Answered step by step

Verified Expert Solution

Question

1 Approved Answer

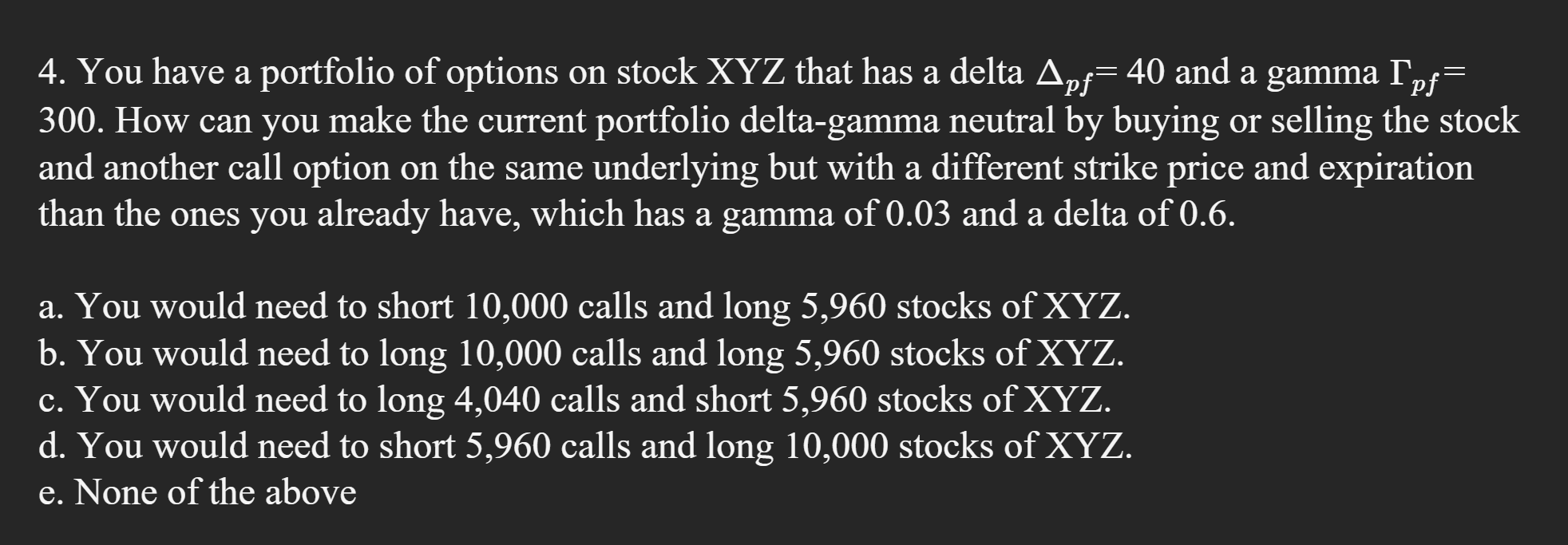

You have a portfolio of options on stock XYZ that has a delta p f = 4 0 and a gamma p f = 3

You have a portfolio of options on stock XYZ that has a delta and a gamma

How can you make the current portfolio deltagamma neutral by buying or selling the stock

and another call option on the same underlying but with a different strike price and expiration

than the ones you already have, which has a gamma of and a delta of

a You would need to short calls and long stocks of XYZ

b You would need to long calls and long stocks of XYZ

c You would need to long calls and short stocks of XYZ

d You would need to short calls and long stocks of XYZ

e None of the above

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

ABC Finance Coloring Book Familys First Financial Literacy Book

Authors: Jason Conger

1st Edition

1955961026, 978-1955961028