Answered step by step

Verified Expert Solution

Question

1 Approved Answer

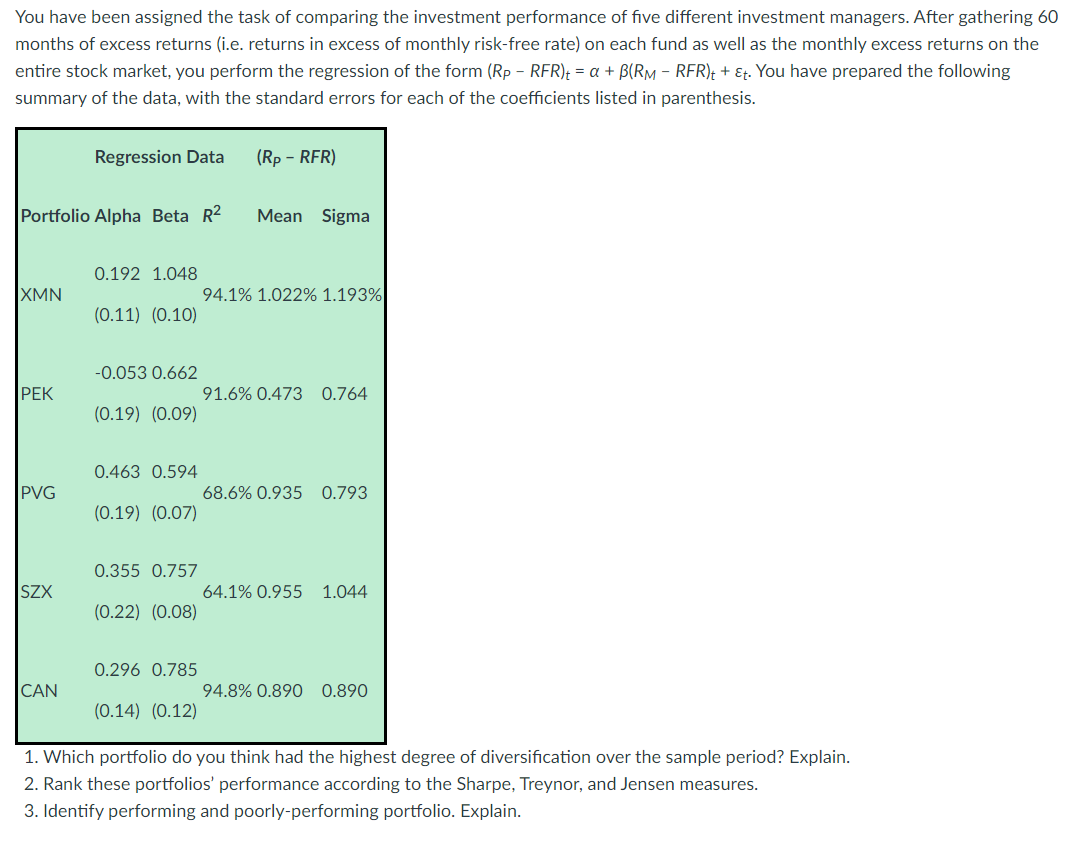

You have been assigned the task of comparing the investment performance of five different investment managers. After gathering 60 months of excess returns (i.e. returns

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financing High Tech Startups Using Productive Signaling To Efficiently Overcome The Liability Of Complexity

Authors: Robin P. G. Tech

1st Edition

331966154X,3319661558