Answered step by step

Verified Expert Solution

Question

1 Approved Answer

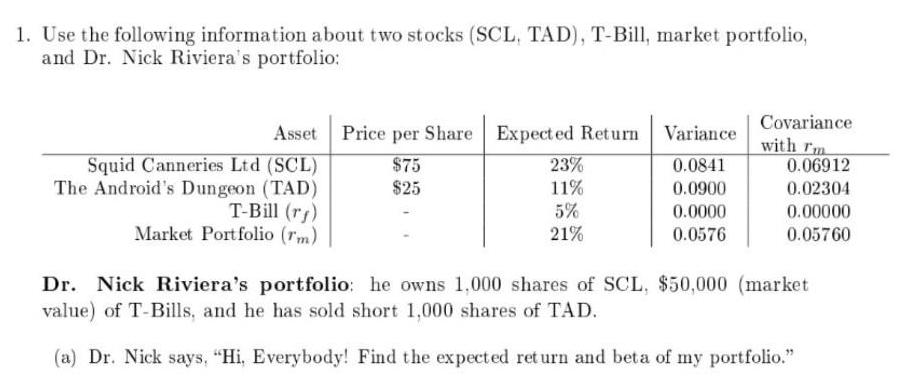

1. Use the following information about two stocks (SCL, TAD), T-Bill, market portfolio, and Dr. Nick Riviera's portfolio: Asset Price per Share Expected Return

1. Use the following information about two stocks (SCL, TAD), T-Bill, market portfolio, and Dr. Nick Riviera's portfolio: Asset Price per Share Expected Return Variance $75 $25 Squid Canneries Ltd (SCL) The Android's Dungeon (TAD) T-Bill (r) Market Portfolio (rm) 23% 11% 5% 21% 0.0841 0.0900 0.0000 0.0576 Covariance with rm 0.06912 0.02304 0.00000 0.05760 Dr. Nick Riviera's portfolio: he owns 1,000 shares of SCL, $50,000 (market value) of T-Bills, and he has sold short 1,000 shares of TAD. (a) Dr. Nick says, "Hi, Everybody! Find the expected return and beta of my portfolio."

Step by Step Solution

★★★★★

3.63 Rating (164 Votes )

There are 3 Steps involved in it

Step: 1

To find the expected return and beta of Dr Nick Rivieras portfolio we can use the weighted average o...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Economics and Business Strategy

Authors: Michael R. baye

7th Edition

978-0073375960, 71267441, 73375969, 978-0071267441