Answered step by step

Verified Expert Solution

Question

1 Approved Answer

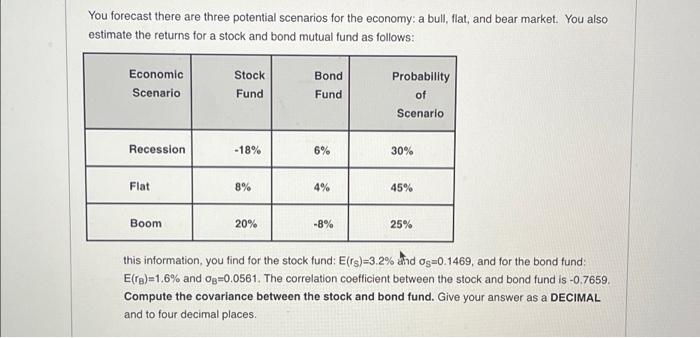

You forecast there are three potential scenarios for the economy: a bull, flat, and bear market. You also estimate the returns for a stock and

You forecast there are three potential scenarios for the economy: a bull, flat, and bear market. You also estimate the returns for a stock and bond mutual fund as follows: Economic Scenario Recession Flat Boom Stock Fund -18% 8% 20% Bond Fund 6% 4% -8% Probability of Scenario 30% 45% 25% this information, you find for the stock fund: E(rs)-3.2% and os=0.1469, and for the bond fund: E(rB)=1.6% and OB=0.0561. The correlation coefficient between the stock and bond fund is -0.7659. Compute the covariance between the stock and bond fund. Give your answer as a DECIMAL and to four decimal places.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Successful Fundraising For Arts And Cultural Organizations

Authors: Carolyn S. Friedman, Karen B. Hopkins

2nd Edition

1573560294, 978-1573560290