Answered step by step

Verified Expert Solution

Question

1 Approved Answer

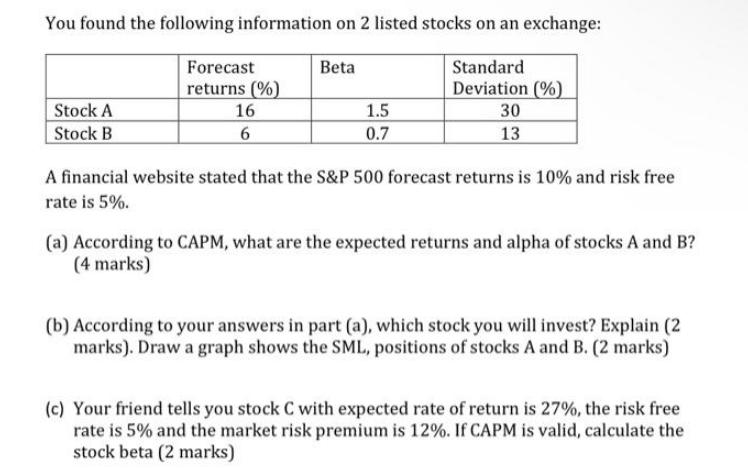

You found the following information on 2 listed stocks on an exchange: Standard Deviation (%) 30 13 Stock A Stock B Forecast returns (%)

You found the following information on 2 listed stocks on an exchange: Standard Deviation (%) 30 13 Stock A Stock B Forecast returns (%) 16 6 Beta 1.5 0.7 A financial website stated that the S&P 500 forecast returns is 10% and risk free rate is 5%. (a) According to CAPM, what are the expected returns and alpha of stocks A and B? (4 marks) (b) According to your answers in part (a), which stock you will invest? Explain (2 marks). Draw a graph shows the SML, positions of stocks A and B. (2 marks) (c) Your friend tells you stock C with expected rate of return is 27%, the risk free rate is 5% and the market risk premium is 12%. If CAPM is valid, calculate the stock beta (2 marks)

Step by Step Solution

★★★★★

3.39 Rating (149 Votes )

There are 3 Steps involved in it

Step: 1

a Expected Returns and Alpha of Stocks A and B Expected Return Using the Capital Asset Pricing Model ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Income Tax Fundamentals 2013

Authors: Gerald E. Whittenburg, Martha Altus Buller, Steven L Gill

31st Edition

1111972516, 978-1285586618, 1285586611, 978-1285613109, 978-1111972516