Answered step by step

Verified Expert Solution

Question

1 Approved Answer

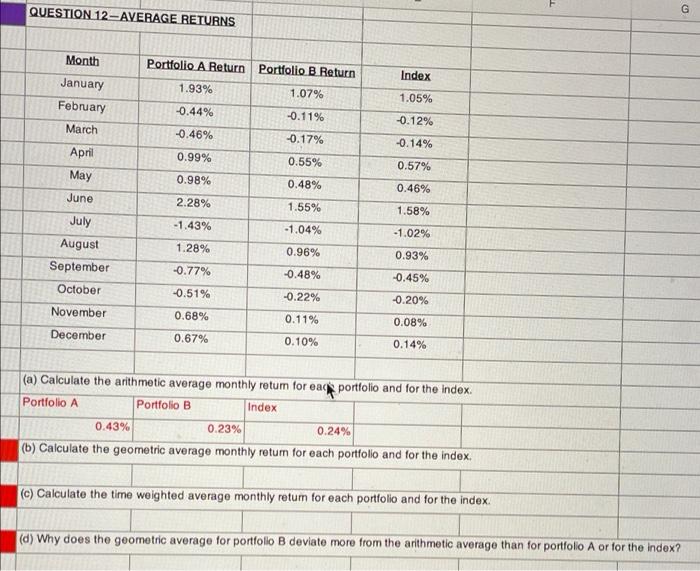

you dont need to solve a please use excel to solve B C and A QUESTION 12-AVERAGE RETURNS G Portfolio A Return 1.93% Portfolio B

you dont need to solve a please use excel to solve B C and A  QUESTION 12-AVERAGE RETURNS G Portfolio A Return 1.93% Portfolio B Return Month January February Index 1.07% 1.05% -0.44% -0.11% -0.12% March -0.46% -0.17% -0.14% 0.99% April May 0.55% 0.57% 0.98% 0.48% 0.46% June 2.28% 1.55% 1.58% -1.43% -1.04% -1.02% July August September 1.28% 0.96% 0.93% -0.77% -0.48% -0.45% October -0.51% -0.22% -0.20% November 0.68% 0.11% 0.08% December 0.67% 0.10% 0.14% (a) Calculate the arithmetic average monthly retum for each portfolio and for the Index. Portfolio A Portfolio B Index 0.43% 0.23% 0.24% (b) Calculate the geometric average monthly return for each portfolio and for the index. (c) Calculate the time weighted average monthly retum for each portfolio and for the index, (d) Why does the geometric average for portfolio B deviate more from the arithmetic average than for portfolio A or for the index

QUESTION 12-AVERAGE RETURNS G Portfolio A Return 1.93% Portfolio B Return Month January February Index 1.07% 1.05% -0.44% -0.11% -0.12% March -0.46% -0.17% -0.14% 0.99% April May 0.55% 0.57% 0.98% 0.48% 0.46% June 2.28% 1.55% 1.58% -1.43% -1.04% -1.02% July August September 1.28% 0.96% 0.93% -0.77% -0.48% -0.45% October -0.51% -0.22% -0.20% November 0.68% 0.11% 0.08% December 0.67% 0.10% 0.14% (a) Calculate the arithmetic average monthly retum for each portfolio and for the Index. Portfolio A Portfolio B Index 0.43% 0.23% 0.24% (b) Calculate the geometric average monthly return for each portfolio and for the index. (c) Calculate the time weighted average monthly retum for each portfolio and for the index, (d) Why does the geometric average for portfolio B deviate more from the arithmetic average than for portfolio A or for the index

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Credit Spreads Beginners Guide To Low Risk Secure Easy To Manage Consistent Profits For Long Term Wealth Creation

Authors: Casey Boon

1st Edition

1974677419, 978-1974677412