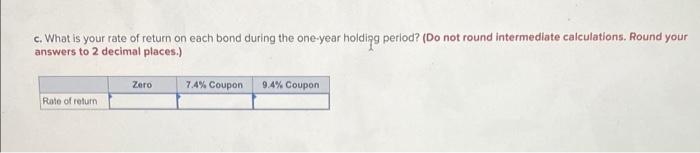

You are the investment manager for a bond fund. You have a one-year investment horizon and are trying to choose among three bonds. All have

You are the investment manager for a bond fund. You have a one-year investment horizon and are trying to choose among three bonds. All have the same degree of default risk and mature in 9 years. The first is a zero-coupon bond that pays $1,000 at maturity, The second has a 74% coupon rate and pays the $74 coupon once per year. The third has a 9,4% coupon rate and pays the $94 coupon once per year. Assume that all bonds are compounded annually a. If all three bonds are now priced to yield 7.4% to maturity, what are their prices? (Do not round intermediate calculations. Round your answers to 2 decimal places.) Zero 7.4% Coupon 9.4% Coupon Current prices b. If you expect their yields to maturity to be 74% at the beginning of next year, what will their prices be then? (Do not round Intermediate calculations. Round your answers to 2 decimal places) Zoro 7.4% Coupon 0.4% Coupon Price one year from now c. What is your rate of return on each bond during the one year holding period? (Do not round intermediate calculations. Round your c. What is your rate of return on each bond during the one-year holdipa perlod? (Do not round intermediate calculations. Round your answers to 2 decimal places.) Zero 7.4% Coupon 9.4% Coupon Rate of return

You are the investment manager for a bond fund. You have a one-year investment horizon and are trying to choose among three bonds. All have the same degree of default risk and mature in 9 years. The first is a zero-coupon bond that pays $1,000 at maturity, The second has a 74% coupon rate and pays the $74 coupon once per year. The third has a 9,4% coupon rate and pays the $94 coupon once per year. Assume that all bonds are compounded annually a. If all three bonds are now priced to yield 7.4% to maturity, what are their prices? (Do not round intermediate calculations. Round your answers to 2 decimal places.) Zero 7.4% Coupon 9.4% Coupon Current prices b. If you expect their yields to maturity to be 74% at the beginning of next year, what will their prices be then? (Do not round Intermediate calculations. Round your answers to 2 decimal places) Zoro 7.4% Coupon 0.4% Coupon Price one year from now c. What is your rate of return on each bond during the one year holding period? (Do not round intermediate calculations. Round your c. What is your rate of return on each bond during the one-year holdipa perlod? (Do not round intermediate calculations. Round your answers to 2 decimal places.) Zero 7.4% Coupon 9.4% Coupon Rate of return

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Wealth Grow It And Protect It

Authors: Stuart E. Lucas

1st Edition

0134194659,0133132838