Answered step by step

Verified Expert Solution

Question

1 Approved Answer

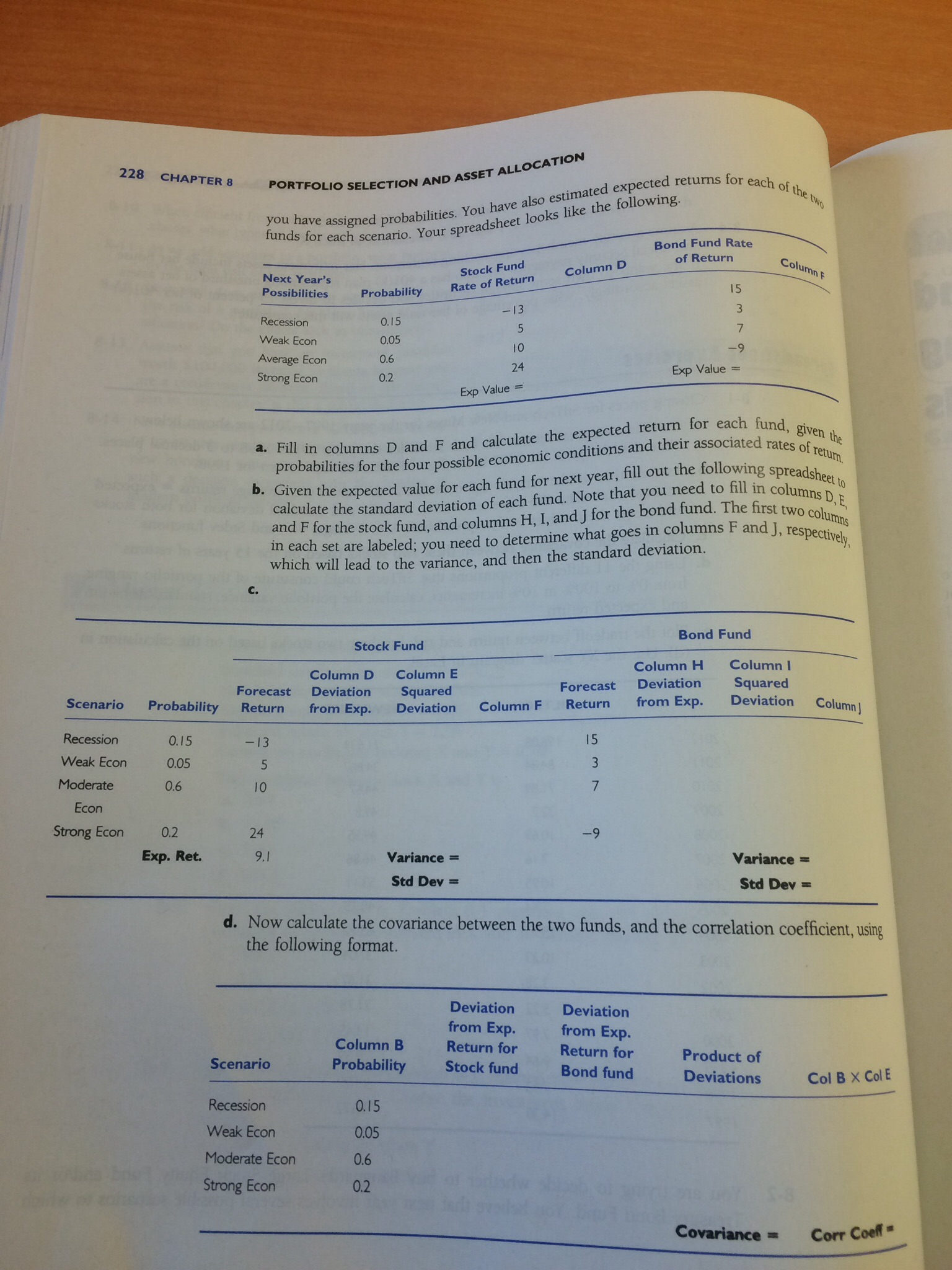

You have assigned probabilities. You have also estimated expected returns for each of the two funds for each scenario. Your spreadsheet looks like the following.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Principals Guide To School Budgeting

Authors: Richard D. Sorenson, Lloyd M. Goldsmith

3rd Edition

1506389457, 978-1506389455