Answered step by step

Verified Expert Solution

Question

1 Approved Answer

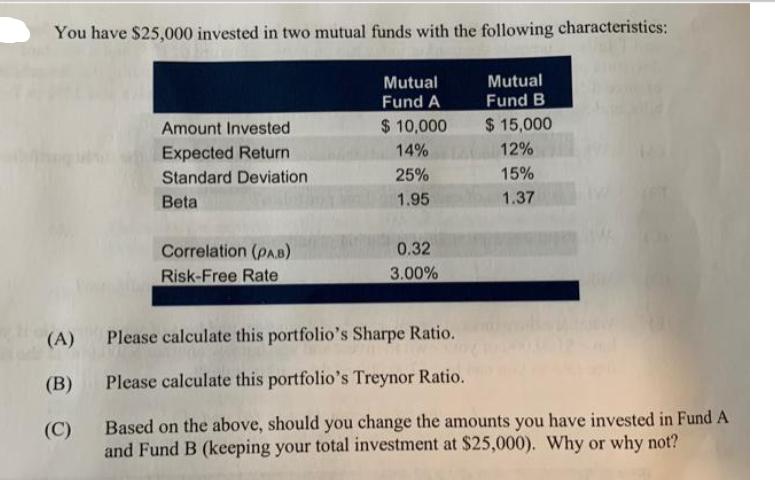

You have $25,000 invested in two mutual funds with the following characteristics: Mutual Fund A Mutual Fund B Amount Invested $ 10,000 $15,000 Expected

You have $25,000 invested in two mutual funds with the following characteristics: Mutual Fund A Mutual Fund B Amount Invested $ 10,000 $15,000 Expected Return 14% 12% Standard Deviation 25% 15% Beta 1.95 1.37 Correlation (PAB) 0.32 Risk-Free Rate 3.00% (A) Please calculate this portfolio's Sharpe Ratio. (B) Please calculate this portfolio's Treynor Ratio. (C) Based on the above, should you change the amounts you have invested in Fund A and Fund B (keeping your total investment at $25,000). Why or why not?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Portfolio Analysis A Sharpe Ratio Calculate Portfolio Expected Return Rp We can calculate the weight...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Multinational financial management

Authors: Alan c. Shapiro

10th edition

9781118801161, 1118572386, 1118801164, 978-1118572382