Answered step by step

Verified Expert Solution

Question

1 Approved Answer

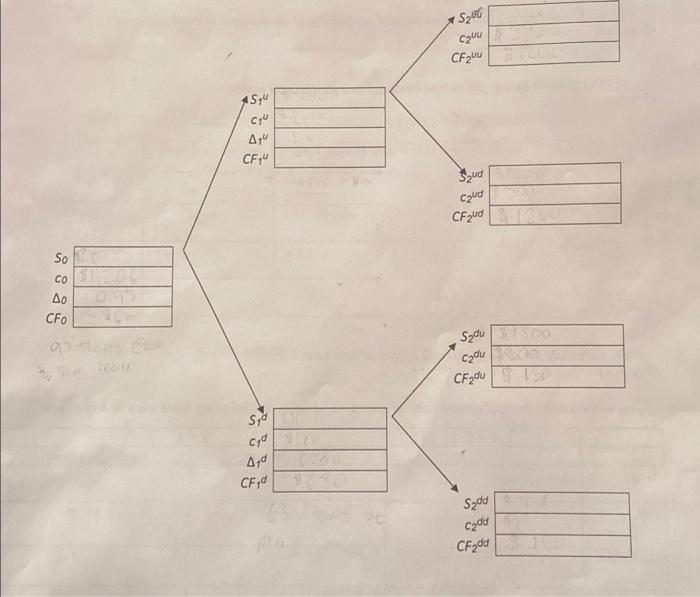

You have just sold a TWO-PERIOD call option on 100 shares of a $20 stock. In each of the next 2 periods the stock can

You have just sold a TWO-PERIOD call option on 100 shares of a $20 stock. In each of the next 2 periods the stock can go up 50% or fall by 50% The risk-free rate is 25 percent per period. The strike price is $12.00 per share. Delta hedge your short position in the option by adjusting the amount of shares that you own to "cover" the call. Note that your answer should show what you buy or sell (how many shares, strike prices, etc each period.

Please show how to get each step on the chart below.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Corporate Governance In Japan Institutional Change And Organizational Diversity

Authors: Masahiko Aoki , Gregory Jackson, Hideaki Miyajima

1st Edition

0199284520,0191536385