Question: You, CPA, work as the assistant controller for A-Plus Corp (A-Plus). You are currently working on a project with the mergers and acquisitions group, which

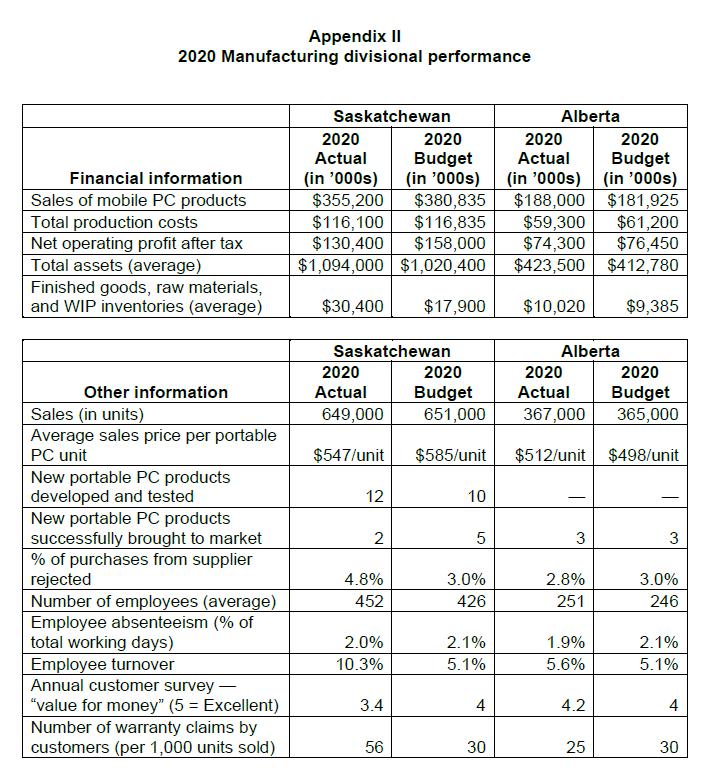

You, CPA, work as the assistant controller for A-Plus Corp (A-Plus). You are currently working on a project with the mergers and acquisitions group, which is responsible for integrating the recent acquisition of Business Intelligence Management Inc. (BIM), a portable PC producer with two geographical divisions: Saskatchewan and Alberta (Appendix I). It is May 7, 2021, and the CFO has recently discovered that the two divisional managers responsible for BIM's operations are due to be paid their 2020 performance bonuses in less than a week. The CFO provided you with the financial and non-financial data for the operations in Saskatchewan and Alberta (Appendix II). Both managers' employment agreements state the following: 1. The bonus must be paid by May 13, 2021. 2. The bonus amount is capped at $110,000. 3. The bonus amount awarded must be justified in writing. There hasn't been a structured approach for determining the managers' bonuses in the past. Therefore, the CFO is debating between two bonus structures and has asked you to discuss and calculate the bonuses under each option and provide a recommendation on which bonus structure to use. Specifically: 1. The CFO would like you to assess what type of responsibility centre these two divisions are, and to identify a relevant financial measure to assess performance of the divisions based on that classification. He would like you to use the divisional performance (related to that measure) to determine the managers' bonuses. 2. The CFO would like you to draft a balanced scorecard that both divisions can use. He would like you to assess each division's performance based on that scorecard and determine the managers' bonuses based on the divisional performance. The CFO also received a call from the Saskatchewan division manager about concerns over divisional financial performance. The Saskatchewan division manufactures wafer chips that it uses in its own products and also provides wafer chips to the Alberta division for its production needs (Appendix I). The manager is concerned about the impact of the transfer on her division's financial performance. Specifically, the Saskatchewan division manager is worried how it will impact her bonus. The CFO has asked you to recommend an appropriate transfer pricing policy and determine the impact on divisional results. Appendix I - Background information Until recently, A-Plus focused on sourcing no-name electronics from Asian countries and then reselling these goods to electronics retailers in North America. On January 1, 2021, A-Plus expanded into electronics manufacturing by acquiring BIM, which specializes in manufacturing portable PC devices, such as laptops. BIM employs 700 individuals. BIM's operations are divided into two geographical regions: Saskatchewan and Alberta. The Saskatchewan division has three plants and the Alberta division has one central plant. Portable PC device manufacturing is a mass production industry, with high volumes of identical or similar products manufactured using assembly lines. Successful portable PC device manufacturers turn over their inventory quickly due to the rapid pace of technology changes. Products are generally made to order for customers — either other electronics companies, which then place their own brand on the units and resell them, or large national electronics retail chains, which place their store brand on the units and resell them. Each division is responsible for developing its own customer base, meeting sales targets, and managing costs. The manufacturing of portable PC devices is still a relatively labour-intensive process because many of the components need to be assembled precisely. Although the Saskatchewan division manufactures wafer chips in one of its plants, most of the electronic components used in BIM's manufacturing process are bought from third-party suppliers. The employees who assemble the components are mainly semi-skilled and have been trained by BIM to perform fairly simple, repetitive operations on the assembly line. When the units are completed, the quality assurance department tests them, and any units that are found to be faulty are returned to the assembly line and reworked. Because quality is key, all electronic components received from suppliers are also tested by BIM's quality assurance department. They do not have the time to test every component; therefore, they test a sample of components from each batch delivered. If they find more than one faulty component in every 20 tested, the whole batch is rejected and returned to the supplier. To maintain assembly line equipment in peak performance, division managers must carefully maintain maintenance schedules and are responsible for determining and budgeting for capital expenditure needs. The Saskatchewan division manufactures the wafer chips needed in many of the Alberta division's products. The corporate policy of BIM's previous executive team was for the Saskatchewan division to sell the wafer chips to the Alberta division at $10 per chip (Saskatchewan division's average production cost). The external market price for this type of wafer chip averaged $20 per chip in 2020. The Saskatchewan division is currently manufacturing wafer chips at capacity, and if it did not have to supply the Alberta division's operations, it could have sold all 330,000 chips delivered to the Alberta division to external companies in 2020. BIM's effective corporate tax rate is 11%. Appendix II - 2020 Manufacturing divisional performance REQUIREDS:

Appendix II 2020 Manufacturing divisional performance Saskatchewan 2020 Actual 2020 Budget Financial information Sales of mobile PC products Total production costs Net operating profit after tax Total assets (average) Finished goods, raw materials, and WIP inventories (average) (in '000s) (in '000s) (in '000s) $355,200 $380,835 $188,000 2020 Alberta Actual 2020 Budget (in '000s) $181,925 $116,100 $116,835 $59,300 $61,200 $130,400 $1,094,000 $1,020,400 $158,000 $74,300 $76,450 $423,500 $412,780 $30,400 $17,900 $10,020 $9,385 Saskatchewan Alberta 2020 Other information Actual 2020 Budget 2020 2020 Actual Budget Sales (in units) 649,000 651,000 367,000 365,000 Average sales price per portable PC unit $547/unit $585/unit $512/unit $498/unit New portable PC products developed and tested 12 10 New portable PC products successfully brought to market 2 5 3 3 % of purchases from supplier rejected 4.8% 3.0% 2.8% 3.0% Number of employees (average) 452 426 251 246 Employee absenteeism (% of total working days) 2.0% 2.1% 1.9% 2.1% Employee turnover 10.3% 5.1% 5.6% 5.1% Annual customer survey. "value for money" (5 Excellent) 3.4 4 4.2 4 Number of warranty claims by customers (per 1,000 units sold) 56 30 25 30

Step by Step Solution

3.41 Rating (154 Votes )

There are 3 Steps involved in it

1 Transfer Pricing Policy Recommendation Given the concern raised by the Saskatchewan division manager about the impact of transfer pricing on divisional financial performance and her bonus its essent... View full answer

Get step-by-step solutions from verified subject matter experts