Answered step by step

Verified Expert Solution

Question

1 Approved Answer

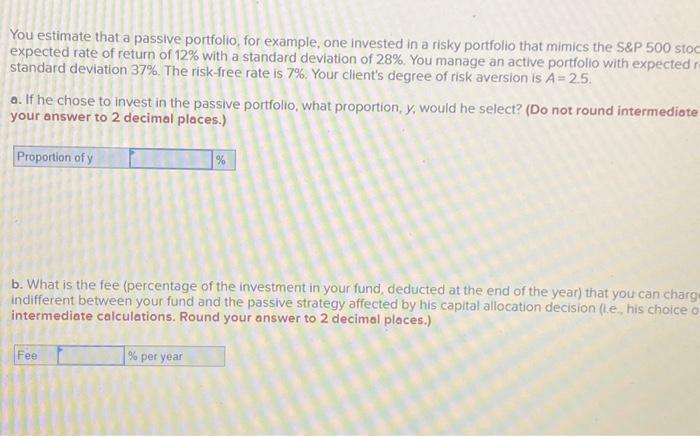

You estimate that a passive portfolio, for example, one invested in a risky portfolio that mimics the S&P 500 stoc expected rate of return of

You estimate that a passive portfolio, for example, one invested in a risky portfolio that mimics the S&P 500 stoc expected rate of return of 12% with a standard deviation of 28%. You manage an active portfolio with expected re standard deviation 37%. The risk-free rate is 7%. Your client's degree of risk aversion is A = 2.5. a. If he chose to invest in the passive portfolio, what proportion, y, would he select? (Do not round intermediate your answer to 2 decimal places.) Proportion of y

b. What is the fee (percentage of the investment in your fund, deducted at the end of the year) that you can charge indifferent between your fund and the passive strategy affected by his capital allocation decision (i.e., his choice o intermediate calculations. Round your answer to 2 decimal places.) Fee % % per year

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

COMMENT INVESTIR ABC DE LA FINANCE

Authors: OLIVIER CHAZOULE

1st Edition

2020367521, 978-2020367523